How COVID-19 Consumer Spend Is Changing Risk Decisions

Transaction Data Changes Inform New Credit Decisions in Australia and New Zealand

COVID-19 consumer spend is changing risk decisions. In Australia and New Zealand (A&NZ) retail credit was already navigating considerable significant, events requiring the attention and resources of the industry. The last five years have delivered a Royal Commission, digitisation, open banking, customer-centric decisioning, and comprehensive credit reporting. However, unlike those events where the industry has had months or years to prepare a response, COVID-19 has necessitated an almost immediate change in focus.

While A&NZ are starting to transition to a more forgiving set of restrictions, globally around a third of the world’s population are still under some form of lockdown, for a largely unknown length of time. Economic indicators such as the price of a barrel of oil (which crashed into negative territory for the first time in history), and US unemployment (around 26M filed for jobless aid in the last five weeks) are not strong.

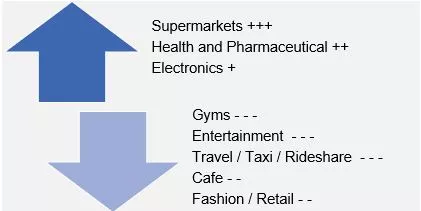

The economic impact of COVID-19 has been felt almost immediately. Variations of “shelter in place” (or lockdown orders) were issued with very little notice. As a result, there has been an abrupt change in consumer spending patterns and these changes have proven to be directionally very similar from country to country and can be generalised in the graphic below;

COVID-19 Consumer Spend Changing Risk Decisions: Australian Data

A scan of the media supports this data;

- CBA reported that supermarket spending on credit cards was up 74 percent based on the same period last year. Other notable changes; 25 percent increase in health services, 7.1 percent fall in transport spending.

- ANZ - 22 percent rise in spending on electronics.

- At an aggregate level, Statistics NZ show that total monthly credit card billings in March fell 9.1 percent to $3.7 billion. This is the largest monthly fall on record and reflects the tight restrictions on movement and commerce in NZ due to C-19. The overall utilisation of available credit limits fell below 30 percent for the first time since mid-2017.

Looking further afield:

- In the USA, there is a similar experience – significant increase in grocery spend, but a sharp decline in entertainment, transport and travel. Citigroup says their card spend fell around 30 percent in the last week of March!

- Brazil, 47 percent of recent survey respondents said they increased their food spending during the pandemic and 45 percent spent more on cleaning products, while another 25 percent bought more health products. On the other hand, 38 percent spent less on sports items. Consumers also reported having decreased their expenditure on other non-essential categories such as office and stationery and beauty and cosmetics.

The removal of spend from the system will have consequences for those industries and some credit issuers have already begun to respond;

- In Australia, there has been an immediate recognition of the difficulties COVID-19 impacted businesses will face. One of the second-tier banks has indicated they will no longer offer mortgages to self-employed individuals involved in at-risk industries such as airlines, tourism, hospitality and retail. Furthermore, casual or contract employees will also fall outside of it’s lending policy, and it will also require proof of receipt of rental income payments to ensure tenants are in fact paying the stated rental.

- Some US issuers have signalled they will begin reducing credit card limits in an effort to limit anticipated bad debt. This practice was common in the US and UK during the GFC, however, it was not as popular in A&NZ during the same period. With the focus on responsible lending, it may something that lenders in the region will revisit.

COVID-19 Consumer Spend Changing Risk Decisions: Operationalizing Transaction Data

