Collaborative Profiling for Corporate Card Fraud Detection

Because corporate credit cards have different business-oriented spending patterns than consumer credit cards, we tackled the corporate card fraud detection problem with FICO’s coll…

If you’re a runner in a major city, chances are you already know what the Corporate Challenge is. This blog isn’t about how to improve your race time or raise more money from sponsors. It’s about a very different kind of challenge: corporate credit card fraud.

FICO recently released two new Corporate Credit models: one for the UK and Ireland, and one for the US; they incorporate standard Falcon 6 innovations, and also FICO’s advanced collaborative profiling technology.

Calibrating Models to Reflect Corporate Spending Behaviors

Corporate credit cards’ patterns are different from those of consumer and small business credit cards. Some corporate cards are frequently used for travel-related expenses, which could result in high-dollar fraud losses. Other corporate cards are used very infrequently, which may make it harder to detect suspicious fraudulent behaviors, since these cards lack full, deep behavioral profiles.

Because corporate credit cards have different business-oriented spending patterns than consumer credit cards, we tackled the corporate card fraud detection problem with FICO’s collaborative profiling technology.

What Is Collaborative Profiling?

FICO’s collaborative profiling technology generates archetypes associated with events from the card’s transaction history. These discrete events in the transaction history serve to differentiate cardholder behaviors from one another. Collaborative profiling has been used with great success in other FICO models such as anti-money laundering, cybersecurity and fraud detection.

An archetype is a mixture of payment card transaction events. Certain transactions will be more probable given a mixture of archetypes. Each cardholder is a mixture of archetypes; FICO uses a Bayesian inference algorithm to derive the latent archetypes in the dataset from a defined dictionary of transaction events and their occurrence for a cardholder. In building the new corporate card fraud models, we utilized an unsupervised machine learning algorithm comprising only non-fraudulent transactions, an approach that is much more stable over time than using fraud behaviors.

Real-Time Differentiation Drives Precise Fraud Detection

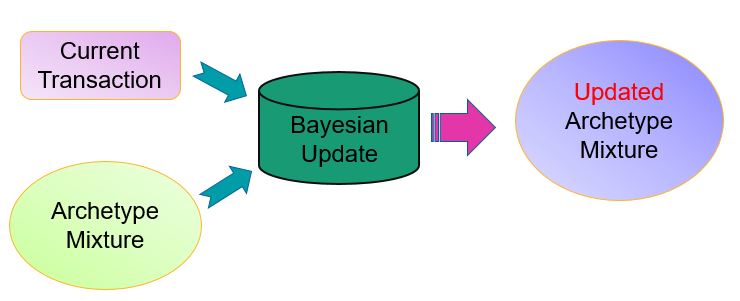

Upon receiving streaming transaction data, the collaborative profiling-enhanced Falcon model assigns and updates a cardholder’s archetype mixture in real-time (Figure 1 below). This is done by replacing the cardholder’s entire transaction history with their recent archetype mixture, a low-dimensional vector embedding of transaction history. We then can estimate the probability of the current transaction conditioned on the cardholder’s recent archetype mixture; high probability is expected based on the transaction history and low probability indicates a change of behavior inconsistent with the transaction history.

Collaborative profiling allows our corporate card fraud consortium model to differentiate between corporate cardholders and small-business cardholders based on the unique purchasing events that differentiate their transaction histories. These purchase history events are based on merchant category code, transaction amount and point of sale entry mode to precisely represent different these types of business card usage.

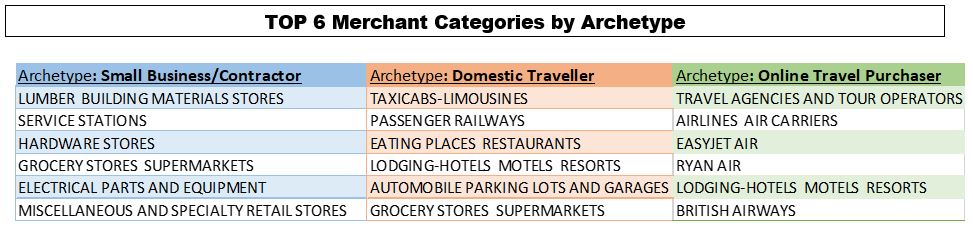

Figure 2 illustrates a sample of the archetypes. By looking at various statistics such as top merchant categories, rate of cross-border travel, and type of card transaction, these archetypes offer some immediate insights into the data, and whether it is likely to be the cardholder’s transaction or not.

