Machine Learning for AML Gives Pros “Superhuman” Powers

Uncovering hidden patterns in money movement makes machine learning for AML a very attractive enhancement to existing AML operations.

Many anti-money laundering (AML) operations work hard to show that they are in compliance with rules and regulations, and struggle to maintain appropriate staff levels to work all the alerts. Despite all this effort, global money laundering is out of control; the annual amount of money laundered is estimated at about 2-5% of global domestic gross product (GDP). High false positives and inefficient processes are one reason that the vast majority of money laundering is going unstopped.

Machine learning for AML is dramatically improving the efficacy of compliance operations, today. I recently spoke on this topic to an enthusiastic audience at the Association of Certified Anti-Money Laundering [AML] Specialists (ACAMS) 18th Annual AML & Financial Crime Conference in Las Vegas. With the energy of Vegas providing an appropriate backdrop, we talked about:

How Machine Learning Is Different from Artificial Intelligence (AI)

As summarized in the graphic above, machine learning does not perform humanistic programmed cognitive tasks. Rather, machine learning algorithms learn novel new relationships from data. Uncovering hidden patterns in money movement makes machine learning for AML a very attractive enhancement to existing AML operations.

Using Machine Learning to Prioritize Alerts and Find More Money Laundering

In my presentation I referenced a 2017 article by McKinsey on the topic of applying new technologies to AML. With 99% of alerts turning out to be false positives, McKinsey noted that machine learning techniques reduce false positives 20-30%. In turn, investigators’ workload can be reduced by 50%.

