How to Address Portfolio Risk Volatility Through Economic Uncertainty - Part 4

Building resilience into Collections & Recovery

Properly managed, the debt collections process can be an effective customer service and anti-attrition tool. Financial impairment resulting from unanticipated events are often temporary. Such events cast many borrowers into uncomfortable territory, creating what may be a defining moment in the relationship between them and their lenders. Lenders who get it right may earn a loyal customer for life, while those who misfire risk cannibalizing valuable relationships that often span multiple products.

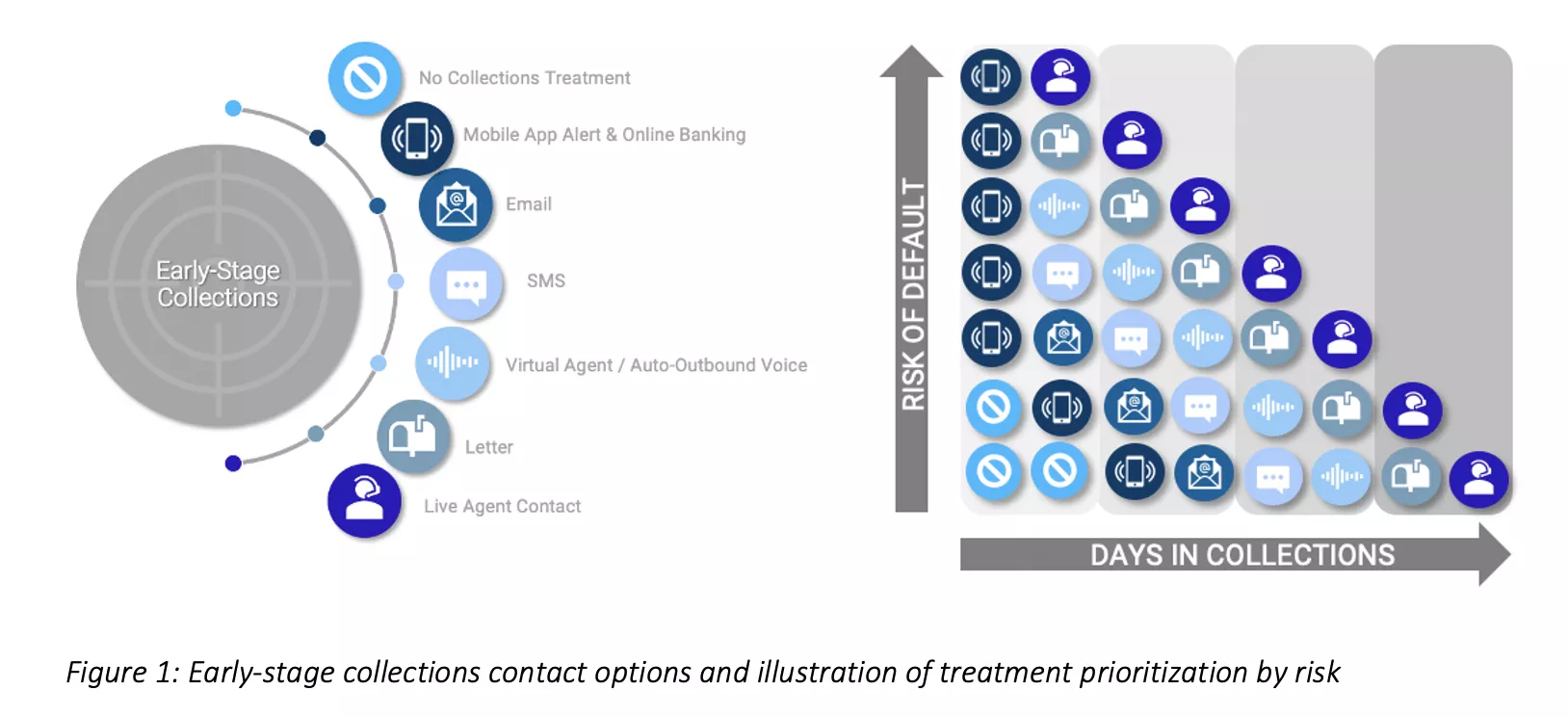

Nowhere are the stakes higher than in early-stage collections, where the uncertainty of outcomes and the range of treatment options are the greatest. Early-stage collections treatments offer a wide range of choices around channel as well as timing, tone, and intensity (i.e., penetration rate) of live-agent contact calls (Figure 1).

