Addressing Portfolio Risk in Economic Uncertainty: Part 3 (2022)

Building portfolio risk resilience into customer management

We all purchase insurance policies for one fundamental reason – to protect and manage our valuable assets against unexpected events. No one plans to have an automobile accident or to have a tree fall on their home, and insurance provides valuable peace of mind that, should significant unexpected events such as these occur, they don’t translate into financial hardships or major life disruptions. Lenders must adopt a similar mindset as they manage the financial health of their consumer lending portfolios to insulate their existing assets from potential portfolio risk volatility.

As we discussed in part 1 of this blog series, FICO® Resilience Index (FRI) was designed with precisely this capability in mind. Leveraging FICO Resilience Index to refine credit risk management decisions during benign economic phases defends against dramatic swings in delinquency rates and provides for a more consistent portfolio risk management approach over time.

During the pandemic, systemic financial assistance programs such as federal stimulus payments and the availability of lender-provided payment accommodations undoubtedly prevented and helped manage the dramatic increases in delinquencies and losses we witnessed in 2008-9. Impressively, the Federal Reserve reported Q1 2022 delinquency rates on all consumer loans of 1.63%, one of the lowest marks in the 35+ years it has been tracked. Despite this good news, many remain concerned that the pendulum will eventually swing in the opposite direction, especially given recent economic challenges on multiple fronts (e.g., inflation, geopolitical instability, ongoing supply chain issues). Indeed, Q3 2022 delinquency rates already appear to reflect some additional credit risk, having increased to 1.92% on all consumer loans, still lower than any pre-pandemic rate on record.

Of course, credit risk management is only one aspect of portfolio health. For revolving credit portfolios in particular, proper attention must be directed toward maintaining asset and revenue growth. As was the tactic during the Great Recession, lender credit risk management response in early 2020 – with few exceptions – was a full cessation of credit limit increases, balance transfer offers, and other spend incentive programs. The result was further downward pressure on an already cautious consumer spending climate during the pandemic, waning portfolio assets and, along with them, significant reductions in interest and non-interest income that had many lenders grappling with the idea of aggressive spend stimulus programs.

Leveraging FICO® Resilience Index can help improve revolving account portfolio exposure management strategies by balancing the need to manage portfolio credit risk in the face of economic uncertainty while encouraging healthy asset growth. By constraining credit exposure across more sensitive customer segments, the delinquency impacts associated with unexpected economic downturns can be mitigated. At the same time, uninterrupted credit limit increase programs coupled with spend incentives to the most resilient segments can help promote and manage usage, asset, and revenue growth.

Two-layered risk appetite approach to customer management without FICO® Resilience Index

To carry the use case forward a bit, let’s first consider exposure portfolio management in an unstressed environment. As we discussed in part 2 of this blog series, which focused on customer acquisition risk management decisions, lenders may choose to take a two-layered risk appetite approach. For example, recognizing that downturns are a regular part of the economic cycle, a portfolio risk manager may define a target population for limit increases as customer segments with expected default rates below X% and stressed default rates below Y%. For the sake of our credit limit increase illustration, let’s suppose the stated risk appetite requires default rates below 5% during a benign economy and below 7% during stressed economic conditions.

