5 Keys to Managing Merchant Risk in Onboarding & Monitoring

What are the steps that merchant acquirers should follow to ensure they can transform the onboarding process while limiting merchant risk?

The impact of the recent global health crisis has been felt across many sectors and geographies, not least the payments sector that has undergone unprecedented change. Consumer habits have shifted to online shopping for goods and services and the impact for merchant acquirers is the need for faster onboarding of new merchants and effective ongoing monitoring to minimise fraud and compliance risk.

When it comes to onboarding new merchants, automation is key, to ensure a transition from the traditional time-consuming process to a slicker, faster process that limits friction for the new merchant. But what are the steps that merchant acquirers should follow to ensure they can respond to this new challenge of transforming the experience while at the same time limiting risk?

1. Automate as much of the underwriting process as possible

For acquirers, providing a frictionless onboarding experience for their merchant customers is essential. With the pandemic accelerating the general consumer shift to a more online approach, new smaller digital only merchants are regularly appearing, with tight margins and the need to be up and running quickly; for them, a speedy process of onboarding is critical.

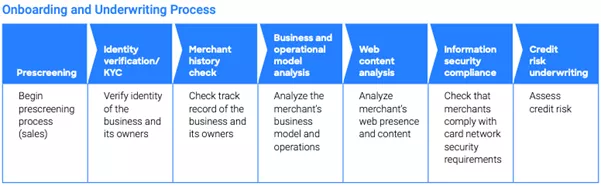

The typical merchant onboarding process has a number of different steps that need to be followed before an underwriting decision can be made, as highlighted in the table below, this is typically a 3-5 day process. As already indicated, given the current climate and the different landscape of online only micro-merchants, this process is too long.

Digital automation can enable a process to underwrite a new merchant in just minutes rather than days. However, this acceleration in decisioning can come at the expense of risk management and can negatively impact profitability for the acquirer if not done correctly.

2. Gather actionable and objective data

Having access to actionable and objective data is key to effective onboarding decisioning. Merchant acquirers should leverage a mix of their own data, third-party data and scoring services to enrich their view of each applicant. The best practice is to leverage both application data and external data from the growing marketplace of data vendors who provide critical insight and scoring of things like bank account validation, email addresses, IP addresses, device IDs and negative hotlists. Ingesting internal data from disparate sources eliminates manual data entry and reduces judgmental underwriting decisioning while creating consistency through automation.

‘Acquirers possess a gold mine of data but the complexity of disparate platforms, unclear data strategy, poor data architecture, and limited buildout capabilities have impaired the ability to effectively monetize this asset.’ (2020 McKinsey Global Payments Report)

3. Leverage analytics and rules

In addition to having accurate and objective data, acquirers should find ways to analyse this data, leveraging analytic models and rules. The tools to do this should allow the acquirer to import models, scorecards, trees and tables, and should be fully configurable from a user perspective. In addition to external data, acquirers often have historical data on applicants but it is inaccessible due to the sprawl of data. Rather than suffering through the pain of trying to centralize all referential data in a single data store, architect the solution to grab data where it resides across many sources and access it at the time of decisioning.

4. Expand the risks you are monitoring, and your rate of learning

Managing risk in the onboarding process should not be the only consideration for merchant acquirers and their merchant customers. Increased digitization and greater demand for new payment solutions have added more risk to merchant acquirers’ portfolios. The barrier to entry into the digital/ecommerce marketplace has added risk as new entities are springing up and entering the system at breakneck speed. Validating these new entities requires more robust solutions that can leverage internal and external data.

Acquirers should sharpen their ability to manage fraud and compliance risk by assessing potentially collusive or fraud-targeted merchant activity, the likelihood of merchant attrition or bankruptcy, and existing and future merchant profitability.

There is a growing need to monitor merchants in real time to detect anomalous behaviours of merchants in time to stem losses. Also, we see great utility in connecting pre-book (onboarding) performance/results with post book (monitoring) outcomes to create faster learning loop and improvement of both areas. In fact, many acquirers are looking at fulfilling both these needs with a single platform/capability for better sharing of insights.

5. Ensure your merchant monitoring approach is comprehensive

An effective merchant monitoring approach will be automated, leverage cutting-edge analytics, real-time urgency and flexible data ingestion, and be able to proactively alert acquirers to potential risks and double as a competitive advantage for attracting new merchants to their network.

To find out more about why an effective strategy for merchant onboarding and monitoring is so important, download the new eBook, Managing Risk with Frictionless Digital Onboarding and Merchant Monitoring.

Learn more about FICO’s solutions for merchant onboarding and monitoring.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.