With so much on the line, it creates a lender imperative to leverage a precise view of risk profiles to best target customer treatments. Key questions include:

- Which borrowers in early-stage delinquency have a high likelihood to self-resolve with little or no collections intervention?

- To whom should we apply the least invasive initial collections efforts such as reminder emails, courtesy text alerts, and virtual agent (i.e., IVR) contacts?

- Conversely, which customer segments have an elevated probability of default warranting live agent contact and more forceful early intervention options?

Answering these questions correctly is crucially important. Underestimating less resilient delinquent borrowers’ default risk under stress results in a reduced collections priority, allowing other creditors to compete more effectively for limited repayment resources. Conversely, overestimating more resilient borrowers’ risk at such times may drive unduly aggressive collections tactics that improve short-term debt collection but jeopardize the long-term customer relationship.

In this blog post, we examine how the behaviors of resilient and sensitive delinquent borrowers differ, and how FICO® Resilience Index can enable a more efficient and effective collections strategy that balances short-term cash collection and longer-term customer relationship goals.

Sensitivity profile comparisons reveal value of FICO® Resilience Index in driving collections priority

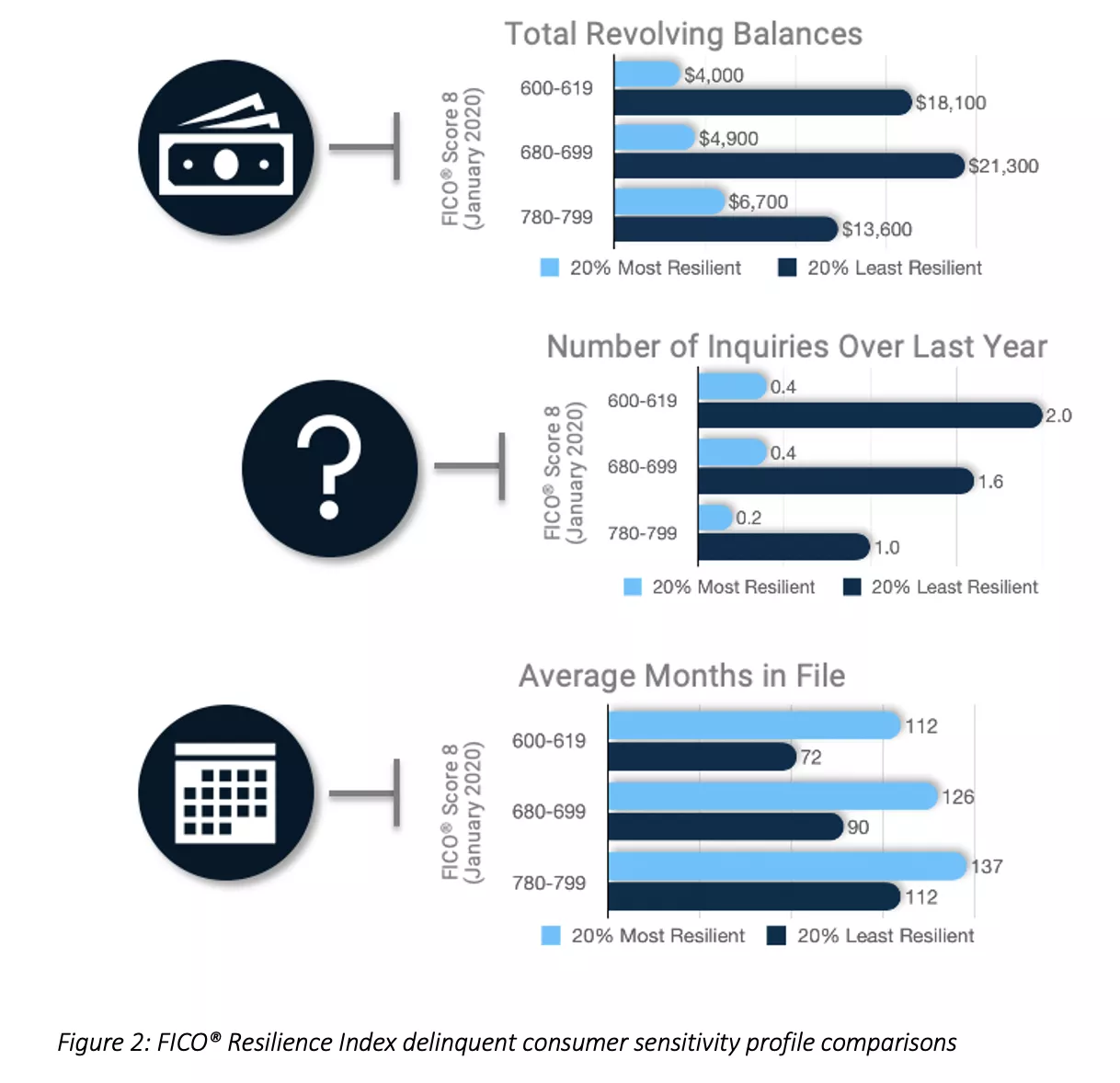

Comparing credit usage profiles of resilient and sensitive consumers with existing 30+ day delinquent tradelines highlights the value of FICO® Resilience Index to customize collections treatments. As seen in Figure 2, the 20% least resilient delinquent borrowers carry significantly higher revolving balances, have more aggressively pursued new credit, and have markedly less credit experience as compared to their 20% most resilient counterparts across the full range of FICO® Scores. Less resilient borrowers within a FICO Score band should therefore be prioritized during stressful times as both their probability of default and outstanding balances tend to be higher, resulting in larger overall credit losses.

Repayment performance for delinquent consumers post-recession

Our previous blogs about building resilience into customer acquisition and customer management confirmed that resilient consumer segments consistently outperformed sensitive ones within narrow FICO® Score bands as the economy transitioned from an unstressed to a stressed environment.

