Addressing Portfolio Risk in Economic Uncertainty: Part 2 (2022)

Building portfolio risk resilience into customer acquisition

If we think of a lending portfolio as an exclusive night club, its underwriting policy acts as the doorperson, checking IDs and making sure anyone trying to enter meets minimum acceptance criteria. Most underwriting policies manage approval decisions based on someone’s assets and behavior at or before the time of application, considering how other similar applicants have behaved in the past. In both the real and metaphorical example, it would be helpful to have additional upfront insight about how people might respond to stress, as it becomes more challenging to manage behavior once they are “through the door.”

FICO® Scores, often an important contributor to underwriting risk management strategies, are designed to provide valuable risk rank-ordering through all economic cycles. The introductory blog to this series notes that consumer behavior varies under stress based on borrower credit risk resilience as measured by FICO® Resilience Index, even within narrow FICO Score bands. Understanding how these portfolio risk variations could manifest in a stressed environment contributes to even more informed portfolio risk-taking and strategic decision-making than using FICO Scores alone.

The FICO® Scoring Solutions team is often asked: Does FICO® Resilience Index only provide useful risk management insight when economic stress is occurring or imminent? Or does it also add value to decisions during benign periods of the economy? This blog illustrates how to use FICO Resilience Index in underwriting risk management strategies during both stressed and unstressed times to maximize its return on investment.

Traditional underwriting risk management strategy approach in stressed versus unstressed economy