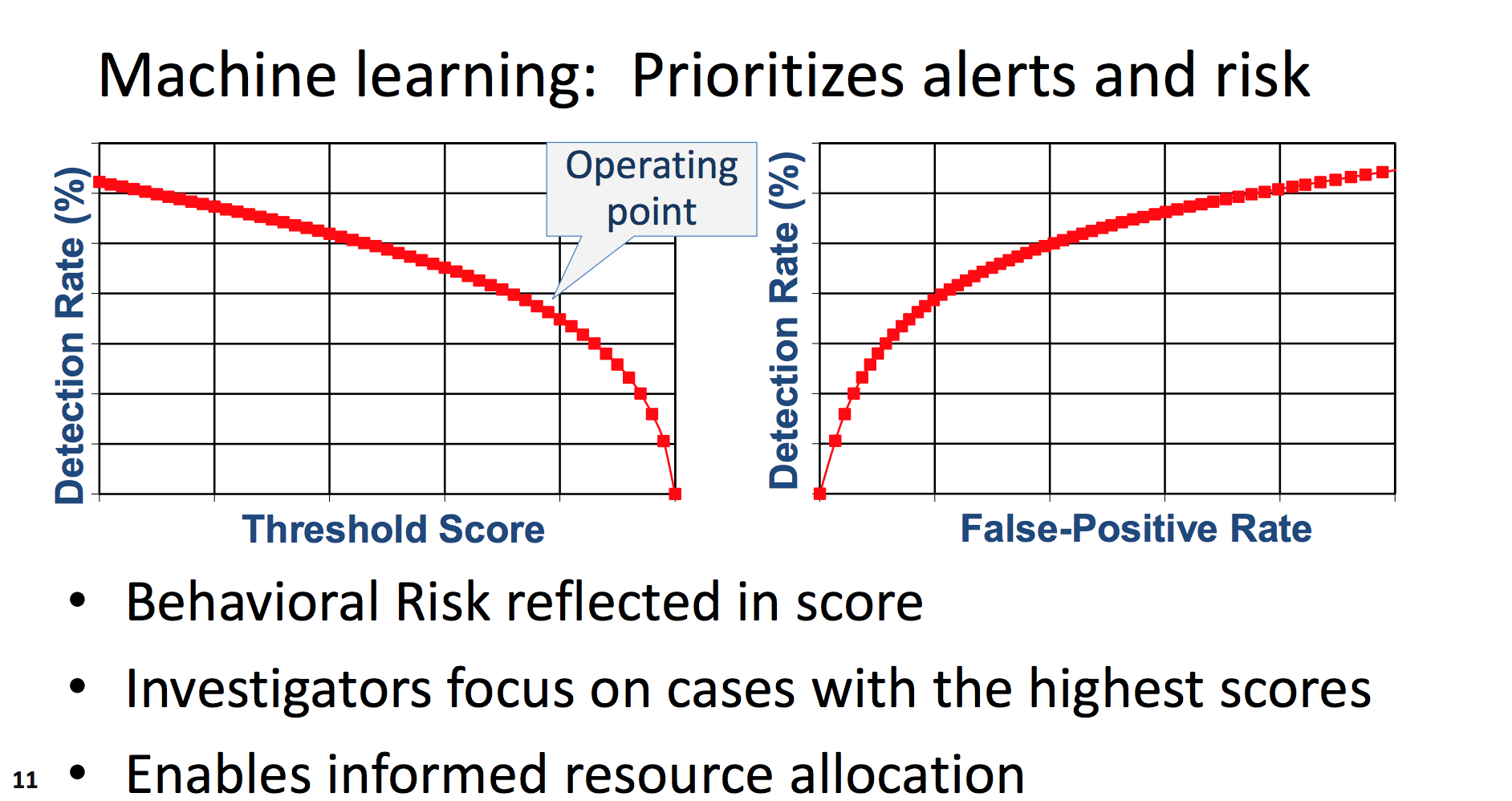

The plot below illustrates how organizations typically use machine learning scores. By choosing a score threshold, an AML professional can understand the amount of money laundering detected and consequently control the false positive rate. The AML professional therefore chooses one or more thresholds triggering analysts to work cases. Transactions may also be auto-actioned.

Challenging Know Your Customer (KYC) Practices Using Real-Time Behavioral Analytics

Machine learning for AML can drive a 3x improvement in alarm-to-suspicious activity report (SAR) conversion rate through tighter segmentation, according to McKinsey. Examples of finer segmentation include learning that a customer has financial relationships outside of the US, is a high net worth individual, or is a small business owner. In this way, machine learning challenges the status quo of KYC processes using real-time behavioral analytics based on financial transaction activity.

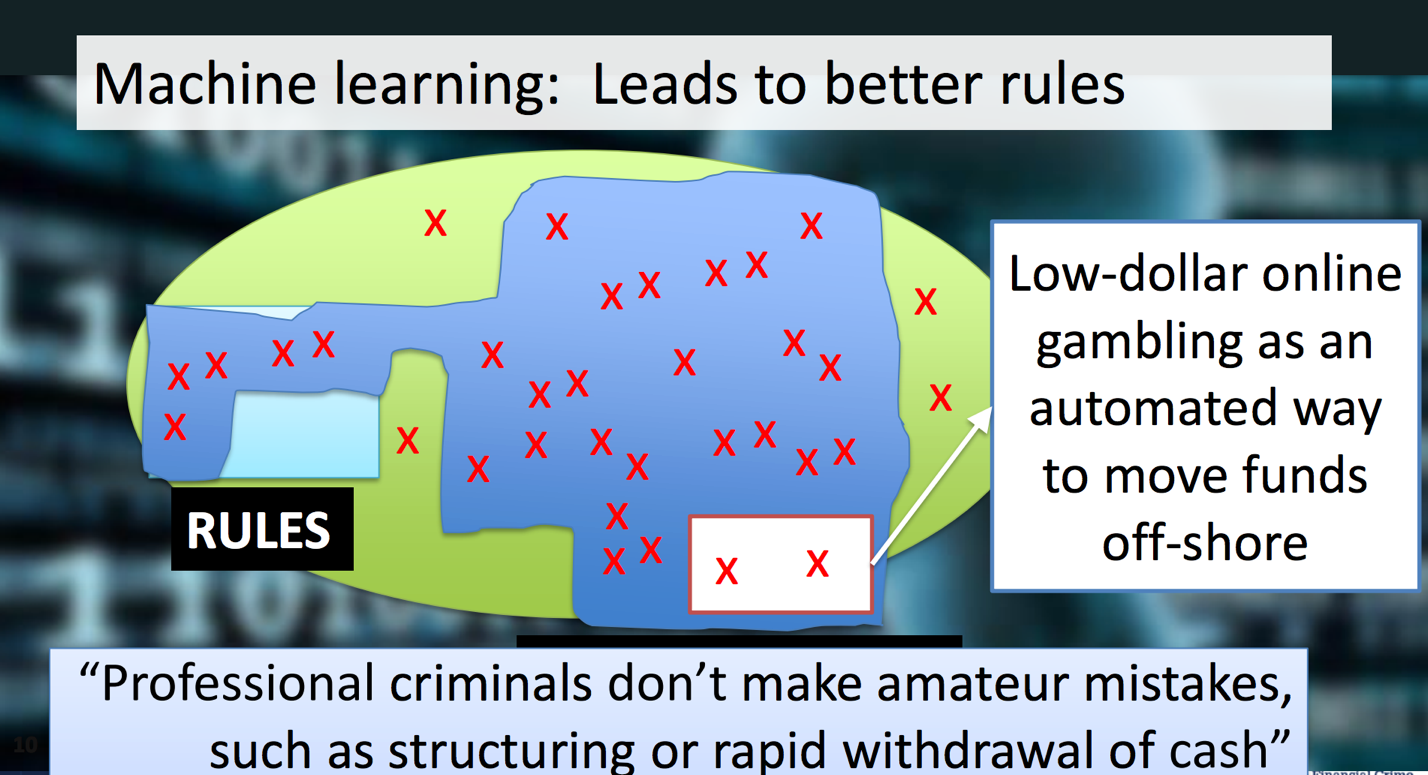

Machine learning can even lead to better rules, as illustrated in the figure below. For example, the machine learning model may find customers who make low-dollar online gambling transactions are doing so as a way to move funds off-shore. By understanding that machine learning algorithms detect new unseen patterns that reveal illicit activity (but rules don’t allow for), new and better rules and insight can be derived.