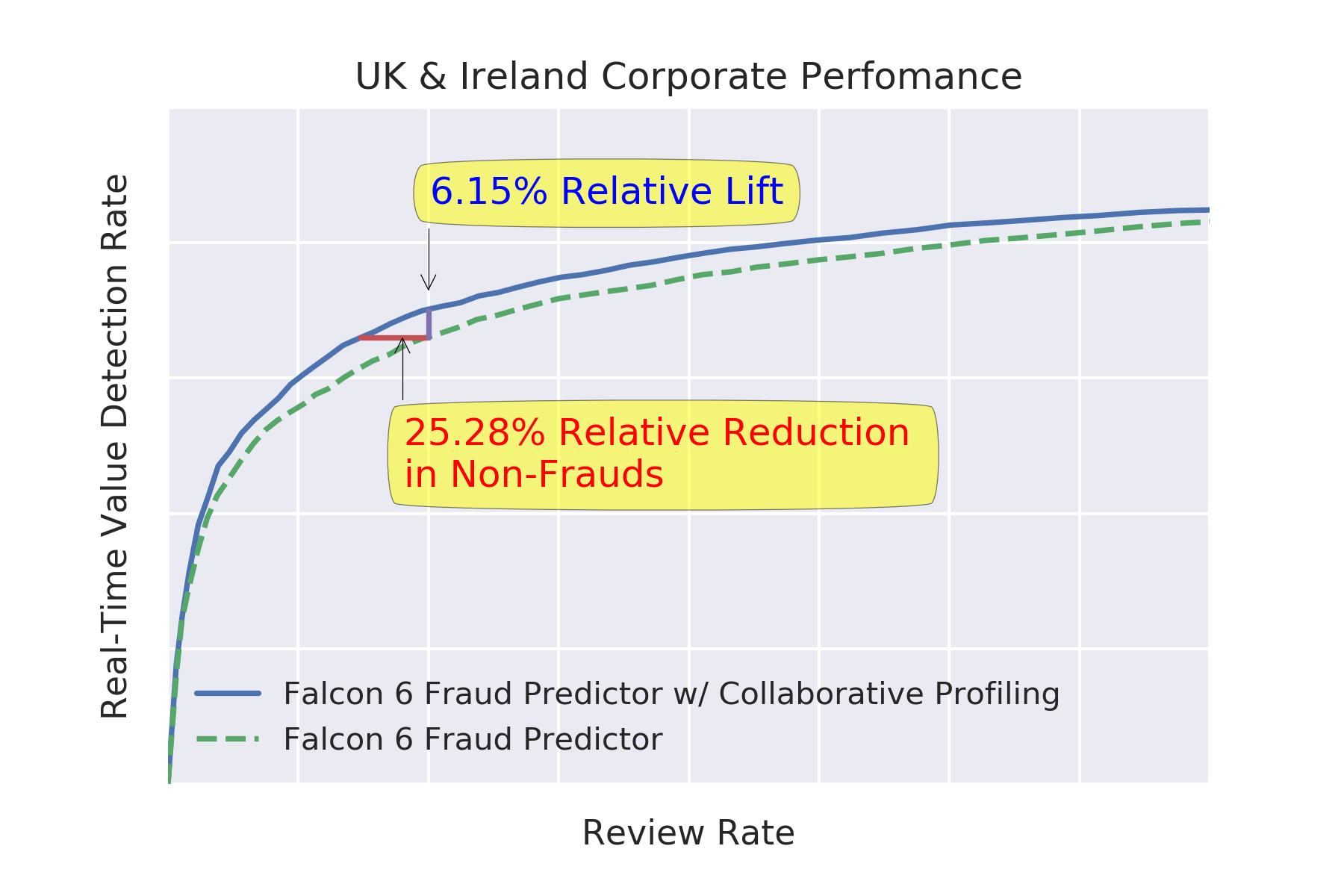

The advantage of using FICO’s collaborative profiling for payment card fraud detection can be measured in fraud dollars detected versus the number of false positives. Figure 3 compares the performance of the Falcon corporate card fraud models with and without collaborative profiling. With collaborative profiling, the real-time value detection rate shows a relative lift of 6.5%, as well as a 25% reduction in false positives at the typical non-fraud review rate for the UK/Ireland model. For the US model, collaborative profiling drives a relative lift of 2%, as well as a 10% reduction in false positives at the typical non-fraud review rate for the US model.

These improvements illustrate how FICO is using collaborative profiling technology to significantly reduce corporate card fraud losses while improving corporate users’ customer experience with fewer false-positive interruptions. In the marathon of fighting payment card fraud, FICO is winning the Corporate Challenge.

Follow me on Twitter @ScottZoldi.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.