Merchant Acquiring: The Fraud Landscape for Competitive Advantage

As merchant acquiring models evolve, fraud management must expand beyond traditional transaction monitoring toward a broader view of ecosystem governance

Why Is Fraud Management the New Battleground for Merchant Acquiring Success?

As payment fraud is both growing in scale and sophistication – where over 23 million transactions were compromised last year, what was once viewed as a necessary operational cost has now evolved into a strategic differentiator. With sophisticated e-commerce merchants increasingly evaluating acquirers on fraud performance metrics during their merchant acquiring selection process, merchants started focusing on false positive rates and chargeback handling capabilities. This represents a fundamental market evolution: fraud management excellence has become the primary differentiator for winning high-value merchant relationships and commanding premium pricing.

This shift is being driven by the rapid growth of card-not-present transactions, where fraud risk is inherently higher. At the same time, first-party fraud and policy abuse — the fastest-growing and hardest-to-detect categories — demand behavioral analysis over time rather than point-in-time transaction screening, raising the bar for what acquirers must deliver.

In merchant acquiring, fraud extends beyond the familiar pattern of a cardholder disputing a stolen credit card or an unauthorised purchase. It is a multidimensional risk that can emerge at multiple points within the payment ecosystem — between the customer and the merchant, the merchant and the acquirer, or within the broader infrastructure that connects them. Modern acquiring environments involve complex networks of merchants, payment facilitators, marketplaces, gateways, processors, and technology infrastructure. As acquiring models evolve, fraud management must expand beyond traditional transaction monitoring toward a broader view of ecosystem governance.

Sources:

Chargeback / CNP Dispute: https://www.mastercard.com/gb/en/news-and-trends/Insights/2025/2025-global-chargebacks-outlook.html

Acquirer Liabilities Rising

The financial imperatives are clear: acquirers bear ultimate liability for merchant defaults and chargebacks when merchants can't absorb losses. Under payment system rules, merchants are responsible for absorbing fraud-related losses, and managing this effectively is part of what keeps them in good standing with their acquirer. But when a merchant is unable to absorb those losses — whether due to insolvency, high chargeback volumes, or outright fraud — the liability shifts to the acquirer. This is why acquirers are so motivated to properly vet merchants and monitor their ongoing activity. They are ultimately the ones on the hook when things go wrong.

In July 2026, Mastercard will update its rules and request acquirers to investigate any flagged merchant within 72 hours — if more than 5% of their purchase transactions result in refunds or chargebacks combined during any 30-day rolling period, their acquirer will need to investigate the merchant.

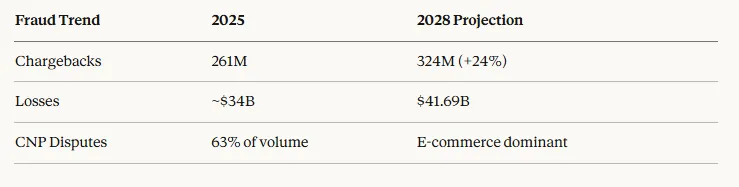

Global chargeback volumes are estimated to increase by 24% from 261 million in 2025 to 324 million by 2028, and the associated losses reaching $41.69 billion, and with average chargeback values ranging from $69 for subscription services to $120 for travel and hospitality merchants. Though this value presents a challenge, it also can be turned into an extraordinary opportunity: while competitors struggle with reactive fraud management, forward-thinking acquirers are transforming their fraud capabilities into state-of-the-art engines that drive merchant acquisition, retention, and growing portfolio.

Three Strategic Imperatives for Fraud-Driven Market Leadership

1. Advanced Onboarding & Underwriting Excellence: Your First Competitive Advantage

Merchant onboarding represents the highest-leverage opportunity in the acquiring lifecycle, which requires application intake, underwriting, and pricing and where early fraud detection prevents costly losses while accelerating time-to-revenue. Onboarding is one of the highest-risk moments in the merchant relationship, where early mistakes are costly downstream. Leading acquirers are implementing sophisticated risk assessment methods, such as automated digital KYC, real-time screening, and advanced risk modelling, to identify potential fraud risks before they enter the portfolio. These methods transform onboarding from a cost centre into a competitive weapon.

