Even in a Crisis, the Best Collections Strategy Is to Avoid Collections

With as much as 50% of consumers experiencing financial difficulty soon, it's time to review your early and pre-collections strategy and processes

With a cost-of-living crisis and soaring energy costs across Europe and other countries, it's important to re-evaluate debt collections and customer risk management strategies. Before I suggest some considerations for early collections strategies, we need to discuss one of the biggest factors driving collections tactics and performance today: regulation, in particular IFRS 9.

IFRS 9 marked the latest in a long line of International Financial Reporting Standards. This new standard was introduced in January 2018 and designed to help lenders and banks enhance their strategy and avoid unpleasant surprises presented in the shape of loan defaults, delinquency, or early collections processes. It also represented a regulatory stepping-stone put in place following the global banking crash of 2008.

Under pre-2018 accounting regimes, defaults were only reported as they happened. The discipline behind IFRS 9 imposed a duty of care on lenders to proactively anticipate and plan for expected credit losses and avoid debt collections well in advance.

IFRS9, Collections Strategy, Delinquency and Risk

As it now stands, IFRS 9 has split lenders into two camps. Some took it as an opportunity to look more holistically and pre-emptively at the operational back-office convergence between informed collections strategies, risk and finance. Others opted for a tactical stop gap to meeting the regulatory demands of compliance, involving more manual checking and work during every reporting cycle.

Any institution belonging to the latter camp may have also unwittingly reduced their chances of turning the regulation into a handy growth and efficiency opportunity. This was the opportunity to digitise risk management, delinquency and collections functions and make the most of risk-adjusted performance measures.

The Looming Post-Pandemic Downturn

The subject of financial fragility is again front-of-mind for all lenders thanks to the global economic challenges faced by all of us — from the squeeze on household incomes to rising inflation, spikes in interest rates, rampant energy costs and multiple supply chain challenges.

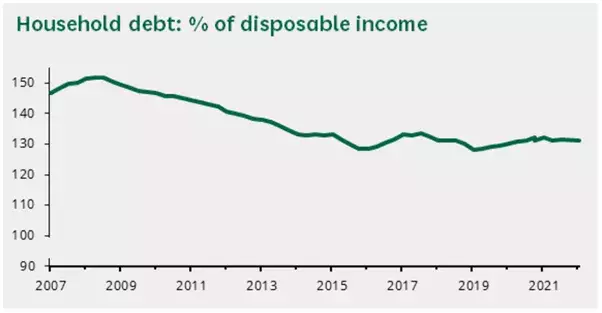

Source: House Of Commons Library

In the UK, the stats speak for themselves. Household debt as a percentage of disposable income peaked at 151.5% in Q2-2008. In Q1-2022 debt was at 131.3% — and rising fast amid predictions it may top 2008 levels.

Despite household spending being down due to savings getting plundered during the pandemic, it’s anticipated that UK consumer borrowing will reach a five-year high, growing a further 8% by the end of the year — equating to almost £16 billion. In England, individual insolvencies are 6.5% higher than in Q1-2021. In Scotland, they’re up 8% year-on-year.

But income segments are often impacted very differently. In July 2021, around one in five (21.6%) households from the lowest income quartile reported being in financial distress. This was set against one in 17 (6%) from the top quartile. More importantly, the gap between low-income and high-income groups has widened — and is increasing. Since July 2021, reported financial distress has continued to rise sharply for the first quartile, while the increase has remained consistent for the fourth income quartile.

It's not just the actual income challenge that determines consumer behaviour — consumer confidence also has a huge impact . Right now, consumer expectations about household finances have also deteriorated significantly during the past year — across all income segments, but especially among the poorest and most financially vulnerable.

Elsewhere across Europe, it’s a similar picture but with a very different range of scales. For example, June’s annual inflation figures ranged from 6.1% in Malta to 22% in Estonia.

One other factor significantly impacts customer behaviour. When policymaking starts influencing consumer safeguards, following damaging political and reputational fall-out from recession-driven pressures, we have in the past witnessed wholesale changes to customer behaviour and credit payment hierarchy.