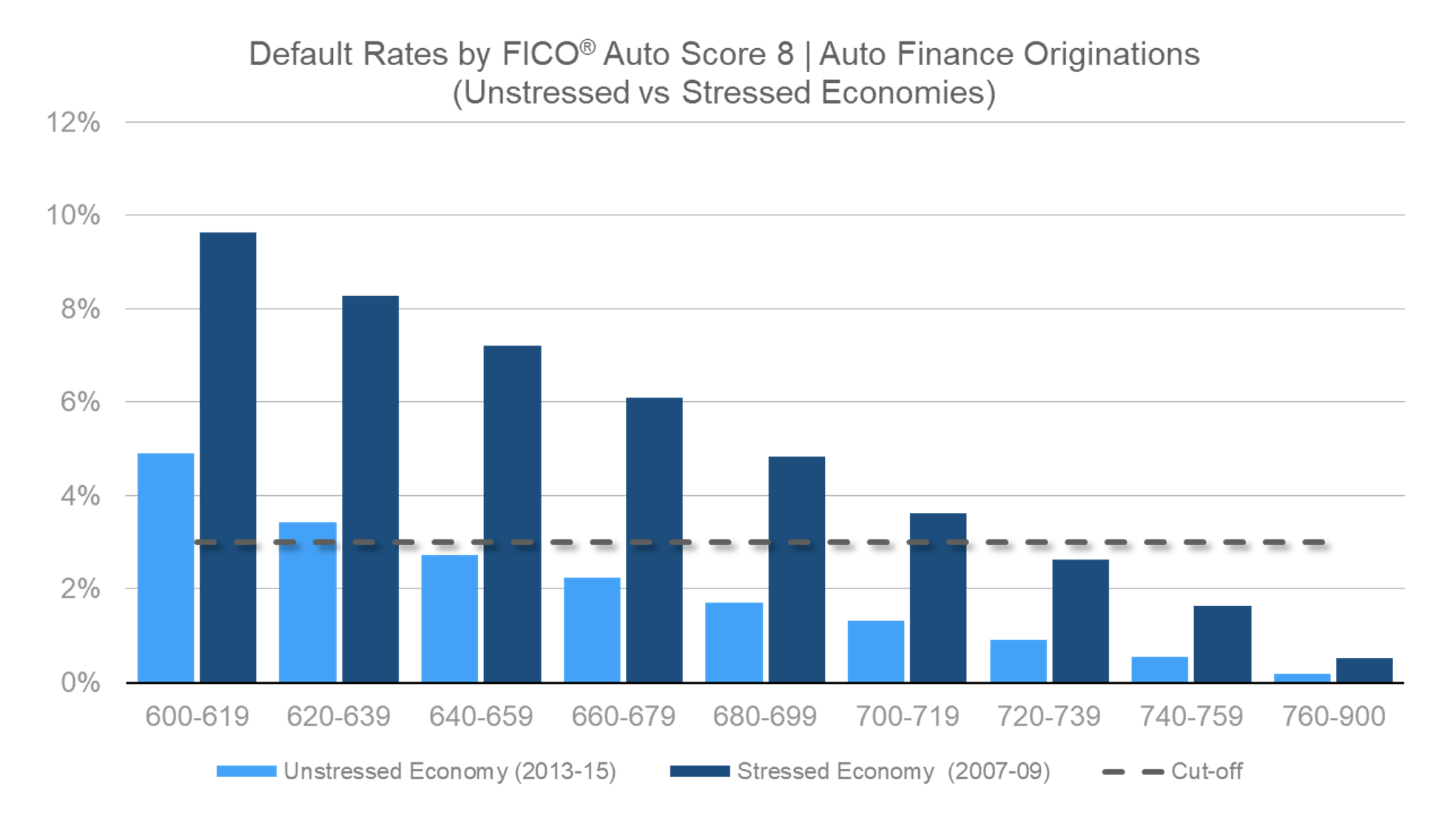

Assume an auto finance portfolio’s current underwriting risk management strategy requires applicants to have an expected 24-month default rate less than 3%. As seen in Figure 1, in the unstressed economy of 2013-15, this would have aligned with a simple FICO® Score cut-off of 640 or higher. However, in the stressed economy of 2007-9, this would have aligned with a FICO Score cut-off of 720 or higher.

During the highly uncertain time of the Great Recession, most lenders shifted management strategies by raising FICO® Score cut-offs significantly to achieve the same overall portfolio risk management profile for accepted applicants. Some even paused new account underwriting altogether, regardless of the applicant’s assets or behaviors.

Figure 1: Auto finance account origination default rates by FICO® Auto Score 8, Oct 13-Oct 15 and Oct 07-Oct 09 versus a theoretical 3% default rate cut-off.

Using FICO® Resilience Index in underwriting risk management strategies in a stressed economy

Economic Scenario

Severe economic stress is occurring or expected to start imminently.

Business Challenge

Raising FICO® Score cut-offs can help manage overall risk levels but can also eliminate the potential to acquire more resilient consumers in FICO Score ranges just below the cut-off. In addition, less portfolio resilient consumers that meet the FICO Score cut-off may significantly underperform in a stressed economy.

FICO® Resilience Index Solution

Using FICO® Resilience Index together with FICO® Score, lenders can manage and leverage information about consumer risk resilience to differentiate payment performance through periods of economic stress.

