Survey: Real-time Payments Fraud Up for 4 out of 5 APAC Banks

Additional identity and authentication technologies needed with fraud expected to increase in 2020

There has been a proliferation of real-time payments fraud, as new near-instant payment platforms, including person-to-person (P2P) transfers and mobile payment platforms grow across Asia Pacific.

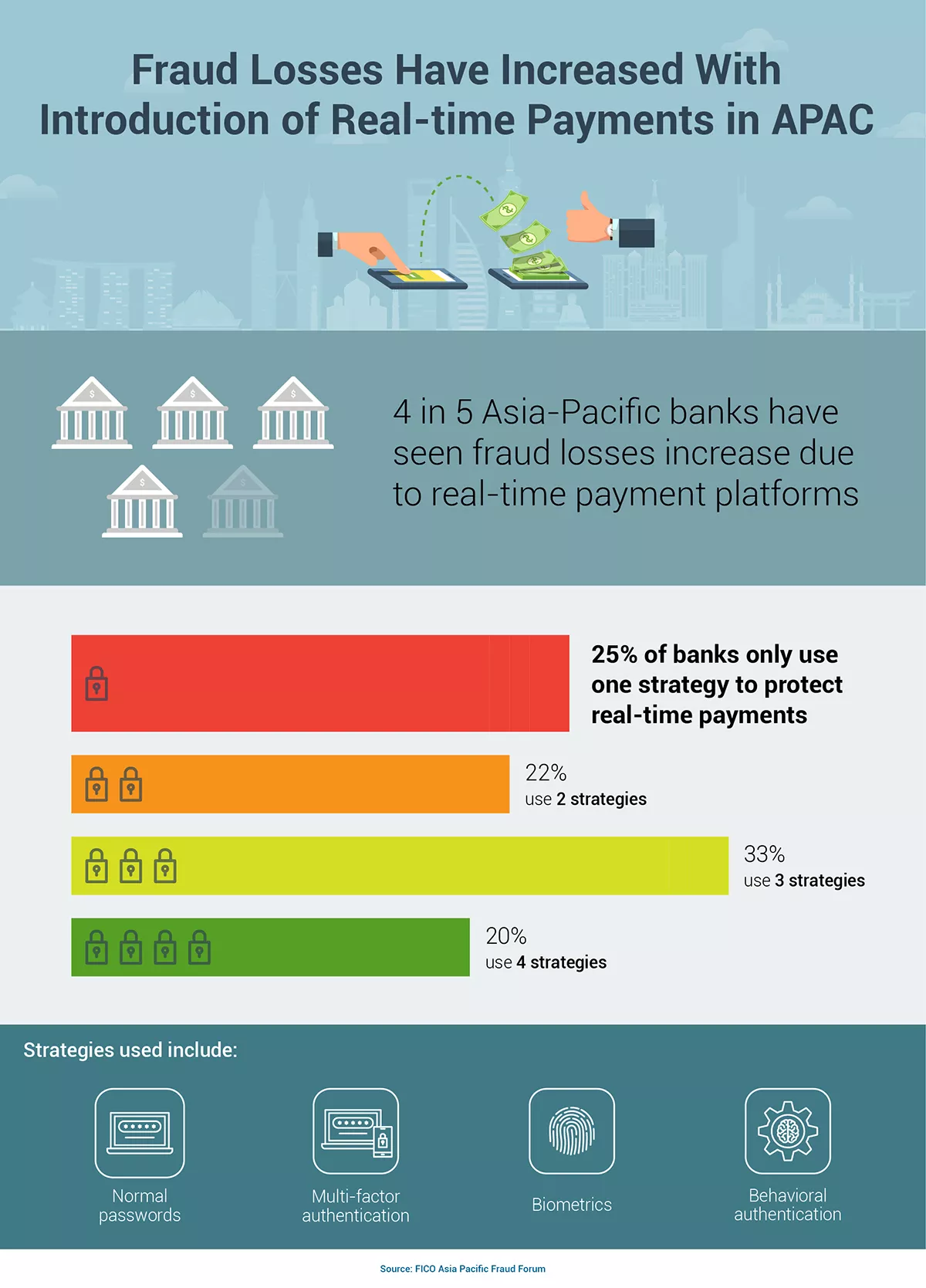

We recently conducted a survey with banks in the region and found that 4 out of 5 (78 percent) have seen their fraud losses increase.

Further to this, almost a quarter (22 percent) say that fraud will rise significantly in the next 12 months, with an additional 58 percent saying they expect a moderate rise in fraud.

While the convenience of real-time payments is great news for customers, increasingly, banks have zero time to clear a transaction or payment. AI can’t slow down the clock, but it can help create systems that are radically quicker to recognize a transaction that smells likely to be fraudulent. Banks will need to move beyond passwords and OTPs and add biometrics, device telemetry and customer behavior analytics to keep up with the changing payments landscape.

Real-time Payments Fraud Defence Strategies

Banks were asked which identity and authentication strategies they used, with the majority saying they used multifactor authentication (84 percent). They also increasingly use a wide range of authentication methods including: biometrics (64 percent), normal passwords (62 percent) and in last place behavioral authentication (38 percent). Interestingly, nearly half of the respondents (46 percent) are currently only using 1 or 2 of these strategies, potentially leaving them more exposed to attack vectors such as identity theft, account takeovers, cyberattacks.

Why try to crack a safe when you can walk in the front door? Criminals are trying to fool banks into thinking they are new customers or stealing account access by tricking people into making security mistakes or giving away sensitive information. When they are successful, criminals are making use of real-time payments to move funds quickly through a maze of global accounts.

The survey bore this out with 40 percent of banks in FICO’s survey naming social engineering as the number one fraud concern when it comes to real-time payments. Account takeovers were ranked second, with false accounts and money mules also rated as problems.

New forms of biometric, multifactor and behavioral technologies allow banks to stop payments being made, even if an account appears to be using the correct but stolen password or entering the right, but intercepted, one-time-password.

Beyond this type of account take over, we also have authorized push payment fraud, such as when a customer is tricked into paying what they think is a legitimate invoice like a fake school bill or payment to a tradesperson. This type of social engineering is harder to stop but better KYC, link analysis to find money mule accounts and behavioral analytics to flag new accounts for a regular payee, are all examples of how to tackle it.

Real-time Payments Fraud: Time For Convergence

Further to stopping fraud in real-time payment platforms, crimes such as drug trafficking, human smuggling, tax evasion and terrorism finance are also attracted to the irrevocable nature of instant payments. The lack of visibility between jurisdictions has seen regulators encouraging banks to move quickly in this cross-border payments space to ensure payments are compliant and secure.

In terms of mitigating this criminal behavior, more than 90 percent of APAC banks surveyed thought that convergence between their fraud and compliance functions would be helpful in defending transactions on real-time payments platforms.

We estimate that there is about an 80 percent overlap in software functionality between legacy fraud and anti-money laundering systems. To tackle fraud and money laundering schemes that exploit real-time money movement you need to leverage all the available technologies, automate as much as you can and introduce models that can identify outlier transactions and customer behavior so your teams can spend their time investigating the riskiest of the red flags.

FICO surveyed 45 executives from financial institutions across the region at its annual FICO Asia Pacific Fraud Forum.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.