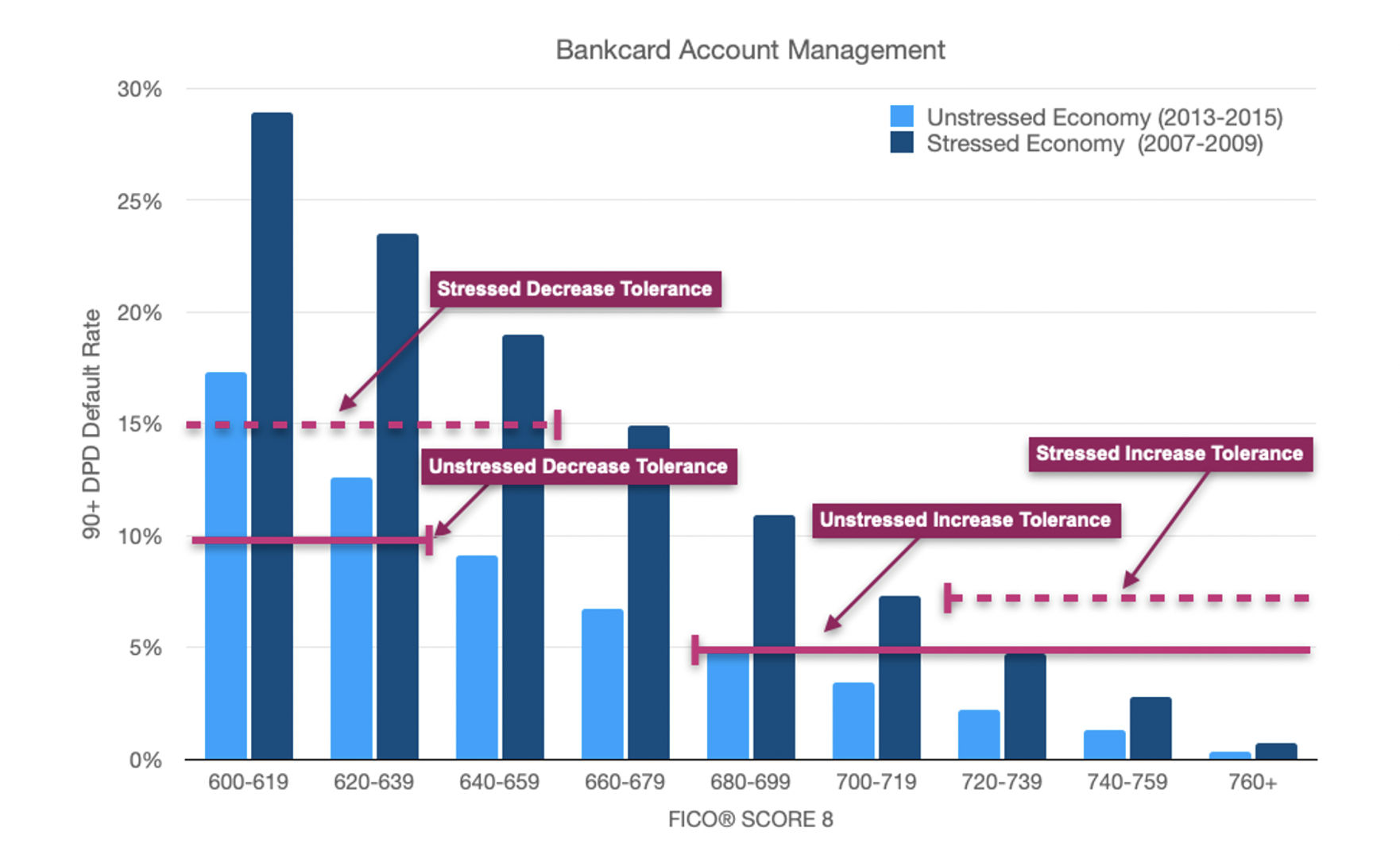

Based on observed industry-wide 90+ days past due default rates for bankcard account management during benign and stressed economic periods (Figure 1), our example risk appetite would mean raising the “normal” credit limit increase inclusion FICO® Score cutoff from 680 to 720.

Figure 1: Bankcard account management default rates by FICO® Score 8, Oct 13-Oct 15 versus Oct 07-Oct 09.

Expanding our exposure management illustration to include credit limit decreases, suppose the stated risk appetite is account default rates above 10% during a benign economy or above 15% during stressed economic conditions. Using a two-layered risk appetite statement would mean raising the “normal” limit decrease inclusion FICO® Score cutoff from below 640 to below 660.

