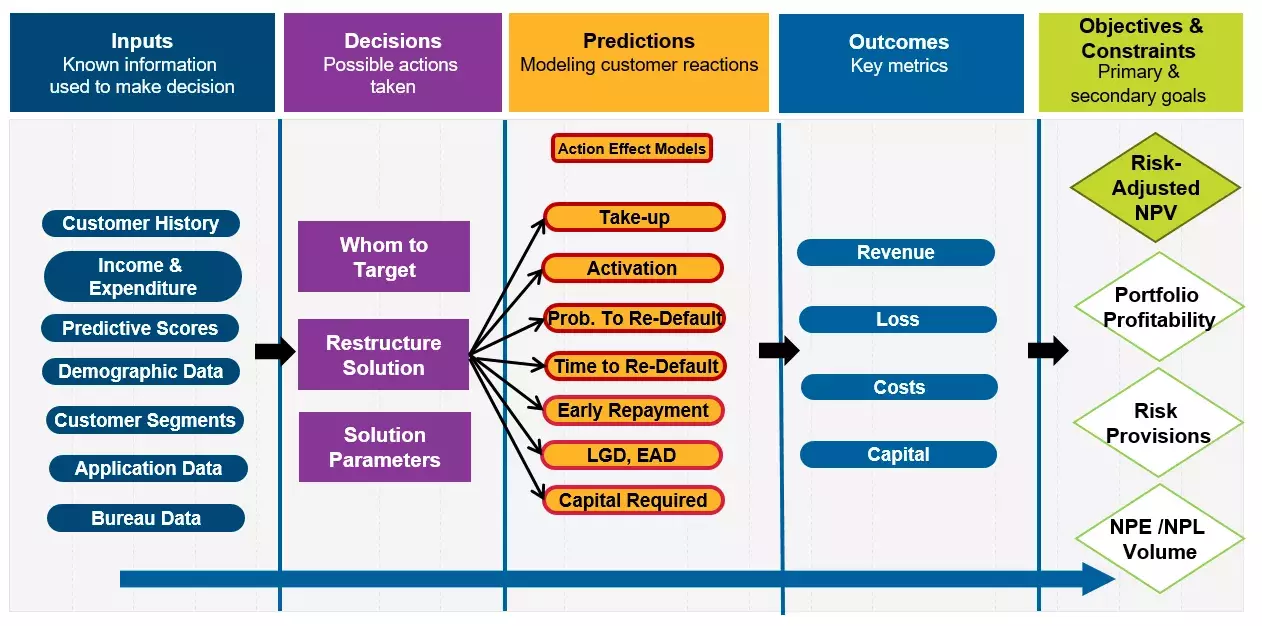

How Loan Restructure Optimization Works

Loan restructure optimization uses mathematical optimization to identify which customers should receive a restructure offer, and which offer should be made. It balances the need to…

Here’s a real-life problem that illustrates the need for loan restructure optimization: I was in a management workshop on collections at an auto finance organization when a receptionist interrupted. “A customer we haven’t spoken to in two years,” she said, “is downstairs. He owes us $100,000. He has $80,000 in a suitcase, and says he can’t pay any more than that. What should we do?”

It’s a great story, the kind you just couldn’t make up. Now ask yourself: Would your organization take the money?

Silly question — of course you should take the money (subject to money laundering checks!). If you go back downstairs and turn down the cash, that customer isn’t coming back with a bigger suitcase.

However, a lot of organizations have policies that would say otherwise. That’s why loan restructure optimization is so important. You need to be able to take the money the customer can offer rather than policy for not compromising and end up with nothing or much less. Restructures are meant to balance the needs of the two parties — and optimization is the analytic science of balancing.

What Is Loan Restructure Optimization?

Loan restructure (also known as Modification of Credit Terms in some markets) optimization uses mathematical optimization to identify which customers should receive a restructure offer, and which offer should be made. It balances the need to increase loan Net Present Value with take-up probability and re-default rates. Because it can balance multiple objectives and constraints, it’s better than simplistic restructure campaigns based on a couple of polices, and avoids high re-default rates caused by judgemental selection of the right restructure solution.

