5 Keys to Using AI and Machine Learning in Fraud Detection

If done properly, using AI and machine learning in fraud detection can clearly distinguish legitimate and fraudulent behaviors while adapting over time to new tactics

Payment fraud is an ideal use case for machine learning and artificial intelligence (AI), and has a long track record of successful use. When consumers get a call, text, email or in-app messages from their card issuer asking them to validate a transaction, or informing them of fraud on their card, they may not even suspect that behind this bit of excellent customer service are a brilliant set of algorithms, such as neural networks. Recently, however, there has been so much hype around the use of AI and machine learning in fraud detection that it has been difficult for many to distinguish myth from reality. At times, you might come to the conclusion that AI and machine learning have just been invented, or just been applied to payments fraud for the first time!

In this blog series, I’m going to explore the five keys to using AI and machine learning in fraud detection. The insights here are based on FICO’s 25+ years in this field, protecting billions of cards worldwide, and my own experience in fraud solution management over the last 23 years.

Let’s dig in, shall we?

Machine Learning and Artificial Intelligence in Fraud

Before we get to Key 1, here’s a brief definition of what we’re talking about, since even the terms machine learning and AI are subject to misuse.

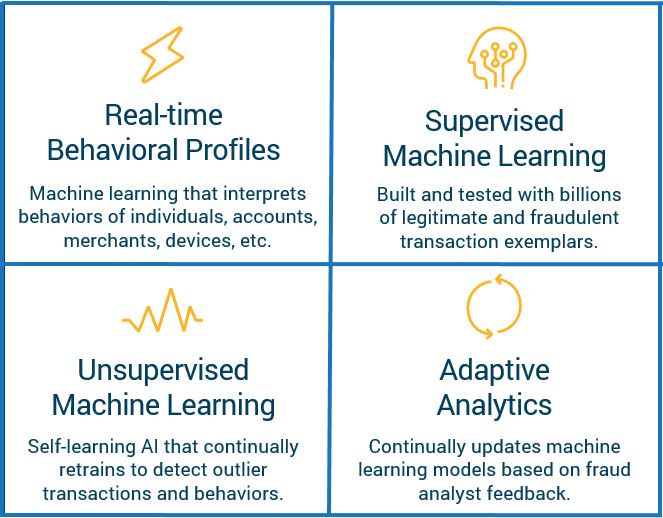

Machine learning refers to analytic techniques that “learn” patterns in datasets without being guided by a human analyst. AI refers to the broader application of specific kinds of analytics to accomplish tasks, from driving a car to, yes, identifying a fraudulent transaction. For our purposes, think of machine learning as a way to build analytic models, and AI as the use of those models.

Machine learning helps data scientists efficiently determine which transactions are most likely to be fraudulent, while significantly reducing false positives. The techniques are extremely effective in fraud detection and prevention, as they allow for the automated discovery of fraudulent and non-fraudulent patterns across large volumes of streaming transactions.

If done properly, machine learning can clearly distinguish legitimate and fraudulent behaviors while adapting over time to new, previously unseen fraud tactics. This can become quite complex as there is a need to interpret patterns in the data and apply data science to continually improve the ability to distinguish normal behavior from abnormal behavior. This kind of real-time fraud detection requires thousands of computations to be accurately performed in milliseconds.

Without a proper understanding of the domain, as well as fraud-specific data science techniques, you can easily employ machine learning algorithms that learn the wrong thing, resulting in a costly mistake that is difficult to unwind. Just as people can learn bad habits, so too can a poorly architected machine learning model.

Key 1 — Integrating Supervised and Unsupervised AI Models in a Cohesive Strategy

Because organized crime schemes fraudsters use are so sophisticated and quick to adapt, defense strategies based on any single, one-size-fits-all analytic technique will produce sub-par results. Each use case should be supported by expertly crafted anomaly detection techniques that are optimal for the problem at hand. As a result, both supervised and unsupervised models play important roles in fraud detection and must be woven into comprehensive, next- generation fraud strategies.

A supervised model, the most common form of machine learning across all disciplines, is a model that is trained on a rich set of properly “tagged” transactions. Each transaction is tagged as either fraud or non-fraud. The models are trained by ingesting massive amounts of tagged transaction details in order to learn patterns that best reflect legitimate behaviors. When developing a supervised model, the amount of clean, relevant training data is directly correlated with model accuracy.

Unsupervised models are designed to spot anomalous behavior in cases where tagged transaction data is relatively thin or non-existent. In these cases, a form of self-learning must be employed to surface patterns in the data that are invisible to other forms of analytics.

Unsupervised models are designed to discover outliers that represent previously unseen forms of fraud. These AI-based techniques detect behavior anomalies by identifying transactions that do not conform to the majority. For accuracy, these discrepancies are evaluated at the individual level as well as through sophisticated peer group comparison.

By choosing an optimal blend of supervised and unsupervised AI techniques you can detect previously unseen forms of suspicious behavior while quickly recognizing the more subtle patterns of fraud that have been previously observed across billions of accounts. A good example of this occurs in our FICO Falcon Platform, with its Cognitive Fraud Analytics.

Follow me on Twitter @FraudBird.

Find Out More About AI and Machine Learning in Fraud Detection

- Review Key 2: Applying Behavioral Profiling Analytics in Fraud Detection

- Review Key 3: Distinguishing Specialized from Generic Behavior Analytics

- Review Key 4: Leveraging Large Datasets to Develop Models

- Review Key 5: Adaptive Analytics and Self-Learning AI

- Discover FICO's fraud solutions

- Read our white paper Fighting Scams with AI Decisioning

This is an update of a post originally posted on July 3, 2018.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.