FCA’s Consumer Duty Mandates Sharper Use of Technology

Managing UK customers to better outcomes under the FCA’s Consumer Duty will require a true platform for understanding and action

Every UK bank, lender and financial services firm is likely to have the FCA’s Consumer Duty front-of-mind right now.

The regulatory clock's rapidly ticking down on a deadline ahead of the new rules coming into force in July 2023. They apply to both new and existing products and represent one of the single biggest compliance overhauls since the publication of the regulator’s Treating Customer Fairly Initiative in 2006.

Crucially, the emphasis under the Consumer Duty is firmly on companies to continually prove they are consistently delivering good customer outcomes. Failure to uphold the new rules could result in sanctions and financial penalties.

While it’s being applied in the UK, we’ve often seen other regulators follow Britain’s lead, as was the case with Treating Customers Fairly. They’re also sound business practice and a solid pathway for dealing with customers – irrespective of where business is being transacted.

Source: fca.org

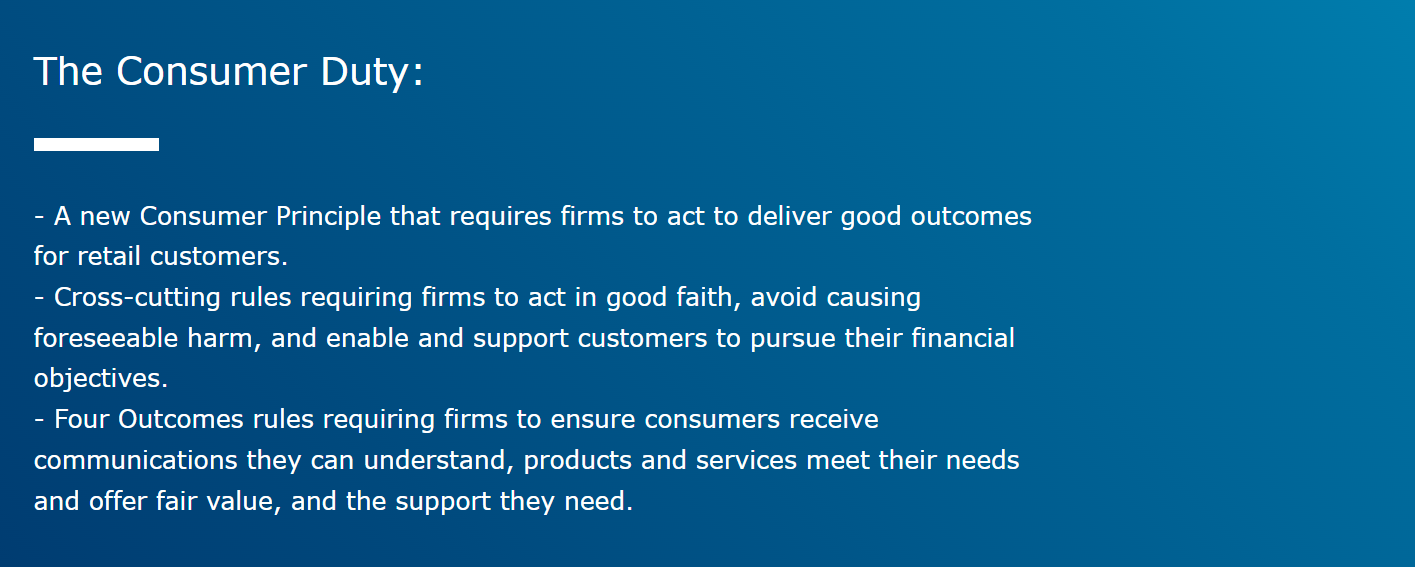

Structure of Consumer Duty

The Consumer Duty brings a 12th principle into the FCA Handbook, known as the Consumer Principle. It gives a simple instruction that firms “must act to deliver good outcomes for retail customers”. While a straightforward enough statement, it’s a clear indication of the intended laser focus on the outcomes experienced by customers.

