Behavioral Biometrics and Customer Identity Authentication

With synthetic identity fraud on the rise, behavioral biometrics enable banks to balance customer experience and fraud prevention

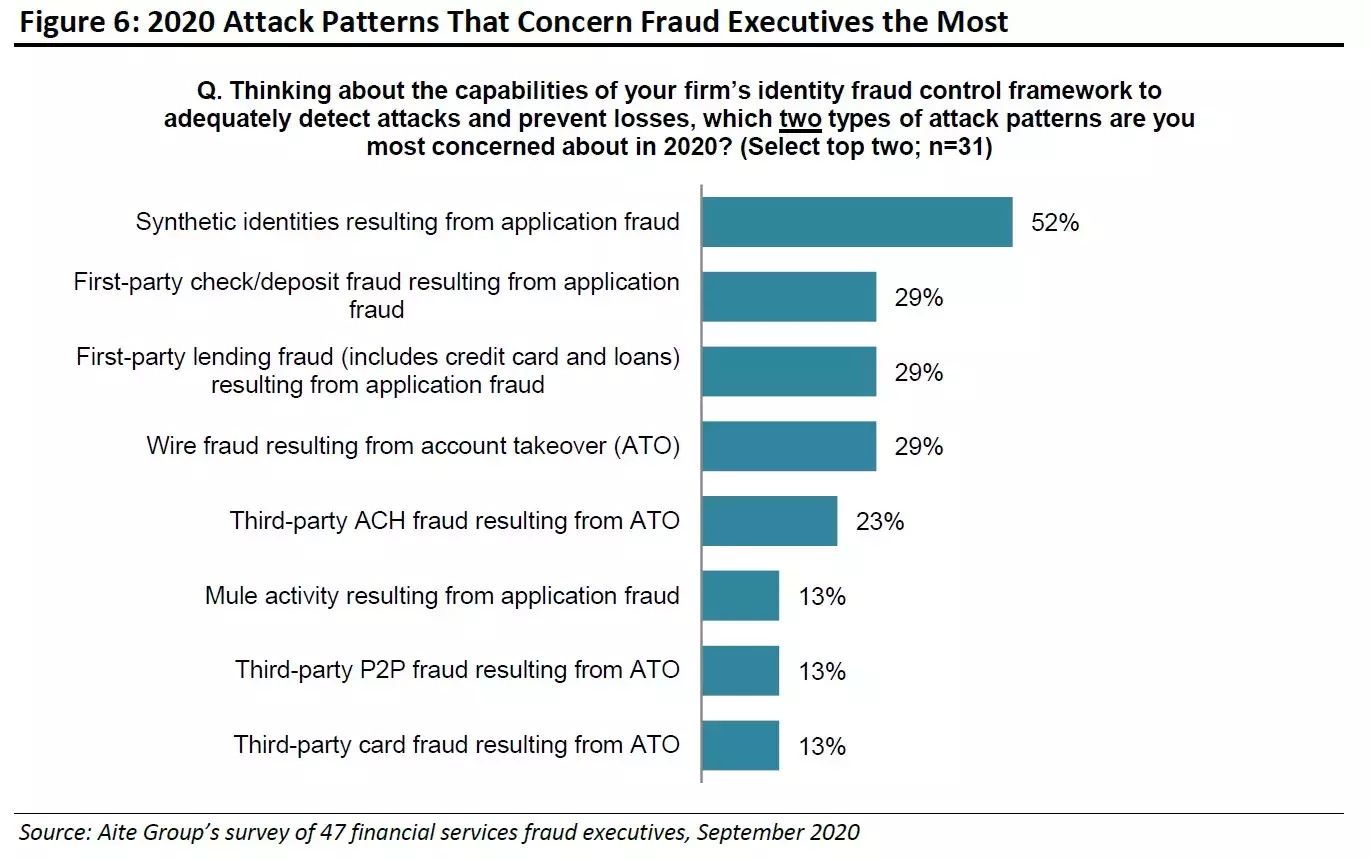

As COVID-19 has spread, concerns about fraud have increased. According to an Aite Group survey of U.S. fraud managers, their biggest concern in 2020 was synthetic identity fraud - 52% reported that this was their biggest issue in identity fraud control.

This presents a challenge to banks, as to be competitive in digital lending they need to provide a superior customer experience. Customers that perceive that they will get a better service elsewhere are likely to leave, particularly in countries such as the UK and the Netherlands that offer simple account switching services.

The key to resolving the tension between customer experience and fraud prevention is to ensure that the bank is using an integrated platform.

Why is being integrated so important? At every stage of the customer lifecycle, banks get more and more data from their customers and fraud managers want to use that data to make better fraud decisions. They can’t do this if the data only exists in a silo, and they have no access to that source.

What Are the Key Elements for Securing Digital Accounts?

Best-in-class customer experience is achievable when the levels of security do not unacceptably increase friction, as my colleague Liz Lasher noted in a recent post. When the balance is right customers gain easy access to their accounts when and where they want it. Seamless identity verification when accounts are opened, coupled with ongoing, smart authentication as accounts are used, is the right strategy for success. Authentication needs to create a balance between security and convenience. Customers look for this convenience, but if banks fail in protecting their accounts, customers easily switch to a competitor.

Behavioral Biometrics Empower Banks to Achieve Balance

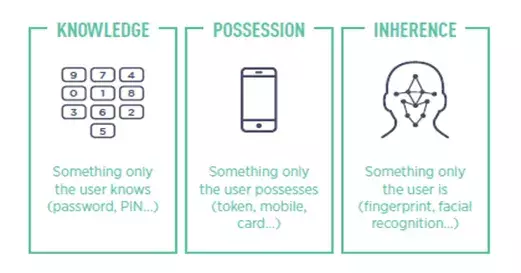

Customer authentication has evolved: in the past, it was mainly reliant on knowledge factors or something only the customer knows, such as a password. Given data breaches and poor password practices, this had to evolve and banks now routinely send one-time passcodes to confirm the identity of their customers by checking they are in possession of their mobile device.

Today people are becoming used to the authentication factor of inherence, or something they are – in other words, a biometric. This trend is being rapidly adopted as people find it convenient to use voice, face or fingerprint recognition. Even though these biometric methods are convenient, they still require the customer to do something. Now there is an alternative that is both reliable and to the customer invisible - behavioral biometric authentication.

How Do Behavioral Biometrics Work?

Behavioral biometrics identify a customer by recognizing the way they do something. Given that this is typically through an activity they were already engaged in, it is a security method that does not add friction to a customer’s journey.

Behavioral biometrics monitor user behavior during the duration of a session and detect any suspicious activity. These behaviors can include keystroke dynamics, mouse dynamics or handwriting dynamics. It’s possible to generate several parameters from a user’s unique way of doing these actions. These range from monitoring human motion gestures and patterns to keystroke dynamics, and factors such as speed, flow, touch, sensitivity pressure and even signature formats.

By leveraging behavioral biometrics to analyze physical and cognitive attributes, it’s possible to detect if an account is being accessed fraudulently, regardless of the customer’s location or device. By incorporating those behavioral insights into the risk analysis process, it’s possible to realize immediate ROI from reduced fraud losses, decreased operational costs, and improved customer satisfaction.

You can read more about how to use biometrics in this post: Six Steps To Using Biometrics To Open & Manage Accounts Digitally. Explore FICO’s solutions at Identity and Authentication.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.