UK Card Delinquency Roll Rates Creep Higher

Balance roll rates — overdue balances on UK cards that go from one 30-day cycle to the next without repayment — moved slightly higher in 2018. Our analysis of data from 11 card iss…

Balance roll rates — overdue balances on UK cards that go from one 30-day cycle to the next without repayment — moved slightly higher in 2018. Our analysis of data from 11 card issuers across the UK shows the areas that warrant attention from card issuers.

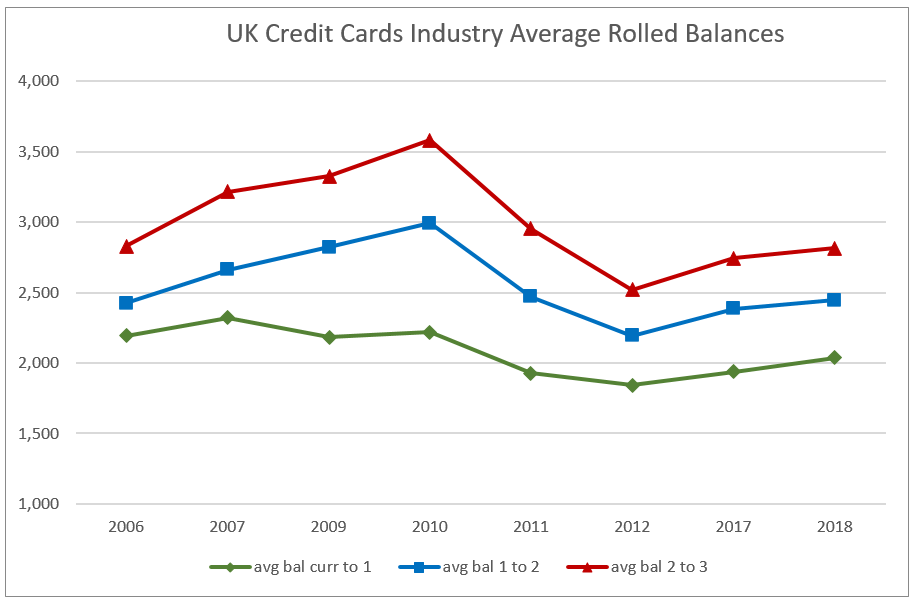

Average current to 1 cycle balance roll rates were at their highest in 2007, with 1 to 2 cycles and 2 to 3 cycles highest in 2010. Whilst 2018 values are noticeably lower than the peak, there has been growth from 2017, ranging from £2,039 to £2,817 dependent on the cycle.

The good news is that, with limits on cards higher now than in 2007 or 2010, the rolled balances are lower than in those years. The bad news is the steady creep up since 2012. This suggest that issuers should review their collections processes and strategies to determine if the focus is still appropriate, based on the current customer performance.

From Current to 1 Cycles

The percent of accounts and balances rolling from current to 1 cycle is at its lowest in the 8 years included. At their peak in 2006, 5.2% of accounts and 7.8% of balances rolled into 1 cycle. This has dropped to 1% and 2.1%, remaining stable compared to 2017.

What caused the drop? In part, issuers having access to a richer data source over the years, including more customer-level and bureau information, as well as the implementation of pre-delinquency campaigns. Issuers may be focusing on higher-risk segments in order accounts to try to reduce IFRS 9 provisioning levels. The more mature consumer subpopulations may be more cautious in their spending habits, with the last economic downturn still in their minds. It will be interesting to review the rates later in 2019 to gauge the impact of increasing minimum and general payments due to the introduction of the Persistent Debt regulations in September 2018.

From 1 to 2 Cycles

Accounts rolling from 1 to 2 cycles both peaked in 2006, but were also high last year. The November 2018 roll rates — showing 15.5% of cycle 1 accounts and 19.2% of cycle 1 balances rolling — were only exceeded in 2006 and 2009. The percentage of rolling balances are on a par with the 2009 value and if the rise continues will soon reach the 2006 levels.

Further analysis of the accounts rolling will determine help issuers determine which accounts to focus on in collections. Data-driven strategies are becoming more common in the Industry to determine the most effective data to segment based on bad rate. Taking this one step further and optimising the best next treatment will provide additional uplift.

From 2 to 3 Cycles

The highest percentage of accounts rolling from 2 to 3 cycles was reported in 2017, and in 2018 it fell to below the 2009 levels. The percentage of accounts rolling was 51.9% last year, and this represented 57.8% of balances, marginally down on last year, with the highest levels in 2009 (59.6%).

Roll-Back Rates

When reviewing roll-back rates, it is worth noting that individual issuer policies on reage and payment plans can influence results. However, over the years the reage policies have been tightened and consumers have to demonstrate the ability to maintain certain payment levels before their delinquency level is reduced. Regarding payment plans, as there is a mixture of approaches in the Industry, including allowing accounts to roll back or flow through delinquency, and this has not influenced the results.

The most significant year-on-year change for the 3 cycle roll-back results was for the percentage of balances curing. In 2017 the rate was 10% and in 2018 5.7%. However, the average balance curing increased by £1,597 to £5,156. This indicates for many issuers that there is a high proportion of smaller balances that could be targeted.

Industry 2 to 1 cycle rates remained stable since 2017, with just under 10% of accounts rolling. The largest difference was seen for balances and accounts curing, with balances curing decreasing from 26.3% in 2017 to 15.8% last year. Average rolled balances have remained stable.

The percentage of accounts and balances curing from 1 cycle has also reduced annually from over 71% to 61%. Average balances have marginally increased.

Further analysis by issuers could determine why these drops have occurred and may suggest strategic changes to address it.

Our Risk Benchmarking results from December show a worsening in the delinquency results in the market. This indicates that there may be a general downturn in performance, which could also be a contributing factor to roll rate results. Watch for my next posts on this topic and on static delinquency.

To learn more about our cards benchmarking service, or FICO’s Risk Benchmarking Service which forms part of the Fair Isaac Advisors P&L Insight Suite, please contact me at staceywest@fico.com.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.