Guidance in relation to how firms should act to deliver the required outcomes for customers is in the form of three so-called “cross-cutting rules”, which apply across the outcome areas of the Consumer Duty.

Source: fca.org

Three Cross-Cutting Rules

1. Act in good faith towards retail consumers

It may sound obvious, and in line with the existing requirements around the fair treatment of customers, but the FCA is reinforcing the expectation that firms design their products and conduct all of their dealings with consumers in a way that is open, honest and supports the financial objectives of customers. It’s good to see the requirement to avoid bias and prevent the amplification of biases that can lead to harm. From an execution standpoint, those working with algorithms for machine learning or artificial intelligence will now need to ensure interpretability and explainability of decisions, so that firms can objectively justify differences in outcomes.

2. Act to avoid causing foreseeable harm

Firms are now required to proactively prevent foreseeable harms that could be caused to customers through action, or inaction. Harm is considered foreseeable, when a prudent firm acting reasonably would be able to predict or expect the harmful result. Firms should ensure that offers and communications are designed and tested so that they deliver good customer outcomes. They will also need to test the performance of their products to mitigate harms.

3. Enable and support customers to pursue their financial objectives

Firms must provide a level of service to customers and communicate with them in a way that supports informed and timely decision making. Crucially, firms must proactively and reactively focus on putting customers in a better position - even if the firm declines to provide a particular product or service to a given customer. Consideration should also be given as to whether there is information or support available. It’s vital that firms think about all customer interactions to make sure they are as smooth and understandable as possible.

The application of these rules within four key outcome areas makes up the detail of the Consumer Duty. Firms that are able to comply with all three rules, within each of the outcome areas, are likely to see customers experiencing the best outcomes.

Why Platform Technology is the Springboard to Enabling Better-Informed Customer Decisions

The scale of the data challenges many firms now face with this regulation shouldn’t be underestimated. Plenty still have siloed data across marketing, credit risk, customer management, fraud, compliance, and collections operations. The siloes prevent key data from being available for decisions across the entire customer journey. There’s also the issue of individual departments deriving inconsistent outcomes, as a result of using their own versions of decision logic within localised systems and without considering the insight that exists elsewhere in the enterprise.

To understand how products are performing across the entire customer journey, firms need to remove business siloes and share intelligence. They need transparency and confidence in decisions that they make, which means that many will no longer be able to simply optimise performance for their individual parts of the business. By truly using data at an enterprise level, it’s clear to see how customers with a certain type of profile have behaved in a particular way and subsequently decide what you to do with the insight.

Greater collaboration is going to be needed across teams to understand the interactions with customers and their impacts across the journey. Success hinges on data, insights, actions and outcomes. Anything less than using a platform approach to managing decision assets will inevitably result in inconsistent outcomes and unnecessary customer harm.

The Four Consumer Outcomes

1. Consumer Understanding

Customers must be offered the information they need when they need it and in a clear way. There’s an expectation that as much effort will go into ensuring post-sale communications are as clear and effective at informing customer decisions, as those used at the point of sale.

It’s not just about providing advice and guidance people can easily understand, but also making sure it’s tailored and relevant to them. It’s also crucial to know the intended audience and be confident that both communications channel and what is said are appropriate. Rather than simply surveying customers about the quality of service, firms will now need to delve deeper and specifically ask consumers if they understand the information provided and whether they have further questions.

2. Value for Money

No surprises here. Every customer expects “fair value”. But the FCA goes a little further defining it as: “The relationship between the amount paid by a retail customer for the product and the benefits they can reasonably expect to get from the product.”

Importantly, when assessing whether a product represents fair value, market rates and prices for comparable products can be considered. Margins, differential pricing and fees are all likely to come into focus as firms review their product portfolios.

3. Products and Services

Getting the most appropriate products in the hands of suitably well-informed customers and prospects is key. It requires a deep understanding of customers as individuals, as each product has to be designed with a specific target market in mind. Selling a product to a customer outside that target market could potentially be to their detriment.

The means by which products are distributed is also a critical consideration for the regulator. Distribution strategies must be designed that align to the needs and characteristics of the product’s target market.

