Fraud & Payments Predictions 2019: Go Cashless - with Care

TJ Horan explains how his wallet diet paid off - and what this means for fraud in 2019.

As far as industry predictions go, perhaps surprisingly, one of mine actually came true: “2018 will be the beginning of the end for physical credit cards. However, their functionality will become even more omnipresent in our lives as more cards migrate to consumers’ mobile phones.”

It’s true that more and more Americans are adopting mobile payments. In May Recode reported, “By the end of this year, a quarter of U.S. smartphone users — 55 million people — over the age of 14 will make an in-store mobile payment. More than 40 percent of those people will have done so through Starbucks’s mobile payments app…” (That’s a lot of lattes.) Meanwhile, Chinese consumers are already the world’s top mobile spenders by far, racking up trillions of dollars in mobile payments.

The Next-Level “Wallet Diet”

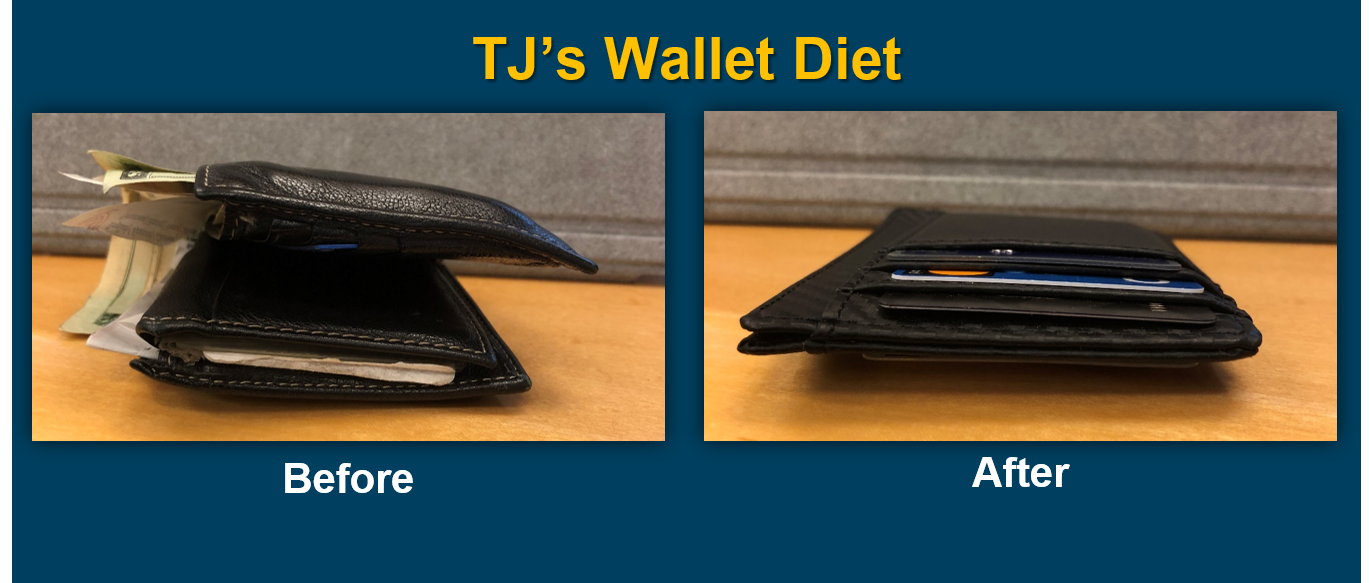

My 2018 prediction, dubbed “the wallet diet” on the FICO blog, was laughed off by many as an impossibility, their own wallets stuffed with cash, cards, receipts and the odd losing lottery ticket. A year later, my “George Costanza wallet” contains only a couple of physical cards; the functionality of the rest has transferred to my smartphone. Seriously. My wallet headed into 2019 is about 1/10th the size it was at the start of the year.

My 2019 prediction is that my newly trimmer wallet will be even thinner by next December. I’m predicting that I, along with millions of other consumers, will go cashless in 2019.

Anecdotally and empirically, we know that countries like Sweden are nearly cashless (900 of the country’s 1,600 bank branches don’t even deal in any cash) while others like Germany are comparatively card-free (only 36% of Germans over the age of 15 even have a card). There’s hard data that supports America going cashless; in April creditcards.com reported:

Three in 10 Americans say they never or rarely carry cash anymore, according to new data from Capital One, with millennial women in the Southeast and Southwest being the least likely to have cash on hand.

Male baby boomers on the West Coast, on the other hand, are far more likely to have greenbacks in their wallet.

Capital One’s survey of consumer spending habits found that while a full third of women report they never or rarely carry cash, less than a quarter of men (22 percent) say the same.

Meanwhile, Americans age 18-35 are the least cash-carrying generation, with 34 percent indicating they generally go cashless, while the share dropped to just 25 percent among baby boomers, who are age 55 and older.

Mobile Transactions Are the Fabric of Life

Here’s why I think Americans, even laggardly West Coast male baby boomers like myself, will go cashless in 2019: it’s finally easy enough. I noticed a marked difference in the ease of making mobile transactions in 2018 during my extensive travels for FICO; it’s getting incredibly easy to conduct nearly every everyday transaction with a smartphone.

- A car to the airport? Uber or Lyft.

- A train into city center? Use the city’s transit app.

- Hotel? At some hotels I can use my phone to both pay for the room and get inside it, avoiding long lines at the front desk.

- Stopping by a farmers’ market to catch a slice of life? Most vendors now prefer to accept payment via phone.

In 2019 I predict that mobile transactions will become even more seamless, making for a hockey-stick chart of their adoption.

Once again, I’ll use my own experiences as a yardstick of averageness. For years I’ve had Ziploc baggies full of foreign currencies, ready to pick up when I leave for another trip to FICO’s far-flung offices. The thought of landing in a foreign land without cash was just, well, something you didn’t do. I recently ran out of euros and considered whether I’d pick up a new supply as soon as I landed and cleared immigration, my usual routine. But after I deplaned I didn’t even think of it — I rushed out of the airport, in true George Costanza fashion, to cross the street to the train station, dodging cars as I did. And my euro Ziploc now remains empty.

Will Fewer Cash Transactions Result in More Fraud?

As a larger portion of cash-based transactions (no matter how small) are replaced with digital transactions, the number of opportunities for fraud will naturally increase. I’m not talking about digital credit card transactions where the fraud losses are relatively stable, I’m referring to new payment vehicles that are tied to retail banking accounts.

Consider this: If someone were to steal the cash in my wallet they’d get $40 (maybe $60 on a good day). If they were to steal (or take over) my mobile payment account, the losses would quickly become much worse.

My third 2019 prediction is that fraud losses associated with mobile payment apps will get worse before they get better.

At least in the United States, real-time payments are relatively new and the fraud defenses are simply not as mature as they are in the credit card space. This rapid acceleration towards cashless consumers will stretch existing fraud defense across several dimensions.

Best wishes for a cashless 2019! Follow my fraud-fighting travels on Twitter @FraudBird.

+++

While you’re here, why not check out our other prediction pieces for 2019

- Government Predictions 2019: Automate, Enhance and Secure

- Cyber Predictions 2019: The Year of Cyber Insecurity

- Analytics Predictions 2019: Machine Learning & Data Efficiency

- Consumer Banking Predictions 2019: Four Trends to Watch

- Public Policy Predictions 2019: Regulatory Reforms Ahead

- Collections Predictions 2019: SOP Won’t Cut It

- Analytics Predictions 2019: Innovations for Ethical AI

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.