Peering Over The Edge Of The Financial Cliff

Australian banks examine options on mortgages and business lending to bridge a looming financial cliff

Financial Cliff: Desperate Times

The hopes of a fairly speedy return to a ‘Covid-normal’ in Australia have been dashed as Victoria has entered a second wave of infections. There is further evidence overseas that future spikes will continue to occur as countries attempt to relax restrictions. This all points to the likelihood of a protracted period of economic uncertainty as governments act to contain outbreaks when, and where, they appear. Meanwhile, time marches on and we approach a potential financial cliff.

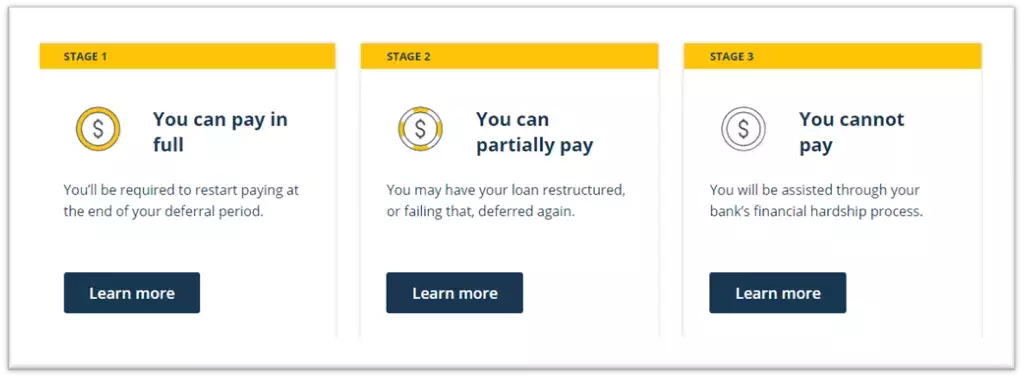

The six month pause on payments instituted by Australian Banks was certainly not designed to accommodate the situation we now find ourselves in. Further assistance was announced in July offering customers a further four month deferral or the option to restructure their loan. Banks have begun to scrutinise any ongoing need for assistance however the president of the Australian Banking Association (ABA) has suggested that at least half of all the mortgage customer currently deferring their payments will require additional assistance, nearly 250,000 customers. The ABA has articulated a three-phased approach supporting customers through Covid-19

Source: https://www.ausbanking.org.au/covid-19/

Currently, banks are moving to phase 2 where their customers’ individual circumstances are discussed at length and an assessment is made on the need for ongoing support. At the beginning of the lockdowns a former colleague described the problem facing financial institutions as a ‘portfolio of good quality customers facing a temporary shock to their income, all they need is a bit of immediate assistance’.

Payment deferrals make perfect sense under these circumstances and align with the typical measures that are offered when customers apply for hardship assistance in Australia. However, these same measures have also created the concern about the financial cliff facing the industry now and it is possible that offering further payment deferrals risks kicking the can further down the road.

Once the holiday is over customers will face an increase in their repayments to cover capitalised interest and an accelerated amortization schedule to meet the contracted terms of their loan. In a situation where the road to recovery is paved with false starts many bank customers could find themselves paying substantially more a month than before the pandemic. Is this the time for the banks to rethink hardship or forbearance policies?

Financial Cliff: More Problems to Come

In the wake of the Global Financial Crisis, lenders in several markets were presented with an almost unprecedented increase in bad debts accompanied by a sharp drop in property prices. Currently, policies in place in Australia are helping to prevent increasing bad debts and the property market has only seen a small drop.

The Australian Prudential Regulation Authority (APRA) has signed off on an extension to loan deferrals until March 2021 effectively staving off any major increase in arrears or impairment for the time being but at least one CEO of a big four bank has described the need to assess the long-term prospects of individual loans seeking assistance. This also has implications for the property market. As assistance is removed, it is quite likely that property prices will decline further as banks and their customers start to address loan impairment.