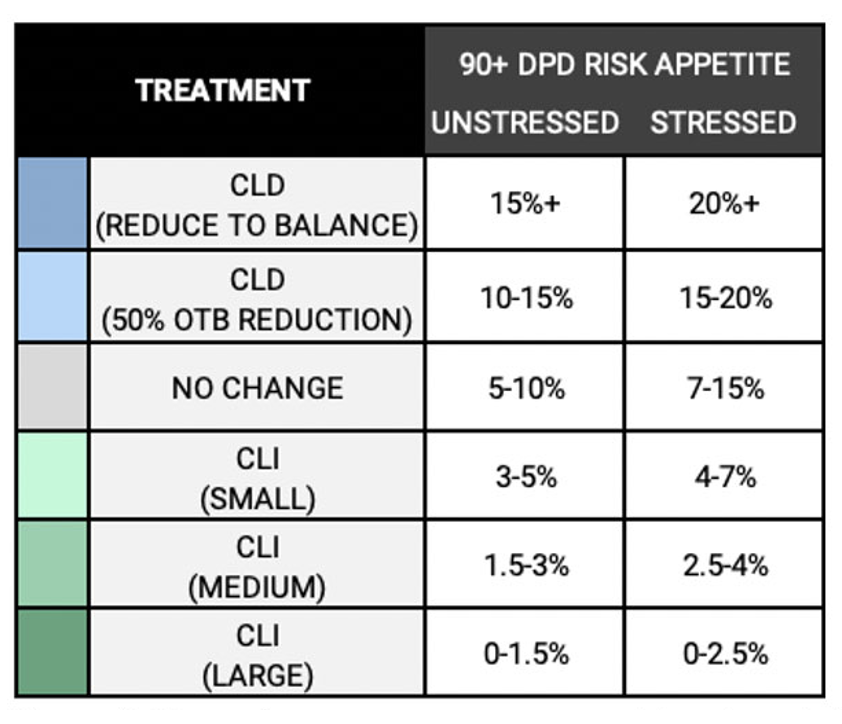

Introducing different levels of credit limit increases and decreases, the complete range of customer risk management treatments by risk appetite may be expressed as shown in Figure 2. The highest risk customers are targeted for credit limit decreases either to their existing balance or by trimming 50% of their existing available credit, or “open-to-buy” (OTB). Credit limits within moderate risk ranges are unchanged while low risk segments qualify for different tiers of credit limit increase amounts.

Figure 2: Example credit limit exposure management treatments by risk appetite.

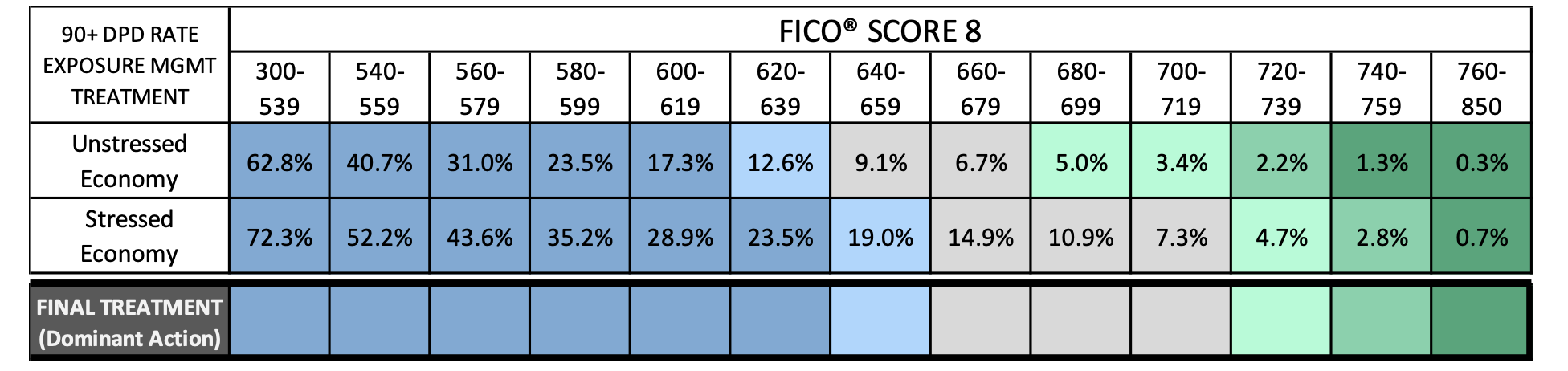

Applying this strategy to a portfolio with the projected unstressed and stressed economy default rates shown in Figure 3 yields a range of limit increase and decrease actions. The final “dominant” treatment is based on the more restrictive action associated with the FICO® Score band. Here, the more restrictive actions happen to align to those from the stressed scenario, but this may vary depending on the risk appetite statement and the default rates by FICO Score band in each scenario.