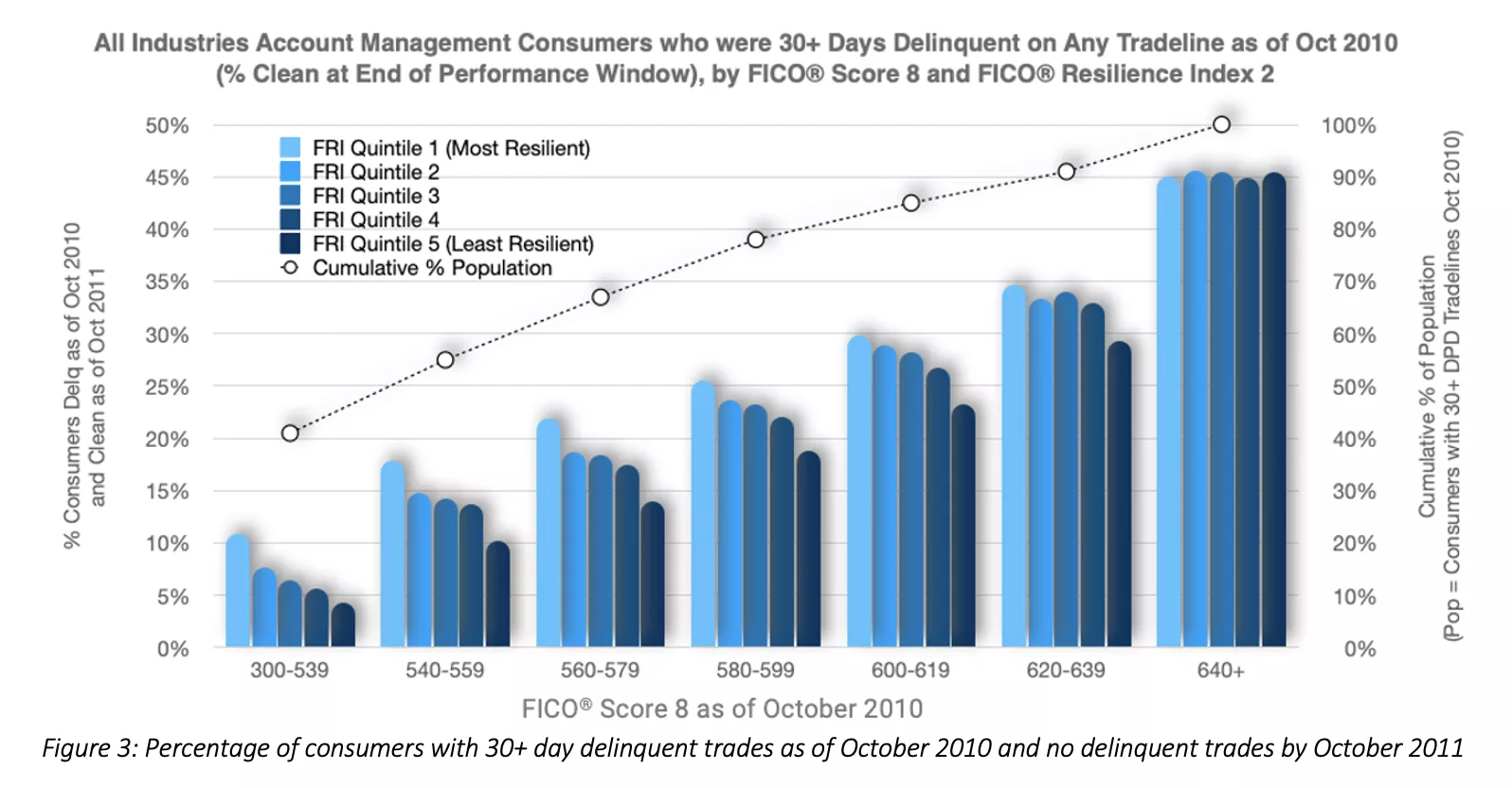

But what can we expect within less resilient delinquent consumer segments as the economy begins to recover from a downturn? Using the period following the Great Recession as a point of reference, we isolated consumers in October 2010 with 30+ days past due delinquent tradelines and analyzed their ability to return to current status, as well as their likelihood of experiencing new serious delinquencies, over the year of economic recovery that followed.

Figure 3 shows the percentage of these delinquent consumers who had clean credit files (i.e., no 30+ day delinquencies) a year later. Within FICO® Score bands below 640, which collectively represented 91% of the delinquent population, FICO® Resilience Index quintiles (reverse) rank-ordered borrowers’ ability to “bounce back” as the economy recovered from its prolonged disruption, especially in the lowest FICO Score ranges where more delinquent consumers reside. For example, in the sub-540 FICO Score population, which alone captures 41% of the existing delinquent borrower population, the most resilient consumers are 2.5 times more likely to become clean than the least resilient consumers (10.9% versus 4.3%, respectively).

