FICO Resilience Index Now Available for Lenders to Pilot

FICO works to keep credit flowing during uncertain economic times

Today, FICO announced the FICO® Resilience Index, a new analytic tool designed to complement the industry standard FICO® Score. During economic uncertainty, lenders and investors need to be able to evaluate and balance portfolios based on rapidly changing conditions. This helps further the safety and soundness in credit, as well as support the global economy. By actively working with lenders and consumers to navigate the current situation, it is apparent that precise analytics are as important as ever to help avoid over-tightening of credit which can delay an economic recovery.

The FICO® Resilience Index is designed to give lenders and investors a refined tool to help identify those consumers across FICO® Scores bands that represent higher resilience during an unexpected economic disruption. For instance, higher-resilience consumers tend to have:

- More experience managing credit

- Lower total revolving balances

- Fewer active accounts

- Fewer credit inquiries in the last year

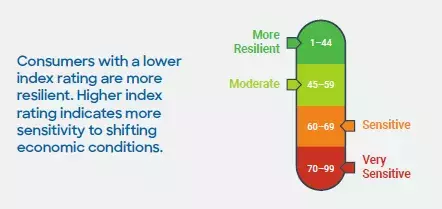

The FICO® Resilience Index’s scale provides an additional layer of insight to help more accurately capture the resilience of a consumer and empower lenders to provide access to credit during difficult economic times. Unlike the FICO® Score, which ranges from 850 to 300, the FICO® Resilience Index outlines a scale from 1-99. Consumers with scores in the 1 to 44 range are viewed as the most prepared and able to weather an economic shift.

Analysis of FICO® Resilience Index data by Tom Parrent, former chief risk officer for Genworth Financial, shows that from 2010 to 2015, nearly 600,000 additional mortgages could have been originated to consumers with FICO® Scores between 680 and 699, had the FICO® Resilience Index been available to lenders at the time. In a new white paper, Mr. Parrent calls the FICO® Resilience Index, “a significant step forward in consumer credit modeling” and “a significant addition to the toolkits used by risk managers, portfolio managers, loan servicers, originators and regulators,” with a wide range of use cases for the mortgage industry, ranging from stress testing to risk-based pricing to loan servicing.

By studying past recessions, we know that in a down economy credit criteria goes up and access to credit goes down as lenders try to mitigate credit risk. The FICO® Resilience Index can be helpful in navigating through changing economic cycles. The desired outcome is for lenders, borrowers, and investors to benefit from a system that is even more precise in assessing risk, and less prone to broad credit restrictions and undifferentiated risk pricing, which can tighten the flow of credit during an economic downturn.

The FICO® Resilience Index can also help address:

- Better Portfolio Management – Lenders can use the FICO® Resilience Index to better gauge and manage overall portfolio vulnerability, by providing a new way for risk officers, regulators and investors to monitor the quality and resilience of a portfolio throughout economic cycles – and evaluate the effectiveness of actions taken to improve resilience and ultimately reduce losses.

- Regulatory Stress Tests – By actively managing FICO® Resilience Index distributions to build more robust portfolios over a full market cycle, financial institutions can more precisely set capital requirements to comply with the Comprehensive Capital Analysis and Review (CCAR) and Dodd-Frank Act Stress Tests (DFAST).

- Better Loss Allowance Estimations – FICO® Resilience Index helps lenders identify more resilient consumers so that they can optimize capital and reduce loan loss allowance estimates.

- Transparency within Secondary Market – Currently, FICO® Score distributions along with additional data points are used to gauge the overall risk of portfolios. The FICO® Resilience Index adds another layer of data and insight to help indicate resilience of the overall portfolio.

Building on FICO’s legacy of innovation for over 30 years, the FICO® Resilience Index is the latest solution designed to enable lenders with a more precise assessment of consumer credit risk. The tool is now available to lenders from multiple credit bureaus.

For more information, listen to my recent FICO virtual resilience keynote.

Read the whitepaper from Tom Parrent, Principal, Quantilytic.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.