Case Study Impact: In a previous client engagement, FICO Platform capabilities reduced manual merchant onboarding timelines from up to nine days to just minutes, while implementing advanced fraud detection that prevented high-risk merchants from entering their portfolio. This transformation enabled the acquirer to compete effectively against fintech disruptors while maintaining superior risk controls.

Strategic Implementation: Deploy AI-driven identity verification systems that leverage multiple data sources to identify synthetic fraud and merchant misrepresentation during the application process. FICO Platform allows users to segment merchant risk profiles automatically, enabling differentiated onboarding workflows that balance speed with appropriate due diligence levels, preventing fraudulent merchants from ever reaching the transaction processing stage.

2. Predictive Merchant Monitoring for Early Intervention

Modern merchant monitoring demands a comprehensive risk assessment across the entire merchant lifecycle. Acquirers need cutting-edge technology that provides integrated customer interaction history, proactive maintenance strategies, and AML portfolio monitoring with a focus on early identification of volume variations, margin deviations, and financial risk indicators. Beyond transaction monitoring, fraud exposure extends across structural layers of the acquiring ecosystem — including payment routing, settlement flows, and intermediary platforms — requiring a portfolio-wide view to detect hidden fraud conditions early.

Behavioral Pattern Recognition: Advanced monitoring platforms track merchant lifecycle indicators, transaction velocity changes, and comparative performance metrics against similar merchant cohorts. This enables early identification of merchants at risk of excessive chargebacks, financial distress, or policy violations — allowing proactive intervention before problems escalate.

Case Study Impact: Acquirers implementing comprehensive merchant monitoring report significant improvements in fraud performance metrics, false positive rates, and chargeback volumes. These platforms enable precise merchant segmentation by MCC codes, sales volume, and risk indicators, allowing for pricing and risk management strategies that improve overall merchant profitability.

3. Integrated Transaction-Level Controls & Governance: Operational Excellence as Competitive Advantage

Transaction-level fraud management must seamlessly integrate with comprehensive governance frameworks to create operational advantages that competitors cannot replicate. Operational efficiency becomes a critical competitive differentiator in merchant acquisition and retention.

Comprehensive Dispute Management: The most effective acquirers implement automated dispute prevention tools that can prevent incoming chargeback cases through real-time merchant notifications. Platforms enable merchants to issue proactive refunds, avoiding costly chargeback processes while maintaining customer satisfaction and merchant relationships without attrition. Merchant monitoring should distinguish between fraud victims and complicit merchants, where monitoring detects both situations, and governance handles the distinct dispute dynamics of each.

Regulatory Compliance Excellence: Advanced acquirers implement governance frameworks to ensure consistent compliance across their merchant portfolios while minimising false positives that could damage merchant relationships or operational efficiency, while supporting the merchant during the dispute process.

The Competitive Imperative

Merchant acquiring success now demands precision execution across fraud management, predictive analytics, and comprehensive portfolio governance. Acquirers that deploy these fraud-centric strategies — supported by advanced analytics and automated decision-making — present higher chances to be ahead of competitors in an increasingly competitive landscape, avoiding merchant attrition and protecting acquirer profitability.

Organisations that transform their fraud management through strategic technology investment will capture outsized returns while protecting their merchant portfolios from increasing fraud losses. Competitive advantage depends on how quickly institutions can implement fraud management strategies to secure both current market share and future growth opportunities.

How FICO Can Supercharge Your Acquiring Business

- Read Why Merchant Acquirers Need Digital Decisioning Platforms

- Read our paper Transforming Merchant Acquiring with FICO

- Discover our approach to merchant acquiring

- Read our executive brief Merchant Onboarding & Originations on FICO® Platform

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.