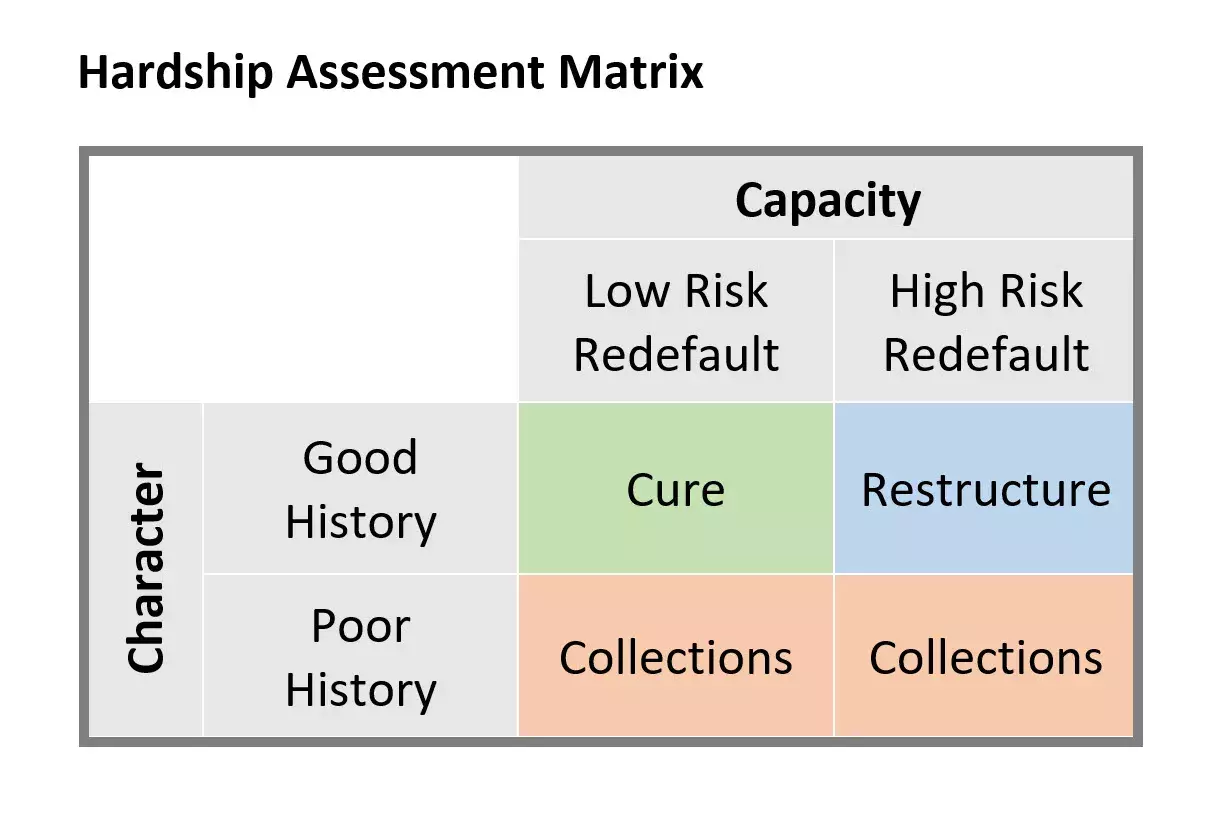

If we think about the three Cs of credit; Capacity, Character and Collateral we currently face a real risk to capacity and collateral.With so much assistance provided to Australians through their banks and the government, it is very difficult to determine their credit worthiness or character. The propensity of a customer to default, or redefault, once they resume repayments is currently driven by their financial capacity. For customers facing higher repayments at the end of their deferral period than previously, the current assistance measures could exacerbate the issues in time.

The challenge facing banks is how to distinguish between the customers that have the ability to resume paying their loans (cure), the customers that could resume paying if their debt was restructured and the customers that should enter collections.

For customers with an extensive payment history, banks have a means to assess their customers’ historic performance. Customers with a poor history of delinquency are likely to continue this behaviour once assistance is removed. Capacity to service a loan can either be assessed though analysis of customers’ transactional data or by having a conversation about their financial position.

For customers with an extensive payment history, banks have a means to assess their customers’ historic performance. Customers with a poor history of delinquency are likely to continue this behaviour once assistance is removed. Capacity to service a loan can either be assessed though analysis of customers’ transactional data or by having a conversation about their financial position.

Financial Cliff: Rethinking Hardship

Following the GFC the Obama administration established the Home Affordable Modification Program (HAMP). This program was set up to help lenders establish loan modification criteria and provide terms that would allow customers to continue to service their debt. The program used a principle of ‘positive present value’ to establish whether a loan modification was suitable for a given loan. One key takeaway from this exercise was that modifying the loan terms was often mutually beneficial to both the lender and customer when considered as an alternative to foreclosure or charge off. Existing market structures and established practices were preventing its implementation prior to the establishment of HAMP. While this was aimed at the US mortgage market, the framework has been extended to other types of debt in various markets and FICO has assisted customers in a variety of markets and settings.