Figure 3: Exposure risk management treatment approach based on FICO® Score 8 only. Cell values represent bankcard account management 90+ days past due default rates by FICO Score 8, unstressed economy (Oct 13-Oct 15) versus stressed economy (Oct 07-Oct 09).

Two-layered risk appetite approach to customer management including FICO® Resilience Index

Factoring in FICO® Resilience Index makes our illustrated exposure management treatment significantly more informed and targeted. The table in Figure 4 shows account default rates during an unstressed economy by both FICO® Score and FICO Resilience Index. Again, credit limit management actions are allocated according to our stated risk appetite during an unstressed economy.

Figure 4: Exposure management treatment approach based on FICO® Score 8 and FICO® Resilience Index 2. Cell values represent bankcard account management 90+ days past due default rates by FICO Score 8 and FICO Resilience Index 2 during an unstressed economy (Oct 13-Oct 15).

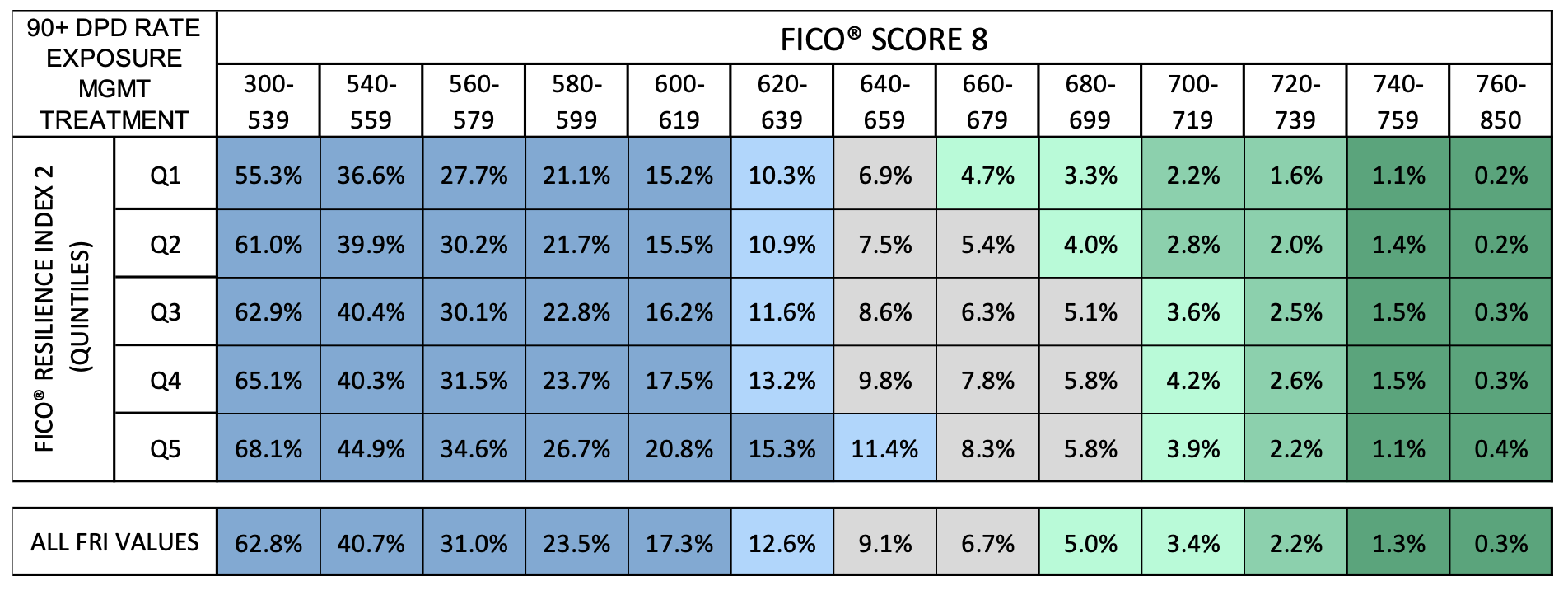

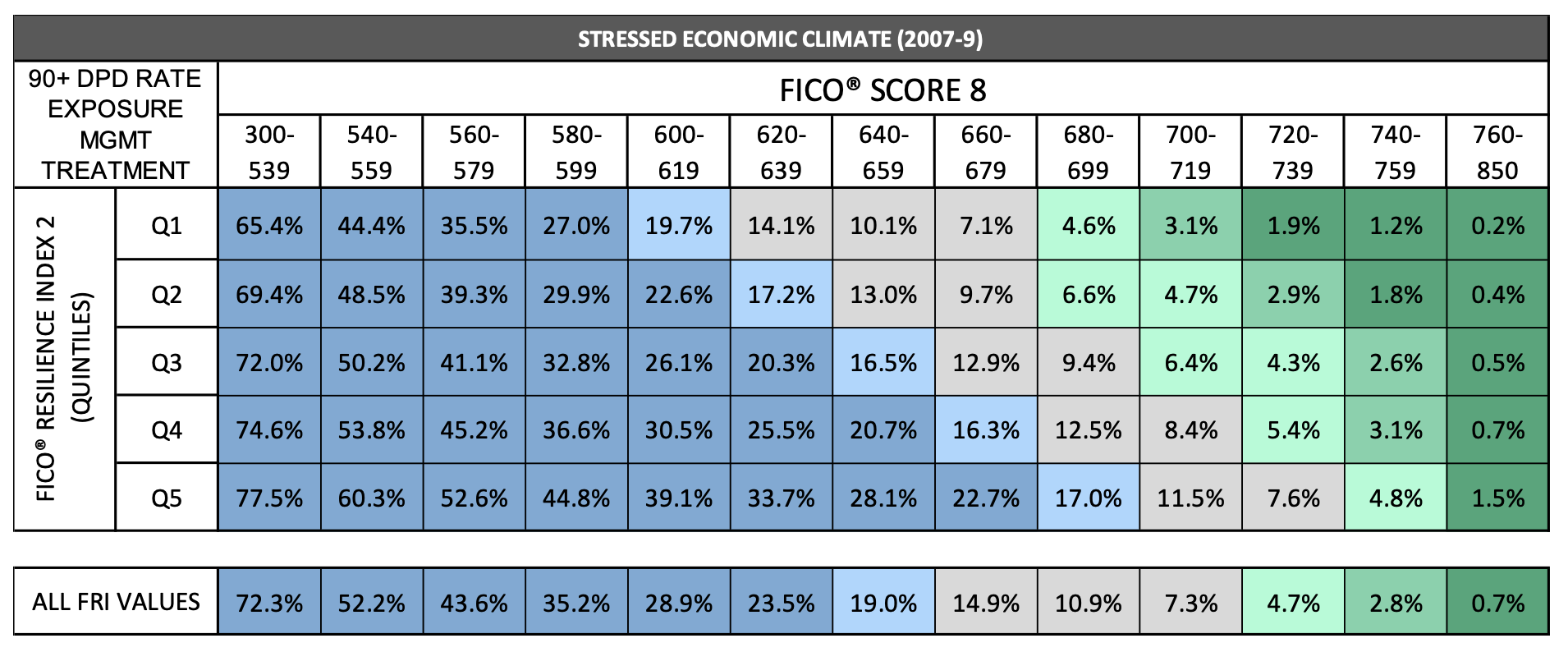

Figure 5 repeats the above exercise, but this time we apply the approach to the stressed economic period.

Figure 5: Exposure management treatment approach based on FICO® Score 8 and FICO® Resilience Index 2. Cell values represent bankcard account management 90+ days past due default rates by FICO Score 8 and FICO Resilience Index 2 during a stressed economy (Oct 07-Oct 09).

