How Direct Debits Can Help with Persistent Debt and IFRS 9

The introduction of two initiatives in the UK credit card market may see an increase in the promotion and take-up of Directs Debit, and greater flexibility offered to those paying…

The introduction of IFRS 9 and persistent debt initiatives in the UK credit card market may see an increase in the promotion and take-up of Direct Debits, and greater flexibility offered to those paying this way.

With IFRS 9, issuers will be looking at ways to prevent credit card accounts moving from stage 1, where they must provision for a 12-month expected loss (based on the balance and a proportion of the remaining limit), to stage 2, where this moves to a lifetime losses provision. If issuers are more cautious this could be 100% of the remaining available balance. Stage 2 will occur if an account goes 30 days past due (there may be a mixture within the industry as to whether this means 1 or 2 missed payments), or the level of risk has significantly increased since the account was opened. The latter will be open to interpretation at an individual issuer level.

Although accounts can roll back into stage 1, as this may be a lengthy process it is anticipated that more effort will be placed on trying to prevent accounts’ risk levels increasing, including trying to stop accounts moving into delinquency in the first place. This may be achieved by identifying external risk factors more quickly. The provision will need to be all of the balance plus the percentage of the remaining available credit which the issuer thinks will be a loss over the account lifetime.

In a previous post, I commented on the over £90 billion in unused credit sitting on UK credit cards and the anticipation of limit decreases campaigns on inactive or low-utilised accounts.

The FCA’s recent release in December 2017 containing their definition of persistent debt may also influence the promotion of Direct Debits. Issuers will need to monitor accounts over a 12-36 month period to determine if cardholders are paying more in fees and interest than the principal balance, and if so take specific actions. This may particularly impact cardholders who consistently make late payments due to forgetting to make manual payments (“lazy payers”). Other groups potentially impacted include those on minimum payments with a high interest rate, missed or late payments or fees due to exceeding their card limit and those with a large balance transfer fee and an interest-bearing balance.

