Who Defaults when Bankcard Accommodations End? Resilience Matters

New perspective on borrowers rolling off bankcard payment accommodations.

With non-mortgage write-off rates at the lowest YTD level seen since 2012[1], it’s easy to forget that the pandemic has, in fact, stressed many borrowers. In contrast to mortgage forbearances of six to 12 months, bankcard payment accommodations are typically just one to two months, with card lenders less likely to readily grant repeated accommodations. Is the recent uptick in bankcard write-off rates[2] a warning sign as many accommodations programs draw to a close?

In a quest to understand how borrowers exiting bankcard payment accommodations are performing, FICO researchers asked, “Does borrower resilience (as identified by FICO® Resilience Index) play a factor in how they weather the economic stress that led them to enter into payment accommodations once the accommodation has ended?” FICO Resilience Index –released by FICO in early 2020 - is designed to predict consumers’ sensitivity to economic disruptions.

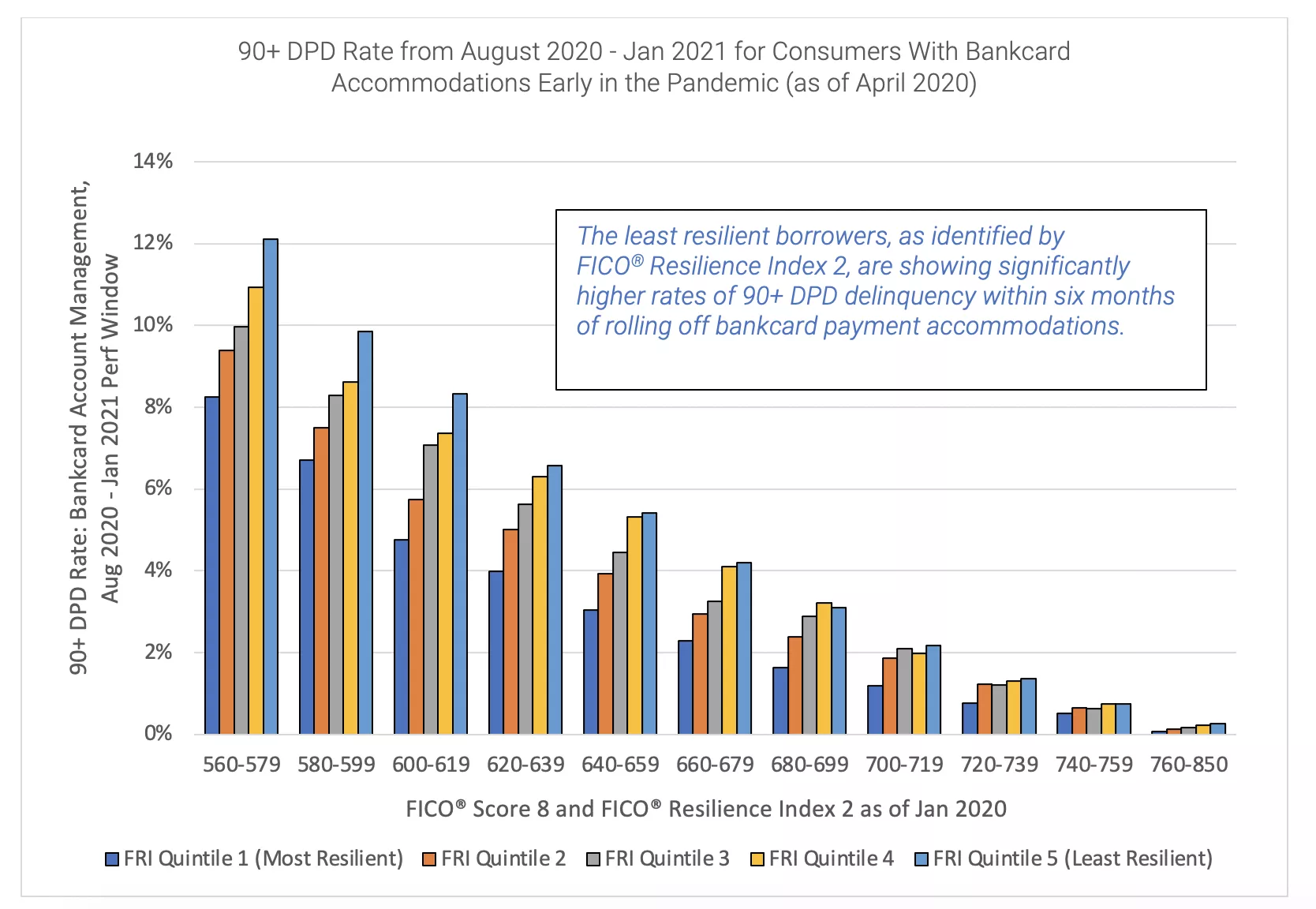

We analyzed borrowers who entered some form of bankcard payment accommodations early in the pandemic (as of April 2020) and had “rolled off” those accommodations by July 2020. We then observed their payment performance on bankcard accounts over the next six months – an unusually short window – to look for early clues into how their repayment behavior related to their level of resilience (measured by their FICO® Resilience Index 2 value as of January 2020, before the pandemic).

We found that particularly for subprime and near-prime cardholders, their repayment performance is strongly related to their resilience. In the FICO® Score band of 600-619, for example, the least resilient 20% of cardholders rolling off bankcard accommodations had a 73% higher rate of 90+ Days Past Due delinquency than the most resilient quintile in the same FICO Score band. Over a longer performance window, we expect the differentiation in repayment rates by FICO® Resilience Index will become even more pronounced.

While the pandemic-driven economic crisis is receding and lenders are charting a path to grow bankcard receivables, it’s worthwhile to consider a borrower’s FICO® Resilience Index – now available alongside the FICO® Score – in payment accommodation decisions going forward, as well as in the extension of additional credit in the form of credit line increases. Less resilient borrowers may need additional time to recover from pandemic-related economic stress before their repayment performance stabilizes. Conversely, more resilient borrowers are more likely to be ready to take on additional credit.

With the availability of FICO® Resilience Index 2 this summer – featuring significant improvement in assessing borrower resilience across different credit products - now is an excellent time for lenders to pair FICO Resilience Index with the FICO® Score in their risk decisioning processes.

To learn more about building for resilience across the consumer credit lifecycle, check out this blog series.

[1] Equifax report: “U.S. National Consumer Credit Trends Report: Portfolio, Data as of May 2021”, p. 10. equifax.com/resources/monthly-national-consumer-credit-report-june-2021-portfolio/

[2] Ibid., 37.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read more

Average U.S. FICO Score at 717 as More Consumers Face Financial Headwinds

Outlier or Start of a New Credit Score Trend?

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.