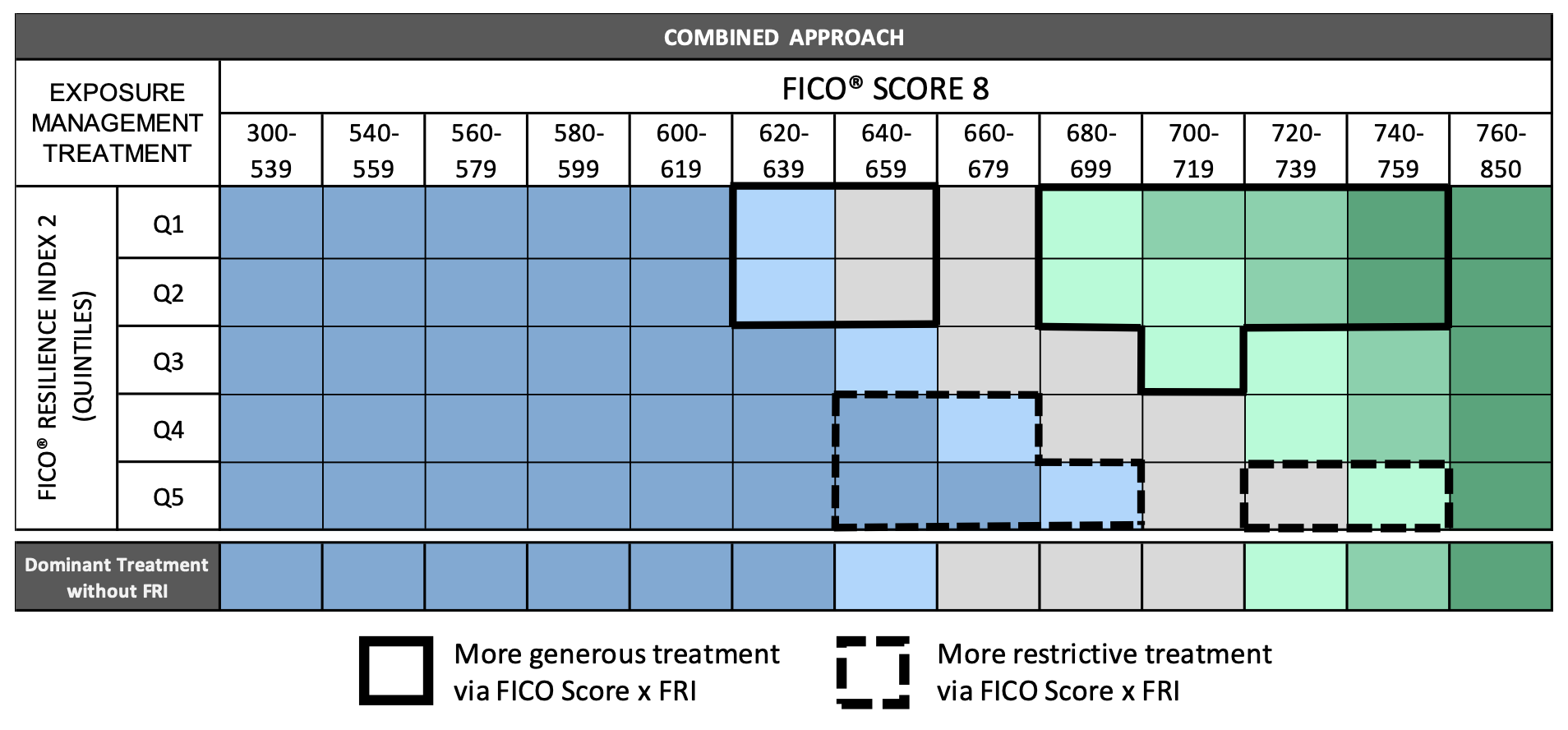

Finally, our illustration of the combined, or two-layered, risk appetite statement identifies the target populations that meet the required criteria for both the unstressed and stressed economy treatment approaches. Again, the dominant treatment is based on the more restrictive action associated with the FICO® Score band and FICO® Resilience Index quintile between the unstressed and stressed economic scenarios. Figure 6 summarizes the combined credit exposure treatment approach and highlights the shift in credit limit allocation through swap in/out groups and segments that receive a more generous or restrictive action as compared to the original FICO Score-based strategy approach.

Figure 6: Bankcard exposure management strategy reflecting two-layered risk appetite statement based on FICO® Score 8 and FICO® Resilience Index 2.

Leveraging this approach over time, based on your own risk appetite, enhances portfolio risk resilience by reducing exposure to sensitive customers whose performance would markedly deteriorate during economic downturns while favoring resilient customers whose performance would be more stable through such troubled times.