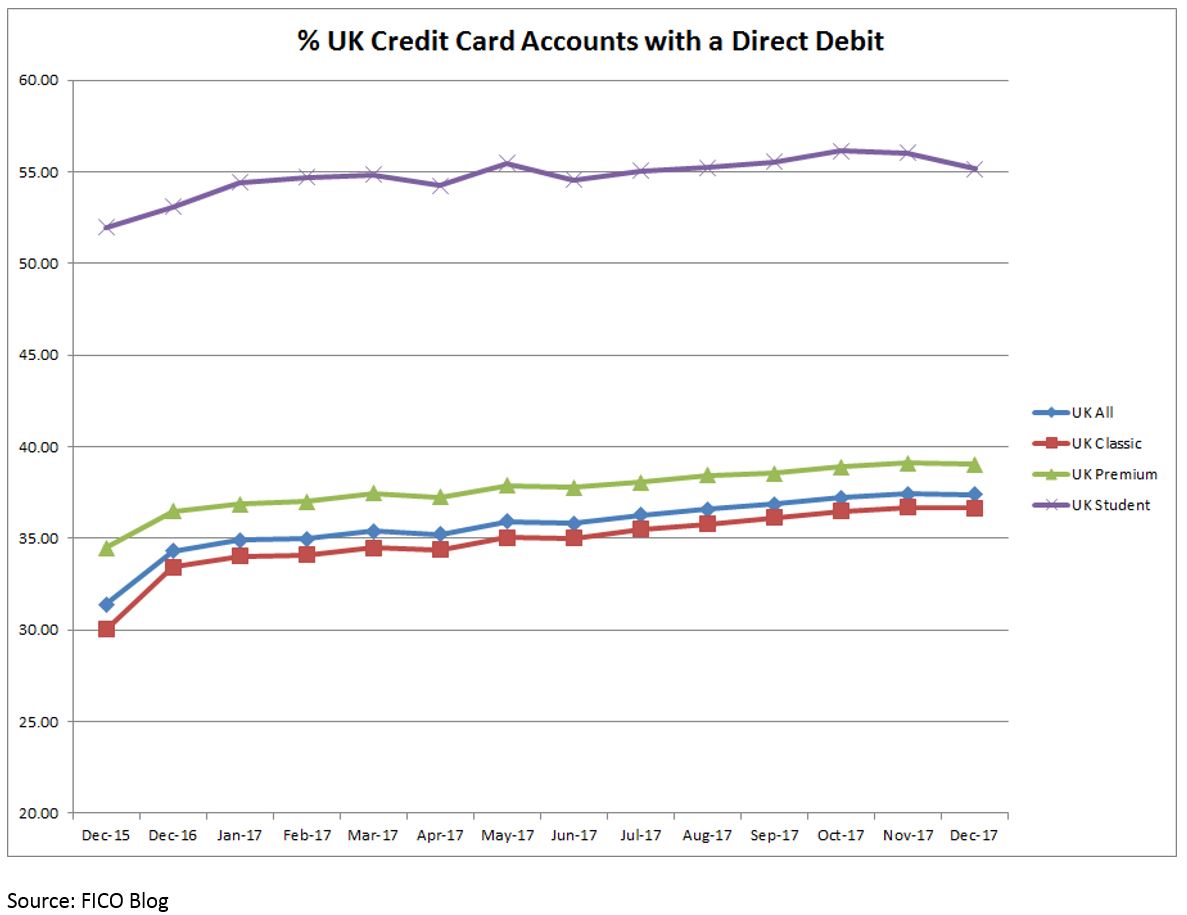

Who Has a Direct Debit?

The December 2017 FICO Risk Benchmarking results show that about 37% of all UK card accounts have a Direct Debit in place. For those <5 years on book, the rate is over 45% and for those 5+ years it drops to 30%. This same pattern can be seen for the Classic and Premium card averages, with only 28% of the Classic population having a Direct Debit set-up to pay their credit card balance, and this is where the highest proportion of accounts report. Student cards have the highest overall percentage (56%), with over 80% of new accounts (<12 months on book) having a Direct Debit. This implies issuers are strongly promoting in this sub population.

FICO looked in more detail at four clients’ data, and accounts without a Direct Debit had a bad rate (bankrupt, charge-off or 3+ cycles in the following 6 months) of between 1.5 to 3 times higher than that of those with a Direct Debit. This takes into account the fact that subsequently the payment could have bounced in the next few months. Whilst this does not mean that all accounts where you set up a Direct Debit will improve payment behavior, it could cover the lazy payers or those who have payment problems. This would be in the cardholders’ interest too, as this would avoid fees and potentially poor credit information being logged at the credit bureaux. This could also help to improve consumers’ credit scores, making future borrowing easier.

There was some evidence that when an account had its statement produced — which influences the payment due date — also impacted bad rates. Issuers could consider a more sophisticated approach to setting the statement date, rather than just linking it to account opening, to ensure it is optimal based on salary date. For existing customers this could form part of a customer service call script. This is a more proactive approach, as currently the majority of issuers rely on the consumer to change the date to suit their circumstances.

Our review also showed that consumers <30 years of age were less likely to have a Direct Debit in place, as they may be more likely to use mobile or internet banking options.

Flexible Direct Debits

After discussions with Bacs, the organisation behind Direct Debit in the UK, it became clear that flexibility in both payment date and frequency can have a significant impact on take-up rates. Offering consumers the option to choose a date, or dates, which suit them best – perhaps to coincide with payday – can have a positive effect. Given the rise of the ‘gig economy’ and the number of people being paid weekly, considering a move away from just a monthly frequency for Direct Debit collection is also worth looking at to encourage more people to opt to pay this way. Find out more about how to promote Direct Debit at www.bacs.co.uk/marketingdirectdebit.

It’s also worth addressing another potential misconception, which is that only minimum or full payments can be taken through Direct Debit. In fact, any % or amount is available — this flexibility could be very useful relating to these two initiatives. Some issuers make it easier than others to change to a more flexible payment structure and this is expected to expand. It would also help with demonstrating to the regulators that customers are being treated fairly.

Increased Direct Debits may result in a loss of revenue for issuers, but this loss may be far outweighed by the cost of provisioning for stage 2 or for the actions required in a persistent debt situation. This trade-off may help issuers build a business case for incentivising Direct Debit usage.

Affordability will have to be taken into account by issuers when determining whether a consumer can increase their monthly payments. Greater use of affordability metrics, including bureau data, is also anticipated.

Issuers could consider

- General Direct Debit education programme

- More visible promotion at originations stage

- Offering multiple Direct Debits in a month if appropriate at the consumer level

- Promoting options for percentages or amounts rather than just minimum or full balance

- Incentivising Direct Debit adoption with preferential offers, such as reduced interest rates or longer balance transfer periods

- Ensuring statement and hence payment due date are aligned to customers’ salary dates

- Targeted campaigns for more mature accounts

- Targeted campaigns based on consumer age

- SMS use for promotions

Organisations interested in finding out more about how offering greater Direct Debit flexibility can drive take-up rates should contact graham.callaghan@bacs.co.uk.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.