Methodology and Results

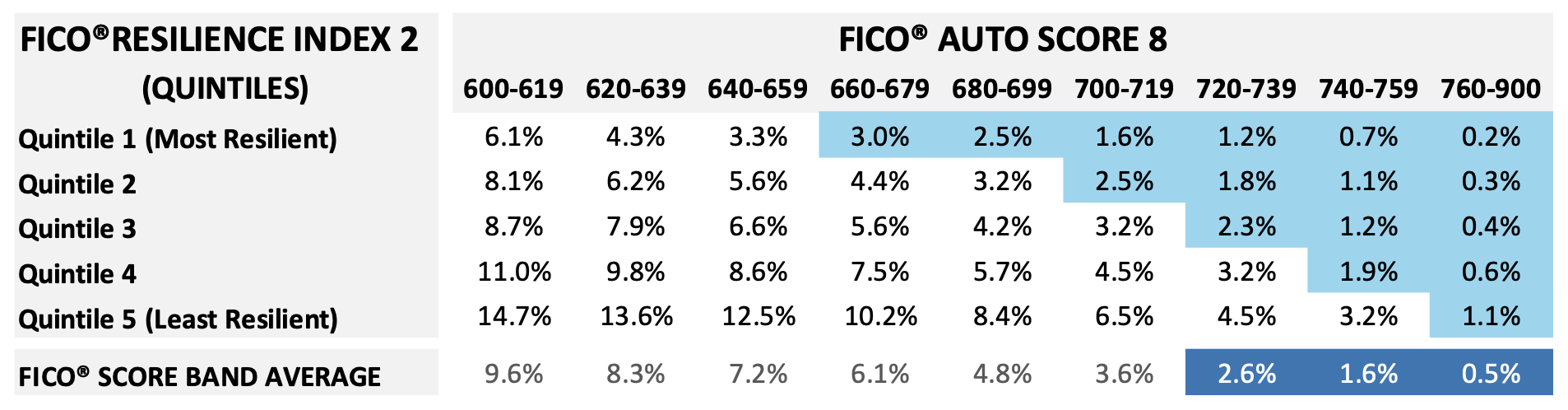

Continuing with our auto finance example, applying the same 3% cut-off based on both scores versus FICO® Score alone leads to a “swap in” population of more resilient applicants in the 660-679, 680-699, and 700-719 FICO Score bands and a “swap out” population of less resilient applicants in the 720-739 and 740-759 FICO Score bands, as seen in Figure 2.

Default rates by FICO® Auto Score 8 and FICO® Resilience Index 2 – stressed economy (Oct 2007 to Oct 2009)

Figure 2: Auto finance account origination default rates by FICO® Auto Score 8 and FICO® Resilience Index 2, Oct 07-Oct 09. Cells are highlighted where the expected default rate is below 3%.

Using FICO® Resilience Index in underwriting risk management strategies in an unstressed economy

Economic Scenario

A benign economy is expected in the immediate future. However, it is recognized that downturns are now a regular part of the economic cycle.

Business Challenge

In a benign economy, lenders need to build risk resilience into their underwriting decisions; however, without insight into how individual consumers within certain FICO® Score bands will fare during times of economic stress, they are creating an unknown potential for additional portfolio risk during downturns.

FICO® Resilience Index Solution

FICO® Resilience Index is designed to continue to rank-order borrower risk resilience during benign periods. Actively managing portfolio risk resilience may result in less volatile credit portfolio risk performance observable during periods of economic stress.

Methodology and Results

One management framework we recommend incorporates a two-layered risk appetite statement in the following form: We will accept applicants with expected default rates less than X% and stressed default rates less than Y%.

Applying this framework to the example above, a lender’s auto finance origination risk appetite statement during a benign period may read: We will accept applicants with expected default rates less than 3% and stressed default rates less than 6%.

Using FICO® Score alone, Figure 1 reveals that the lowest FICO Score cut-off that meets both criteria is 680. Introducing a two-layered risk appetite statement would therefore shift the FICO Score cut-off 40 points higher during a benign economy than the current strategy.

Incorporating FICO® Resilience Index allows a more precise implementation of the two-layered risk appetite statement due to its ability to differentiate credit portfolio risk performance under stress within narrow FICO® Score bands.

