eKYC – Why Malaysian Banks Must Act Now!

Bank Negara confirmed in July 2020 that banks and other financial institutions could deploy eKYC as part of the onboarding process.

In December of last year, the Malaysian National Bank, Bank Negara, issued a consultation document about their intention to allow eKYC in the applications process for a wide range of financial products. Little did they know that Covid-19 was about to happen and that the requirement to validate customers’ identities remotely would become an even more pressing issue. Bank Negara acted and in July 2020 they confirmed that with immediate effect, banks and other financial institutions could deploy eKYC as part of the onboarding process. They even gave financial institutions the go-ahead to utilize artificial intelligence and machine learning to support their eKYC processes.

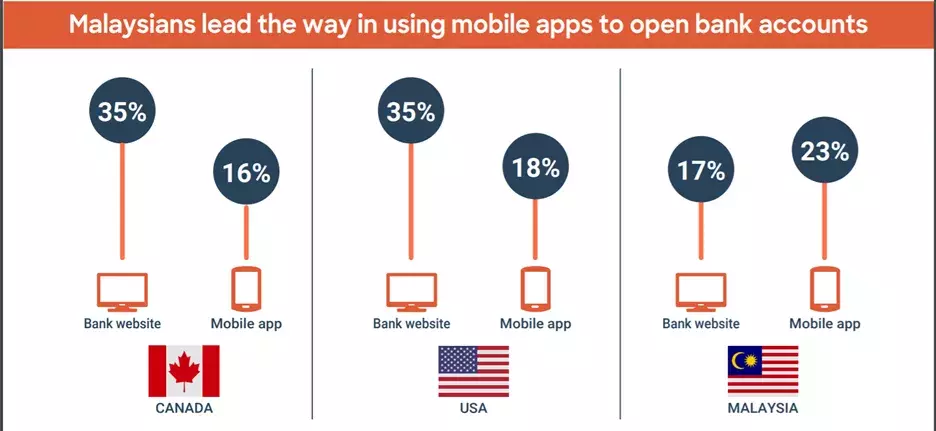

With face to face interactions limited due to the impact of Covid-19 the financial services sector can now look to grow their businesses using their websites and apps – but what will their customers think? FICO carried out a survey earlier this year with 500 Malaysian adults to find out. The news is promising, with 78 percent of Malaysians saying that they would open a financial account digitally. When we look at how Malaysians prefer to open digital accounts, it’s noticeable that while they lag some of the other countries surveyed in terms of their willingness to use websites, they are ahead of the curve when it comes to using apps.

The level of comfort Malaysians have with using apps – given they are predominantly mobile phone apps – is a vital factor for the success of eKYC initiatives. Customer journeys driven through a well-designed banking app with mobile phones used for face and document image capture, fingerprint capture, device recognition and keystroke analysis augers well for both account applications and the ongoing authentication of customers returning to use their accounts through their banking app.

When Malaysians open accounts digitally, they expect to carry out most of the associated tasks, including many of those related to eKYC using the same channel. 78 percent expect to be able to prove their identity and 46 percent to prove where they live using digital methods with 40 percent expecting to be able to set-up a biometric for future authentication. Not meeting these expectations could be costly. Less than half of customers forced to complete eKYC by mailing documents, taking them to branches or even by scanning and emailing will carry out those extra steps as soon as possible. Almost a quarter of applications will be completely abandoned – with the majority of those customers going to another provider.

Can Malaysian banks deliver on customers’ eKYC expectations?

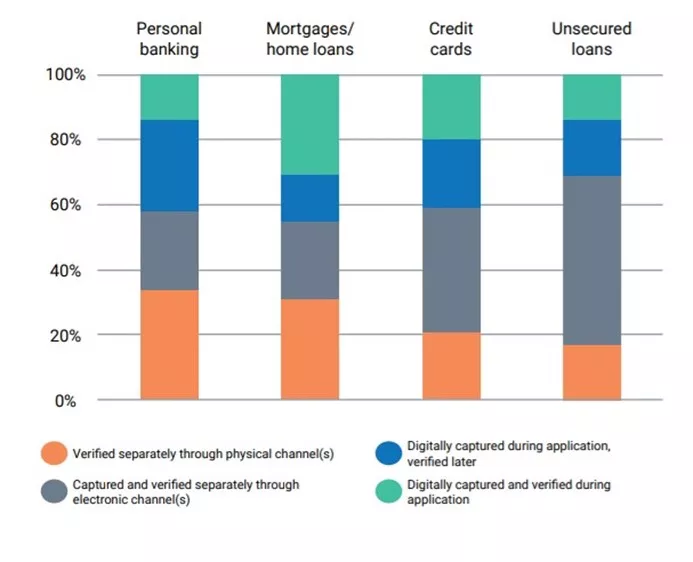

The consumer survey took place early in the global pandemic and while the direction of transformation was already clear it seems reasonable to expect that it has only accelerated given the restrictions we’ve all faced. Banks and other financial institutions need to act, but are they ready to do so? In May of this year analysts Omdia undertook an independent research project on behalf of FICO to uncover the customer identity management strategies of banks around the world including those in Malaysia and the Philippines. While there is still some way to go for banks in SE Asia when it comes to utilizing real-time digital identity capture and verification, they are out in front of some other regions. Many types of account openings still rely on verifying identity separately through physical challenges. Almost 40 percent of those trying to open a personal bank account digitally are forced to mail documents or visit branches to prove their identities.

This may in part be due to a technology gap, almost half of the banks surveyed said they had operational challenges related to the need to ‘physically’ validate customers’ identities and the manual processes required to do so. While most banks in the region (80%) have technology that uses character recognition (OCR) to extract data from identity documents, only a third have the capabilities needed to compare a ‘selfie’ image to an identity document or to verify the real-time presence of the applicant with a ‘liveness’ check.

These results suggest that most banks have some way to go but given customer’ preferences there is a distinct opportunity for those that are ready to get to grips with eKYC that will give them a competitive advantage in the near future

eKYC Malaysia – digital transformation success

Implementing a fully digital onboarding solution that combats fraud, enhances customer experience and meets regulatory compliance standards for eKYC may seem like a tall order – but banks in the region are not only managing to do so but are exceeding their already ambitious expectations. A leading Southeast Asian Bank worked with FICO to deploy an AI-based, biometrics solution to give them a seamless and secure digital platform. Within just five months they surpassed the 1 million user mark, way ahead of their initial year-end target of 100,000 users and have:

- Fast-tracked speed of customer acquisition for onboarding new customers with powerful AI

- Reduced customer inconvenience and diminished application abandonment rates

- Improved approval time from days to minutes, providing easy-to-use and integrated security across the customer lifecycle

- Met Central Bank compliance requirements to reduce fraud

How FICO helps

FICO® Falcon® Identity Proofing gives organizations the power of mobile identity verification. As part of FICO’s unified digital identity platform, Falcon Identity Proofing provides a seamless method for validating identities during the customer onboarding process and enrolling them as trusted entities. State-of-the-art facial recognition, liveness detection, document capture, hologram detection, and real-time corroboration ensure organizations take a balanced approach to user experience, providing easy-to-use, integrated security across the customer lifecycle.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.