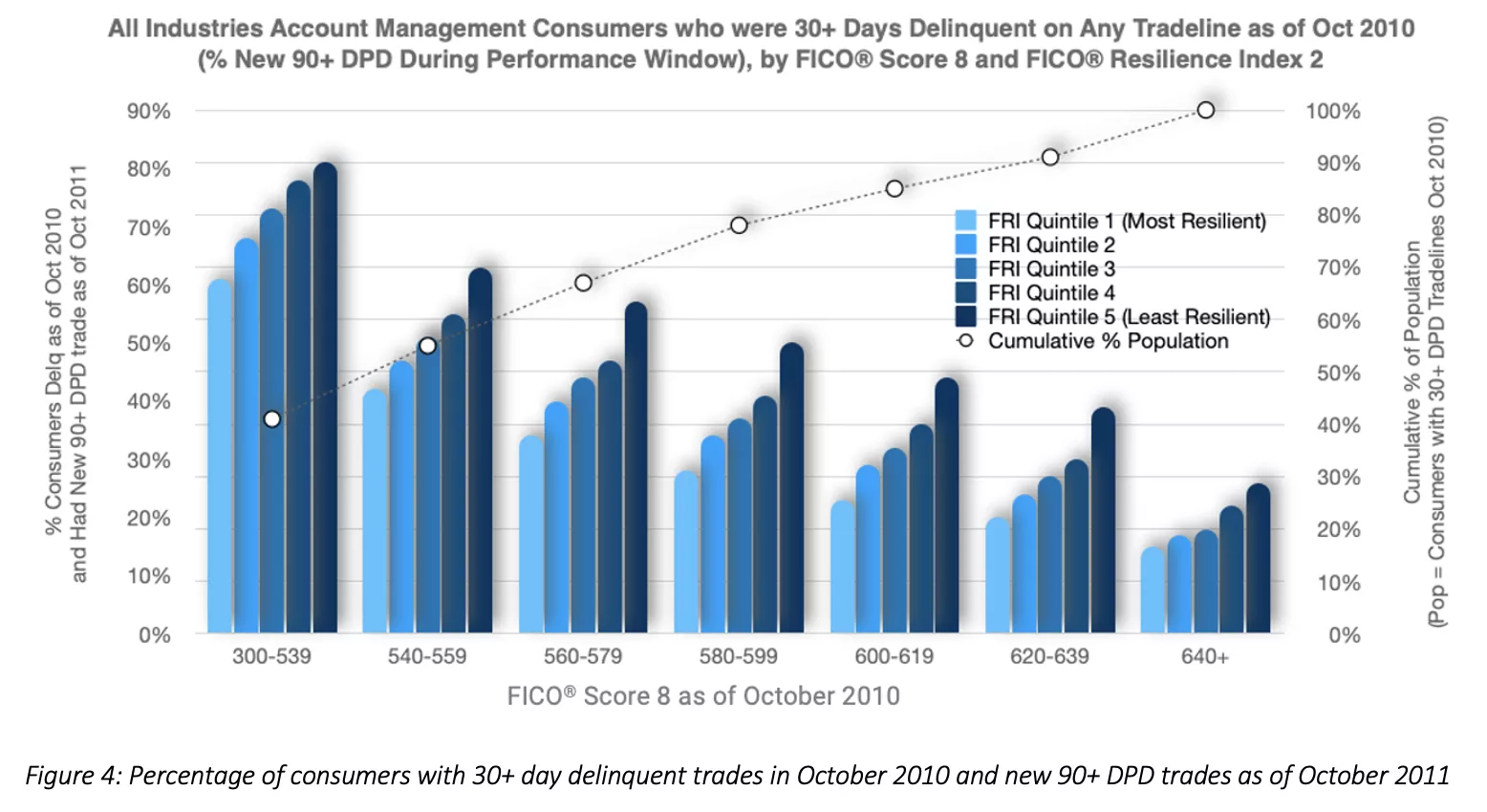

Similarly, we studied the ability of FICO® Resilience Index to rank-order delinquent borrowers’ rate of new defaults in the aftermath of a recession. For this same population of already delinquent borrowers as of October 2010, we analyzed the rate of new 90+ day delinquencies in the following twelve months (Figure 4). Within each FICO® Score band, FICO Resilience Index rank-ordered the risk of new post-recession defaults, which remained elevated despite an improving economy. In the same sub-540 FICO® Score segment, the least resilient consumer segment had default rates 33% higher than the most resilient segment (81% versus 61%, respectively). The rank-ordering was evident across all FICO Score bands.

Summary

Responsible borrowers never intend to enter collections, but some economic situations make delinquency unavoidable. FICO® Resilience Index uncovers hidden risk patterns that allow lenders to manage portfolio risk while simultaneously promoting the best customer collections experience possible, especially in the fragile early stages of an economic recovery. Prioritizing and tailoring treatments of early-stage delinquent customers based on their resilience can thereby lead to more efficient collections and stronger long-term customer relationships.

Please visit the FICO Blog to keep up to date on all of FICO’s latest insights and offerings, including the other three installments of this series, "How to Address Portfolio Risk Volatility Through Economic Uncertainty.”

To gain more background about the FICO® Resilience Index, please visit https://www.fico.com/en/products/fico-resilience-index.

This blog is co-authored with FICO Senior Principal Consultant, David Binder.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.