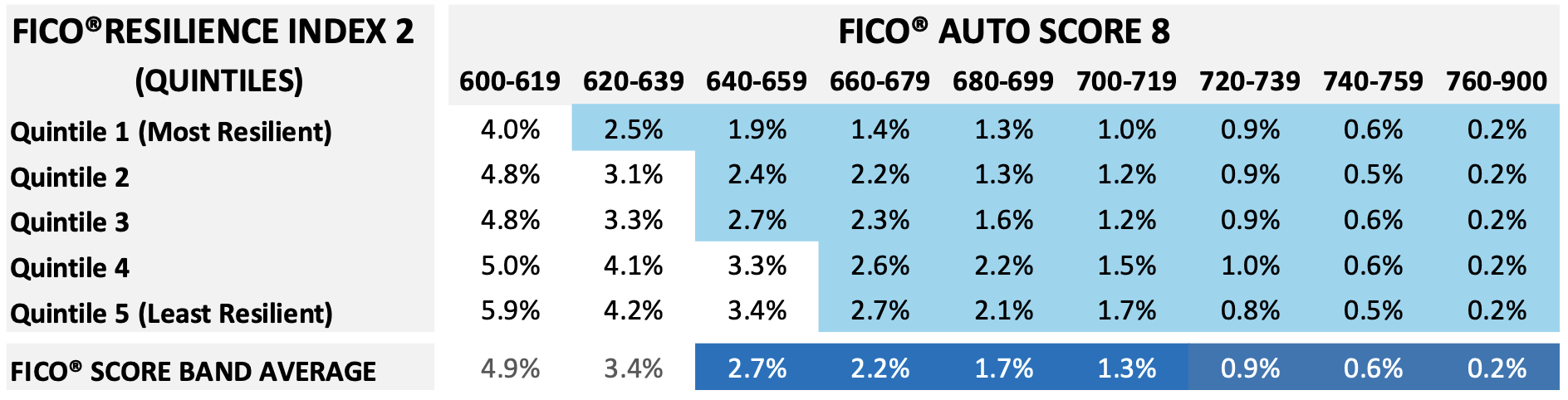

Figure 3 shows auto finance risk performance through the benign economy of October 2013 to October 2015. As expected during such times, there is only a minor difference between the population that meets the desired 3% cut-off based on FICO® Score alone (i.e., a FICO Score cut-off of 640) and the one based on a combination of FICO Score and FICO® Resilience Index.

Default rates by FICO® Auto Score 8 and FICO® Resilience Index 2 – unstressed economy (Oct 2013 to Oct 2015)

Figure 3: Auto finance account origination default rates by FICO® Auto Score 8 and FICO® Resilience Index 2, Oct 13-Oct 15. Cells are highlighted where the expected default rate is below 3%.

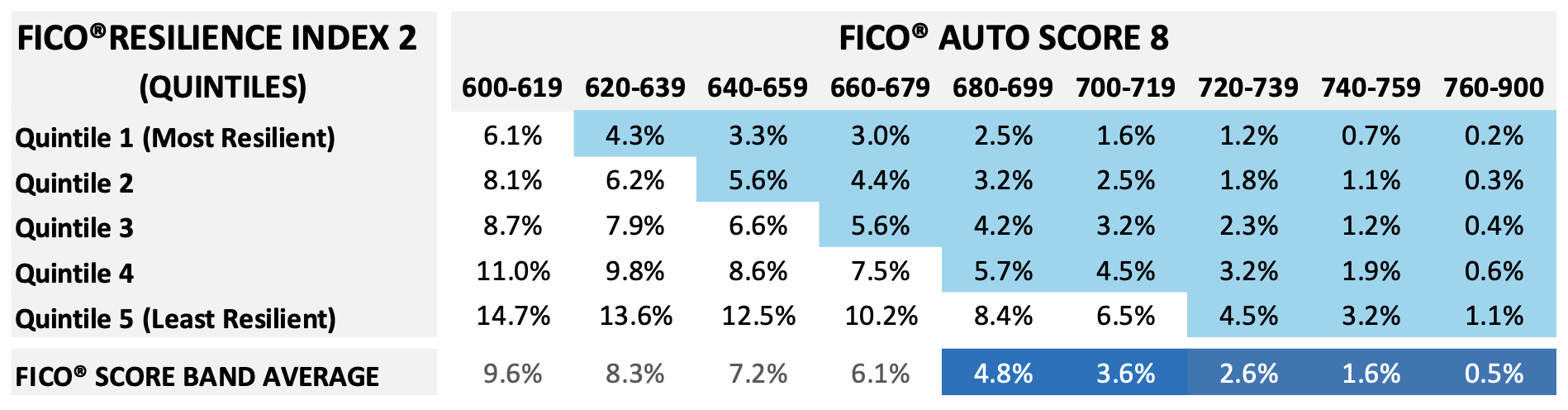

In contrast, Figure 4 shows the same stressed auto finance risk performance presented in Figure 2, but cells are only highlighted where the default rate fell below the maximum stressed default rate of 6%. Here, incorporating FICO® Resilience Index provides a more refined view of the eligible population, as expected.

Default rates by FICO® Auto Score 8 and FICO® Resilience Index 2 – stressed economy (Oct 2007 to Oct 2009)

Figure 4: Auto finance account origination default rates by FICO® Auto Score 8 and FICO® Resilience Index 2, Oct 07-Oct 09. Cells are highlighted where the expected default rate is below 6%.