An essential consideration under the assessment criteria is a customer’s likelihood to default (or redefault). This assessment is made using a serviceability metric such as the debt to income (DTI) ratio. A loan modification that improves a customer’s DTI, reduces their likelihood of defaulting when their serviceability (capacity) is the major reason for hardship. The present value of the modified loan, with reduced risk, is considered against a scenario where the loan remains on its current terms, at a higher risk of default. Using this framework, a bank can consider the costs of measures such as fee or interest waivers against the costs of foreclosure and charge off, along with any potential shortfall. When we think about a customer’s serviceability as a key risk lever, not all assistance offered is equal and a more nuanced approach is possible, one that can be better tailored to the circumstances of each customer.

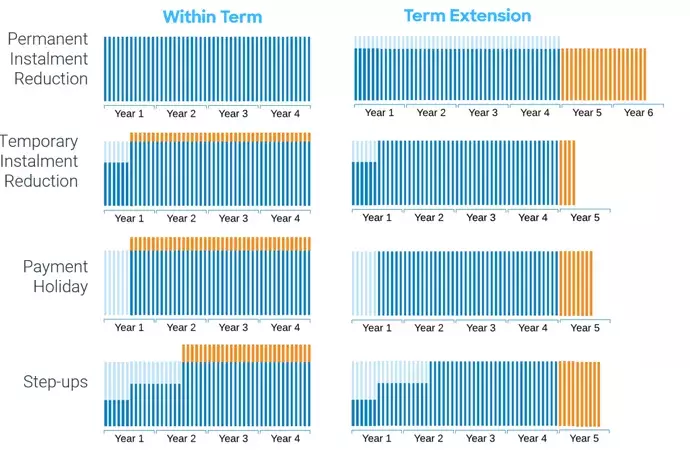

The use of repayment holidays or interest only restructures, doesn’t necessarily alleviate the problems faced by customers when a systemic shock is experienced, and a prolonged recovery is expected. Customers are faced with an even larger financial burden at the end of the forbearance period. If we consider this using the present value framework, a customer’s risk of default is temporarily reduced during the period of forbearance. When their payments resume the customer presents a greater risk of default that than they did when they requested assistance. Particularly if their circumstances remain unchanged. Concerns surrounding the financial cliff aren’t unfounded and, could be, underappreciated.

There are ways to help alleviate this burden when customers request hardship assistance. Waiving fees, interest and arrears over the forbearance period is one way, whilst extending the term of a loan is another. The below figure helps to highlight how different loan modifications affect the ongoing repayment schedule for customers even after assistance has been withdrawn.

Financial Cliff: What About Property Prices?

An obvious risk highlighted earlier in this post concerns a material drop in property prices, which is likely if property owners start to de-leverage or there is a move to act on impaired assets by the banks. Under this circumstance the cost of foreclosure or agreeing to a settlement with a customer could prove far more costly than restructuring a loan so that a customer can continue to service their debt. This however creates another problem for bank balance sheets. If the bank agrees to lower payments or foregone interest while mortgage LVRs increase this will impactthe bank’s Risk Weighted Assets, which .could have a significant impact on bank return on equity.

Another modification considered in the HAMP was principal write-down. How this measure could be mutually beneficial seems counter-intuitive at first glance. Reducing a customer’s principal reduces both the repayments and their LVR, the evidence from HAMP showed that a customer’s likelihood of default is influenced by both measures independently. Principal write-down was encouraged under HAMP and subsidies existed to promote this type of modification. Several colleagues at FICO have worked with lenders in the US on loan modifications and experience was that principal write-downs became an important hardship option. It gives the customer options once they are back on their feet and only reflects the potential shortfall the bank might face if they foreclosed.

Financial Cliff: Where Next?

While the industry in Australia looks to September and how to best manage their loans to customers at the end of the initial 6 month holiday, it appears that targeted payment deferrals will be the primary approach to address hardship while the path to recovery remains uncertain. The potential for ongoing, rolling lockdowns and the sheer number of customers impacted, highlights the problem we are facing as support is withdrawn. An approach to hardship that is both scalable and customer-focused is vital.

Bank staff need to be enabled to execute the bank’s hardship strategy. Tools are required to help formulate and quantify the impact of hardship policy on those customers seeking assistance. This involves identifying who you want to help and how. Then there are those at the coalface speaking directly to customers. Do they have the tools to capture what information is important and make a decision with each customer on the best way forward?

Finally, it is true to say that historically, hardship has been a tiny part of bank-operations and has remained a very manual process because of it. Building out a digital pathway for customers to seek assistance, formalising a consistent and fair assessment methodology and leveraging alternative data to assist with the assessment is the only way to address the scale of the problem. Throwing more people at the problem won’t be sustainable as a solution to this situation.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.