Seven Considerations for Creditors

Creditors need to hone their collections strategies and process skillsets because IFRS 9 will come at a cost for the inefficient.

Regulatory scrutiny is increasing and it’s all about driving the right outcomes. In the UK, banks and lenders are looking at effective ways to comply with the FCA’s new Consumer Duty. Elsewhere in Europe, a slew of compliance challenges is already in place.

Retaining market share is critical. Creditors know they risk losing good customers that may offer enormous lifetime potential if they aren’t properly supported. But with the wrong treatments, poor support, or late action, they risk going elsewhere. And once a customer has been lost, they’ve generally been lost for good. Banking and financial services continue to be hugely competitive, with many institutions wrestling with a combination of legacy systems, siloed thinking and lean, competitive, new-to-market disruptors and fintechs.

Keep a careful eye on the cost of collections. It’s always worth noting that the moment a customer goes into collections their account will immediately be between 30% and 60% less profitable. If the account stays in collections for more than a month, there’s a direct risk it will have to retain an impairment, with the lost profit remaining on the lenders’ balance sheet until the product is repaid in full. The knock-on impact is a double whammy as it further reduces future forecasted profits, given a proportion of the credit balance is subsequently reported as a forecasted loss.

Plug in to quick wins at speed and scale. A slew of additional real-time data sources and insights are readily available, from Open Banking and public records to traditional credit bureaux and alternative data. The trick is converting all the information into meaningful insights that can drive well-informed action.

Many lenders still face challenges in achieving a comprehensive customer-centric view from their internal data. Successful collections strategies are underpinned by access to as wide a range of data as possible — especially real-time transactional insights, credit utilisation, income and spending behaviour. The ability to quickly assess where financial difficulties are coming from and in what shape, select the best way to engage with the customer and proactively offer the most appropriate help, are all vital.

It’s a tricky balancing act. Pre-collections strategies are arguably the hardest place to get customer communications right. Too little, too late and its costs. Too much, too soon and the customer risks being alienated by a perceived over-reaction or simply become suspicious. Neither ends happily.

What does ‘good’ look like? The right results will see customers prevented from needlessly rolling into collections. Clearly, there are customer loyalty and regulatory benefits to proactive action. But financially it’s also likely to be a key lever on the balance sheet.

Top performers are actively delivering a carefully considered collections strategy, regardless of the economic position at any given time. In the UK, there’s a constant degree of preventative activity underway around helping customers avoid persistent indebtedness. But other benchmarks include strictly imposing minimum card payment, or maximum borrowing set as a ratio of income. Despite that many lenders aren’t as proactive as they could be.

Forecast for the Near Future

For the next few years, it’s not simply a matter of spotting the 5% of accounts that have a high probability of rolling into collections. Pre-collections activity is set to become a key focus area for customer management teams across all portfolios.

We’re likely to see a blurring of the organisational, policy and process lines between collections and customer management. Either customer management functions will need to adopt some of the dynamic attributes of a best-practice early collections strategy and forbearance assist function, or collections functions will need to recognise that a growing proportion of their book will have a very different return-to-good profile. Collectors, if they undertake to manage 20% or so of the good customers, will need highly efficient and effective capabilities to operate at scale and in an agile way.

Irrespective of the implications set out by IRFS 9 in not proactively managing down the pending risk posed by inefficient collections, forecasts indicate that up to 50% of consumers are going to experience financial difficulty soon. At some point these customers will need highly effective support. While there will be multiple ways to address the challenges to be faced, it’s probably fair to say the best collections strategy will always be to avoid collections altogether – if possible.

How FICO Is Helping

All the key requirements outlined above, and the capabilities required to deliver them, are proven components of the FICO Platform. It enables our customers to manage complex data flows, drive deep customer insight, understanding, and make real-time decisions on appropriate treatments and engagement approaches for customers. It improves customer interactions through digital and traditional channels, with optimized approaches that consistently deliver the most appropriate business and customer outcomes.

Learn More About Pre-Collections and Informed Collections Strategies

- Watch a video on why customer-centric debt collection is critical.

- Find out why digital-first collections means thinking like a marketer.

- Read more background to the IFRS 9 learnings on models and operations.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.