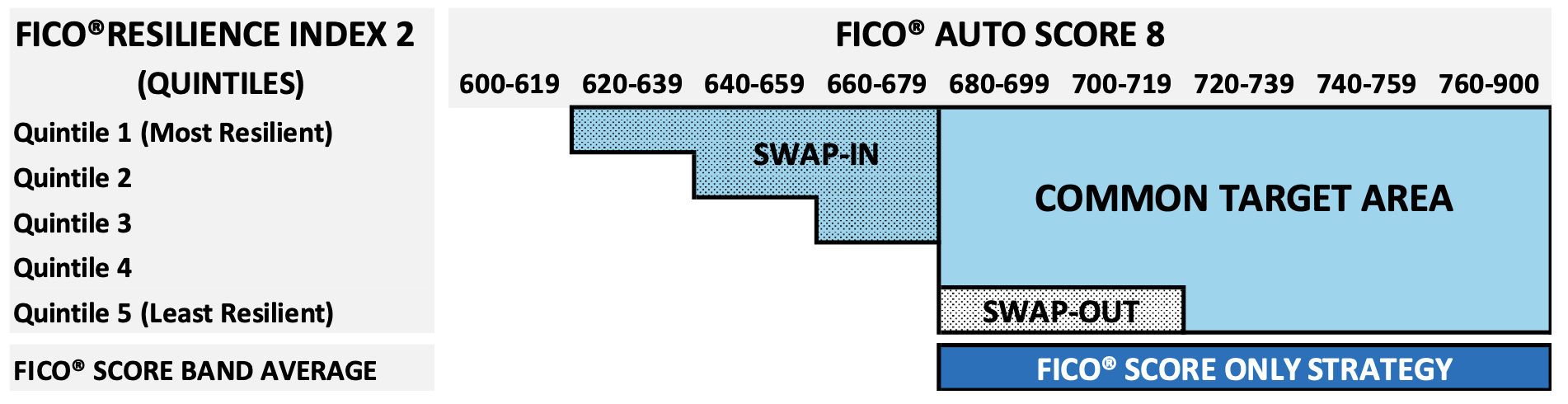

Implementing the two-layered risk appetite statement therefore identifies the populations that meet the required criteria on both charts. As seen in Figure 5, while the approach using FICO® Score alone would result in a simple FICO Score cut-off of 680, the combined strategy using both FICO Score and FICO® Resilience Index would swap in more resilient applicants just below that FICO Score cut-off and swap out less resilient applicants just above it.

Underwriting strategy comparison (FICO® Auto Score 8 only vs. FICO Auto Score 8 and FICO® Resilience Index 2 together)

Figure 5: Auto finance account origination strategy reflecting two-layered risk appetite statement based on FICO® Auto Score 8 and FICO® Resilience Index 2. Cells are highlighted where the expected (unstressed) default rate is below 3% and the unexpected (stressed) default rate is below 6%.

Relevance to other industries

While the above example illustrates the application and benefit of the combined use of FICO® Auto Score 8 and FICO® Resilience Index 2 to adjust auto finance underwriting risk management decisions, lenders can expect to reap similar value across portfolios in other industries (e.g., bankcard, mortgage, unsecured personal lending). Further, the ability to rank-order and manage applicants’ risk resilience to economic downturns (expected or unexpected) offers intuitive value for related account origination decisions such as account pricing, product qualification, and initial loan (or line) assignment.

Benefits of a two-layered risk appetite approach including FICO® Resilience Index

Incorporating a two-layered risk appetite takes full advantage of FICO® Resilience Index’s ability to differentiate performance under stress, providing lenders more refined portfolio risk management decision-making power, even during benign periods of the economy.

Please visit the FICO Blog to find all four parts of this series and to keep up to date on how to enhance portfolio risk management with all of FICO’s latest insights and offerings.

To gain more background about the FICO® Resilience Index, please visit https://www.fico.com/en/products/fico-resilience-index.

This blog is co-authored with Jim Patterson, Senior Director of Product Management

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.