4. Consumer Support

In all interactions with its customers, firms should seek to provide customer service that enables them to get the expected benefits from their product and pursue their financial objectives. This involves taking account of customers’ needs and characteristics, to the extent that individual requests for specific amendments should be met, where reasonable.

Service levels, abandon rates and complaints will all be under review from the regulator – it’s time to think about how unreasonable barriers to solving customer issues can be removed. With an emphasis on providing flexible support models, we will see greater numbers of customers moved away from the call queue.

The treatment of customers who are experiencing financial difficulties also needs focus. Proactive and customer-centric pre-delinquency campaigns — where solutions are tailored to the individual to stop them falling into arrears — are the very definition of seeking to avoid foreseeable harm. For those customers do still make their way into arrears, adapting the collections approach to each customer’s circumstances and needs can drive better outcomes for both firms and customers. Providing omni-channel and self-service capabilities can create the clear lines of communications and space that customers need to support an increase in resolution rates and a return to sustainability. Live conversations about managing debt can be awkward. Typically, it's a conversation customers often try to avoid. But automated technology actually empowers and improves consumer support thanks to its adaptable omni-channel features. It eliminates any embarrassment many late payers feel when they're speaking to an agent.

There are smart routes and quick wins to making matters easier, and here at FICO, we see it every day. Companies are embracing a self-serve two-way digital dialogue. It's already a proven winning communication strategy and when executed properly, companies can expect to see a significant uptick in customer engagement and operational efficiencies. It also helps identify where a company should focus its efforts and at the same time delight customers who appreciate the anonymity of this debt collection communication approach.

Customer Characteristics and Vulnerabilities

The FCA is also clear about the requirement for customer characteristics to be taken into consideration within all of the cross-cutting rules and customer outcome areas. This includes their resources, degree of financial capability or sophistication and reasonably foreseeable customer characteristics. This greatly moves the needle from simply ”tick-box compliance” to a greater level of data-driven customer understanding.

It is now vital to have a detailed understanding of a customer to be able to understand whether they form part of a target market, what their communication requirements are and, crucially, whether there are any signs of vulnerability. These must be taken into consideration throughout, planned for and tracked. It’s a fundamental expectation and is emphasised by the requirement to investigate any unexpected or adverse outcomes within particular groups.

Good Governance Is Always Worth the Investment

Governance is everything – from avoidance of regulatory risk to upholding reputational value in the marketplace. In the context of Consumer Duty, there’s a requirement for ongoing self-assessment and testing of outcomes. These all have to be clearly evidenced and reported back to the FCA. Customer outcomes should also become a focus of every firm’s internal audit team, regardless of where they’re based. Good practice is good practice the world over.

It’s also worth noting that firms will be expected to report their findings to governing bodies, on at least an annual basis. Submissions will be followed by a formal review and conclusion regarding compliance. Reviews must not only be regular, but sufficiently granular to all identification of groups of customers, who may be deemed to be receiving poor outcomes. Agreement of remedial activities must then be outlined as and when they’re required. Most firms are now expected to task and mandate an executive team to focus on customer outcomes.

All of this places a significant emphasis on having access to the data which can evidence the decisions and actions taken. It’s a significant challenge for many firms as it requires the use of large volumes of data from disparate sources.

How FICO Is Helping

All the key requirements outlined above, and the capabilities required to deliver them, are proven components of the FICO Platform. It enables our customers to manage complex data flows, drive deep customer insight, understanding, and make real-time decisions on appropriate treatments and engagement approaches for customers. It improves customer interactions through digital and traditional channels, with optimised approaches that consistently deliver the most appropriate business and customer outcomes.

Learn More Here

- Read the blog Even in a Crisis, the Best Collections Strategy Is to Avoid Collections.

- Watch a video on why customer-centric debt collection is critical.

- Find out why digital-first collections means thinking like a marketer.

- Read more background to the IFRS 9 learnings on models and operations.

- Read the blog Empower Your Customers to Self-Serve With Digital Omnichannel Communications.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.