Fraud Analytics for Open Banking: Behavioral Profiling

Behavioral profiling approaches are extremely important in tackling fraud that happens when banks share financial data with third parties through application programming interfaces…

Digital banking channels are increasingly popular, and behavioral profiling of customers is vital in preventing new types of fraud. The open banking revolution makes understanding each customer’s behavior even more important in preventing fraud by considering all the aspects of transactions. Transactions in the world of open banking contain data not previously seen in the payments ecosystem.

Behavioral profiling approaches are extremely important in tackling fraud that happens when banks share financial data with third parties through application programming interfaces. The behavioral profiling in the FICO Falcon Platform leverages historical details to track a customer’s patterns, including:

- typical spending velocity

- the hours and days when they tend to transact

- which foreign countries they have transferred to before

- favorite beneficiaries

Transaction Profiles

Transaction profiles enable FICO Falcon Platform to detect subtle, yet anomalous changes in behavior and elevate the score on the transaction. Each profile is a continuous learning cognitive “mini-model” that uses machine learning to interpret behavior in real-time.

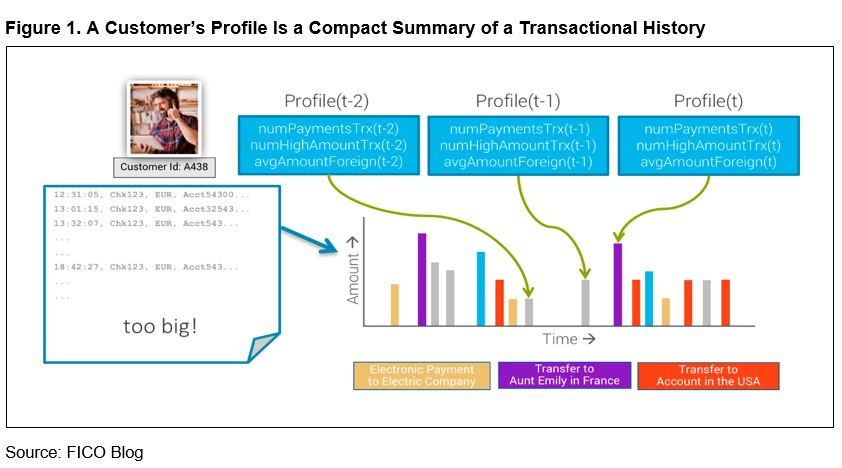

Profiles compactly summarise each customer’s transactional history, which is too big to be retrieved when a decision has to be made in milliseconds (Figure 1). This is why we require streaming analytics.

Transaction profiling, applying Kalman filter principles, creates a profile for each customer. This is updated in real time, with each transaction, to account for behavioral changes.

Profiles are:

- Recursively updated; computing the estimate for the current profile state only requires the estimated profile state from the previous transaction and the information connected with the current transaction.

- Composed of numerous monetary and non-monetary parameters that are continuously updated to enable adaptive behavioral profiling.

- Memory-efficient and do not require extensive storage space.

In practice, when a transaction enters the FICO Falcon Platform, the system pulls a profile connected with that transaction. The system updates the variables stored in that profile, and uses the updated profile to produce the final score, which indicates the likelihood of fraud.

Understanding Recurring Behavior

People form habits, and by looking at their transactional history we can learn their frequent behaviors. Generally, customers use the same devices, such as computer or mobile phones, go to the same online merchants and transfer money to repeated beneficiaries. These recurrences can be analysed and understood to shine further light on normal behavior, and thus on fraud.

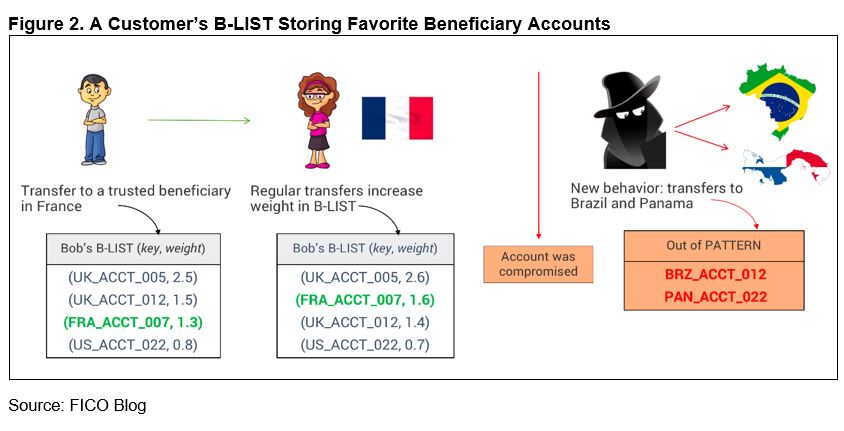

To understand recurrences, FICO Falcon maintains behavior-sorted lists or B-LISTS, which enable the system to create a real-time ranking of features associated with each customer’s most frequent behaviors.

By using machine learning, the system makes sure that only the activities that keep recurring remain in each customer’s B-LIST. Frequent activities have higher ranks and are less likely to be fraudulent.

In Figure 2, money transfers to the same beneficiaries have higher weights in a customer’s B-LIST and are less likely to be fraudulent. On the other hand, money transfers to destinations that are not included in the customer’s B-LIST are substantially riskier. FICO’s B-LIST technology is a powerful facet of the transaction profile.

The open banking changes, specifically the need to fight fraud and keep genuine customers happy, means that behavioral profiling at the individual customer level is crucial. Each customer’s profile, including transaction profiling and B-LIST technology, is a “mini-model” that uses machine learning in order to learn highly detailed behavioral patterns of that customer in real time.

Learn More

For more information, see my previous post on fraud analytics.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.