COVID-19 Checklist for Banks: 6 Changing Fraud Patterns

As consumer spending patterns change in the pandemic, fraudsters are changing to match

The FICO Advisors team of consultants has just published our third COVID-19 bulletin to help banks adapt and thrive in these unprecedented conditions. Here are our observations on changing fraud patterns.

A consequence of the economic downturn is the blurring of lines between fraud and risk. It is now less clear whether a customer has obtained credit with no intention to repay for fraudulent reasons, or whether they have fallen on hard times through unemployment or other financial pressures. A review of how you define first-party fraud, treat suspicious behavior, and engage with customers is essential.

Both genuine customers’ and fraudsters’ behavior continues to change and adapt to a constantly changing environment. Fraud detection strategies need to adapt, too. Trends to think about include:

- The continuing move from card present to card not present (CNP) transactions

- The high-risk CNP mix has changed; airlines, travel, hotels, and entertainment no longer pose the same level of risk

- Increased contactless/token usage and transaction spend limits

- Increased genuine home-based insurance claims, as people spend more time at home and conduct home improvement projects

- Shift in the channel mix, resulting in more online/mobile registrations and usage

- The expedited move to digital interactions means less face-to-face interaction, less identity document validation opportunities and increased pressure in making quick and frictionless decisions. How can you continue to detect fraudulent activity while not negatively impacting the overall customer experience?

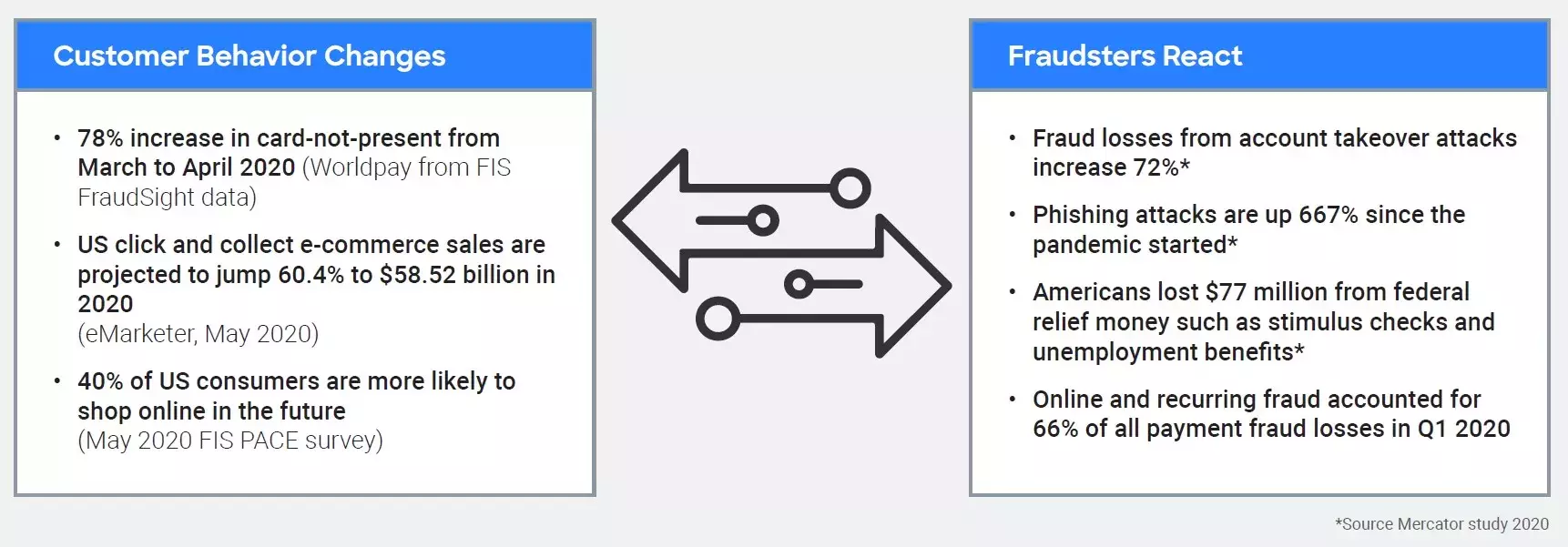

As shown below, these changes in customer behavior are driving changes in fraud patterns.

Want to learn more about responding to the pandemic challenge? Read our full bulletin: Coping with the COVID-19 Crisis: Adapting to the New Reality.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.