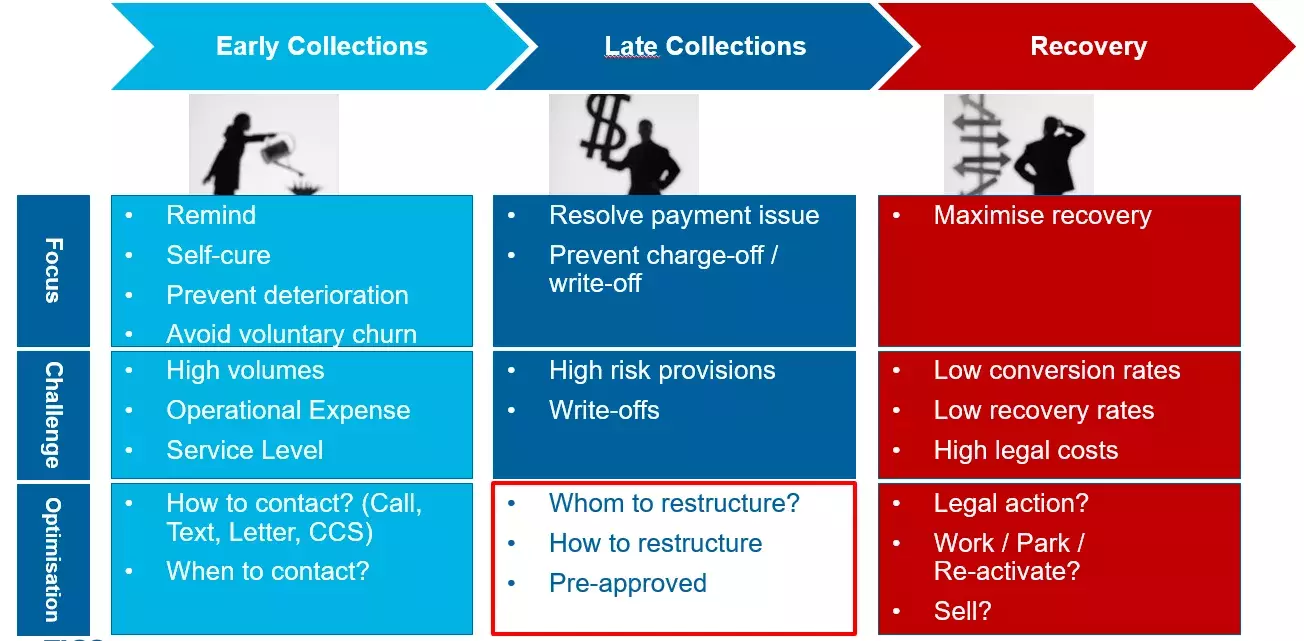

Debt Collection and Recovery Lifecycle

Optimization can be applied throughout the collections process, but the questions you ask are different. By the time you are in late collections, the question is less about who is high risk (everybody is) or whom you should talk to (no one is going to self-cure) than about how you can reach a compromise that resolves the issue.

Some customers are in financial difficulties due to lifetime events like health, divorce and unemployment. Some of these are temporary deteriorations of their financial situation, and some are permanent.

You can insist on the customer fulfilling the contract, and allow their debt to go to recoveries, but this is typically not the best decision for you or the customer. It is also a disincentive for the customer — most people would rather pay the accounts where they might still have a service when the payments are made. It’s in both sides’ interest to find a solution that is sustainable for the customer, and takes the money the customer can provide.

In order to do effective restructuring you need to do two things, and these can be solved with debt restructure optimization:

1. Pick the right person to contact, and understand their income and expenditure situation, so you know what they are able to pay. To pick the right restructure option, you need to go through the customer’s income and expenditure, and this is an expensive conversation. The whole cycle might be $50-100 of operational cost. You don’t want to do that with a customer you don’t need to restructure, or one for whom the restructure won’t succeed. Out of, say, 50,000 accounts in buckets 2-4, you want to pick the 2,000 you want to talk to. Analytic optimization can find the right customers, and it does so in part by weighing the impact a restructure can make on the Net Present Value of the loan, and the likelihood that the customer will respond to an offer.

2. Pick the best options for the customer given their circumstances. Optimization can respond to the customer’s income, spend, outstanding debt and other circumstances to find the right restructure plan. This includes whether you need to offer temporary or permanent reliefs, whether there should be step-ups, whether you should compromise on interest or capital and by how much, and other variables.

Optimization helps collections staff to pick the right tool. It provides a decision tree that removes the decision of what tool is best based on income, spend, current balance, current plan, etc., and says how the new payment plan should be restructured. The result helps the creditor with the NPV of the account, and helps the customer.

How to Configure a Debt Restructure Optimization Solution

Why Use Optimization?

What we see in many markets is that the selection of restructure tool is driven by a mix of policy and collector gut feeling, many organisations use spreadsheet calculators that apply basic rule sets. In markets with high delinquency rates, collectors tend to over-restructure, or to restructure using plans that don’t solve the problem, they just kick it down the road. This causes high restructure default rates — you might see 50% after 6 months, or 80% after 12 months. In these cases, you’ve removed the account from collection portfolio, but it will be back. The customer is blamed for the repeated defaults, when in fact it’s the problem with the solution.

You want a solution that fixes the problem permanently. It won’t be perfect — you might see a 15-20% restructure default rate — but it will deliver substantial uplift over a restructure strategy that is judgementally derived. Now more than ever, in an IFRS 9 world, the performance of restructures will determine the lifetime provision that will need to be retained on these customers. Default rates that are higher than they could be will cost more in provision and NPV than what is being recovered short-term in cash.

Optimization can solve for this. It helps you get past unhelpful policies and gut reactions, and it will also make the financial impact of policy constraints transparent.

Best Practices

Here are three best practices for adopting and deploying loan restructure optimization.

- Execution. You need to know not only what the best offer is, but the best way to put it in front of the customer. That means having a good decision engine that supports the collector, helping them convince the customer to take up the offer.

- Simplicity. Keep the paperwork simple. Ideally, the customer can accept it immediately, rather than being required to come three times to a branch, or sign a 30-page agreement at seven places — this sounds unrealistic but actually happens. If you make it too hard, the customer thinks they are signing away their soul or gives up. The quicker the process is, the fewer touchpoints, the lower the number of times the customer needs to walk somewhere, the more likely the customer will take up the offer.

- Measurement. Measure things like restructured accounts rolling back to 30 days past due, the operational impacts from campaign to closure, and where in the process you are losing customers, so you can address operational hurdles.

You may be wondering: So did that auto finance firm take the customer’s $80,000? Yes — but only because there was a C-level exec in the room who could make the call. That’s why loan restructure optimization is so important — so you don’t need C-suite approval when a customer comes with a reasonable offer.

Want help? Our Fair Isaac Advisors team has the experience necessary. Give us a call.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.