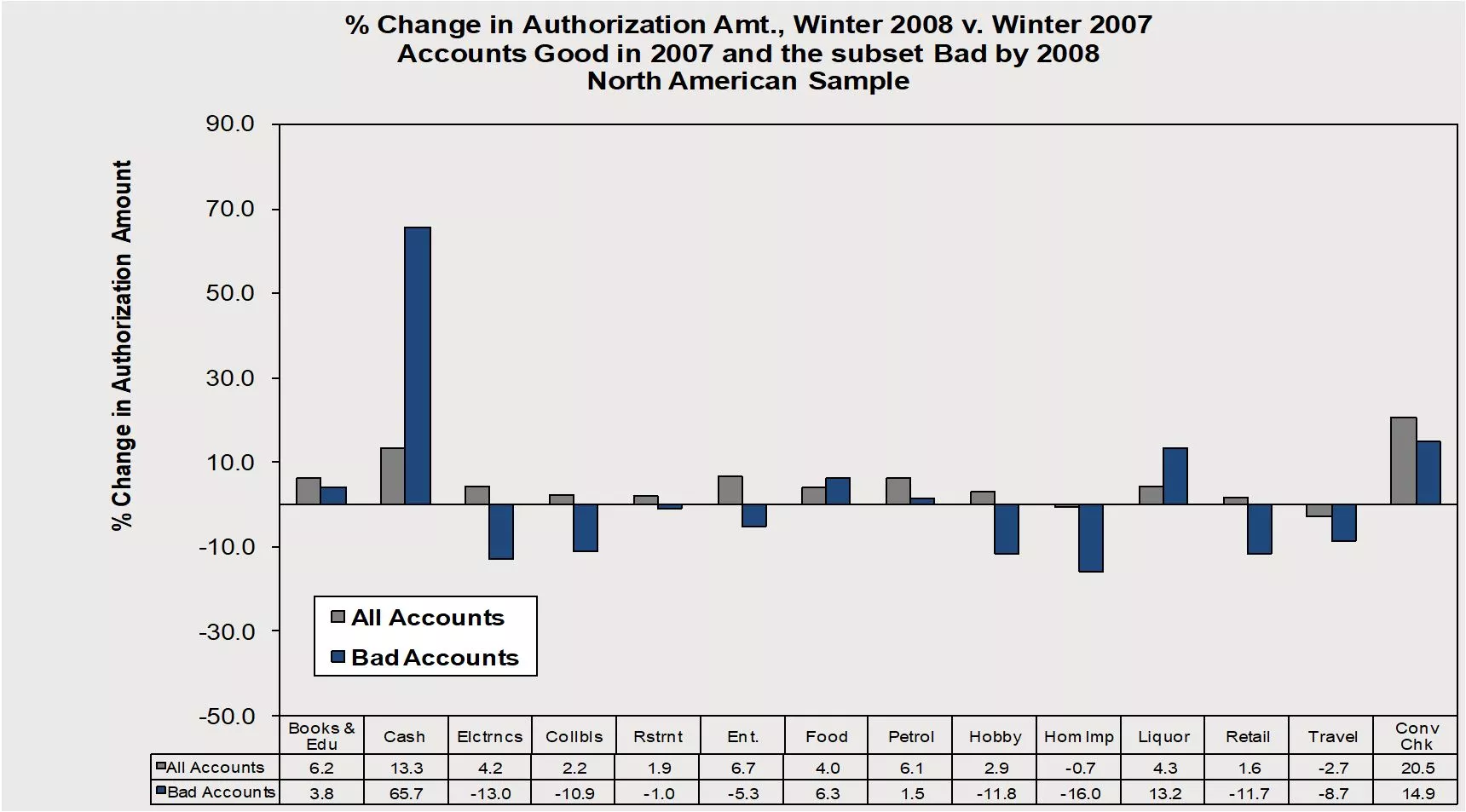

FICO has spent a significant amount of time with clients proving and operationalising value from their transaction data across the credit lifecycle, both here in A&NZ and in other markets. The chart above is an analysis of transaction data from the GFC in the US and shows the changes in spend between the 2007 US winter and winter 2008. The grey series represents all accounts, whereas the blue series is a subset which subsequently moved into late-stage delinquency. Note the positive blue peaks over cash advances, liquor and convenience checks.

COVID-19 Consumer Spend Changing Risk Decisions: Key points to consider

- While a lot of industry focus will rightly be dedicated to approaching delinquent debt, it is worth thinking about what data is being created now that might be useful for you later.

- Transaction information has significant value, both in what is spent, but also what spending is foregone

- Spending patterns will change as customers react to changes in their income, including any stimulus payments

- The prolific nature of transaction data means it is often slow to process, and only stored in full detail for a short period of time

Finally, how might your organisation summarise the transaction data you have access to such that:

(a) you do not lose the signal the data contains, and

(b) it is represented in a format which can be operationalised in your decision systems for customer segmentation and treatment?

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.