Relevance to other customer risk management decisions

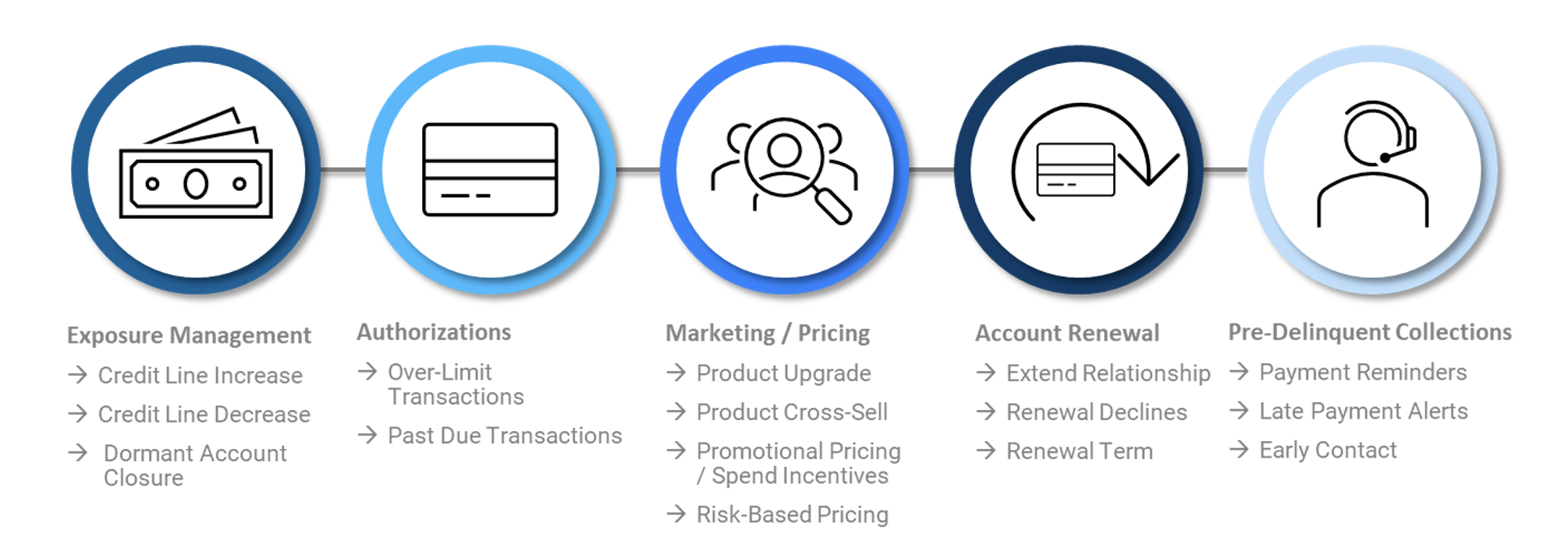

Nearly any risk-based decision may be improved by considering the degree to which a stressed economic climate is likely to impact a consumer’s ability to repay their debts. In addition to improving portfolio exposure management decisions as illustrated above, FICO® Resilience Index can enhance numerous other customer management decisions (Figure 7), such as:

- Authorizations – Refine transaction approval and decline decisions for over-the-limit transactions based on customer resilience.

- Marketing / Pricing – Target spend incentive campaigns that favor more resilient customer segments. Promote usage and loyalty via product upgrades and deepen customer relationships across the portfolio via cross-sell campaigns to more resilient customers.

- Account Renewal – Adjust renewal decisions in customer portfolio segments based on likelihood of negative performance during economic downturns.

- Pre-Delinquent Collections – Accelerate collections efforts at the missed payment due for customers who are deemed sensitive based on FICO® Resilience Index. Target resilient customer portfolio segments with non-invasive courtesy notifications via digital outreach.

Please visit the FICO Blog to find all four parts of this series and to keep up to date on all of FICO’s latest insights and offerings.

To gain more background about the FICO® Resilience Index, please visit https://www.fico.com/en/products/fico-resilience-index.

1 “Delinquency Rate on Consumer Loans, All Commercial Banks.” FRED, 16 August 2022, http://fred.stlouisfed.org/series/DRCLACBS.

This blog is co-authored with David Binder, Senior Director of Scores Product Management.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.