How Machine Learning Models Are Made Explainable

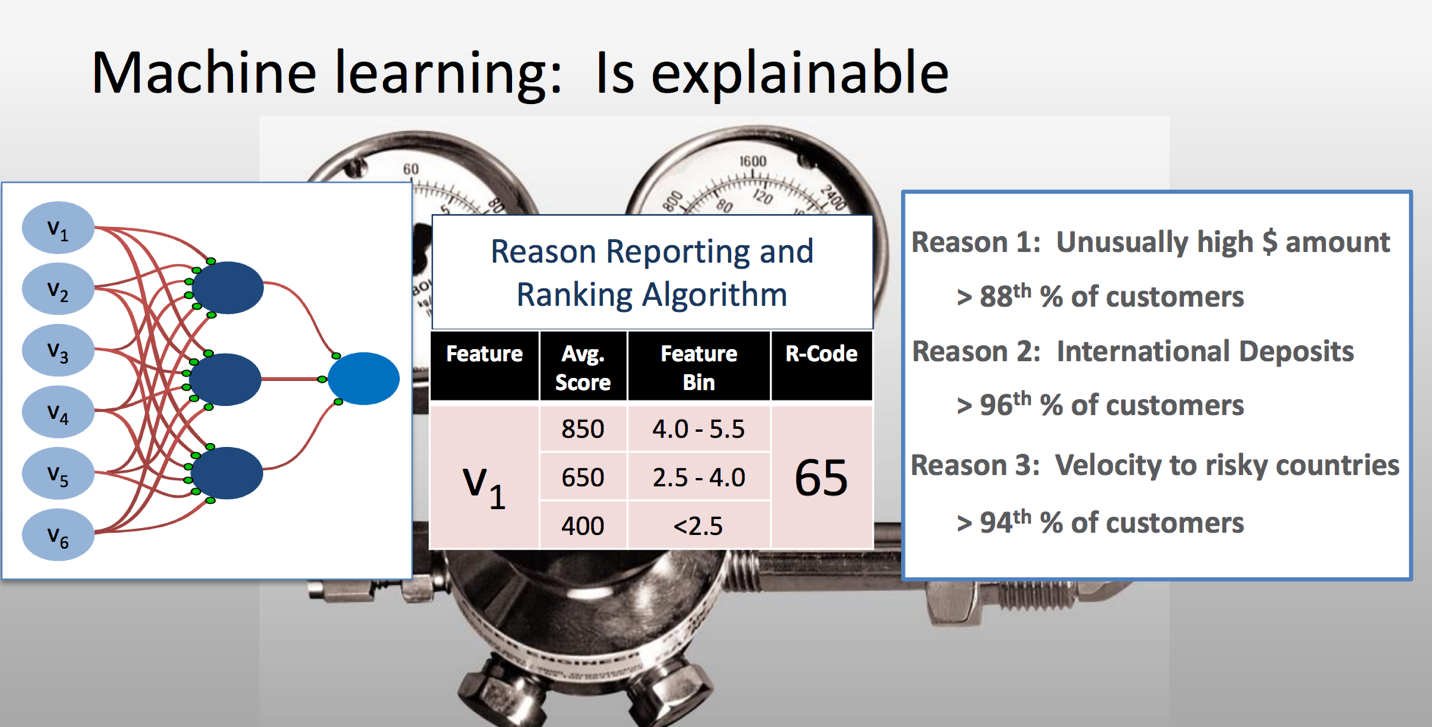

In addition to using machine learning, I described how these machine learning models are made explainable to investigators, regulators and internal governance teams. The example below shows how the multiple variables comprising the model (V1-V6 at far left) each feed into machine learning algorithms, the results of which are processed by a Reason Reporting and Ranking Algorithm. The reasons are ranked in terms of importance and relevance in explaining how the model arrived at the score.

This algorithm has been used in the FICO® Falcon® Platform for years, and speaks to the likelihood that value of a variable (and consequently the reason code) would contribute to the observed score. This is based on the totality of data used to construct the machine learning model and is probabilistic. By ranking the top reason codes, analysts and regulators will understand how the score was derived, which can aid in investigations and creating narratives of the SAR.

In sum, machine learning for AML can help with key compliance challenges like false positives, gaining new insight and understanding of customer behavior, and providing decision logic that is clear and explainable. Clearly, machine learning technology adds a “superhuman” boost to the efficacy of AML efforts!

For more information, read our Artificial Intelligence in AML and KYC: Enhancing Accuracy and Reducing Costs Hot Topic Q&A.

To learn more about how I help FICO develop technology to fight financial crime, follow me on Twitter @ScottZoldi.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.