Top 5 Scores Posts of 2020: Keeping Credit Flowing During Uncertain Times

Pandemic impact on FICO Scores and the introduction of the FICO Resilience Index

The COVID-19 pandemic cast a huge shadow on the financial services worldwide. The FICO Blog posts last year reflected that – we wrote about everything from the impact on collections, proactive lender communications with consumers, issues with fraud, and of course, how FICO® Scores were impacted.

We hope that what readers learned helped instill confidence in keeping credit flowing during uncertain times. In our top post, Vice President and General Manager of Scores, Sally Taylor explained the new FICO Resilience Index, designed to provide lenders with a more precise assessment of consumer credit risk and consumers with demonstrated talent for weathering economic storms greater access to credit.

And while there continues to be uncertainty about the economy, FICO® Scores were steady.As three of our top five posts explain, medical conditions or diseases have no impact on a consumer’s FICO® Score, nor do loan forbearances or deferred payment agreements. And as our fourth most popular post explains, the average U.S. FICO® Score is actually 5 points higher than the average score last year, further illustrating the lag between when a major macroeconomic event occurs and when the FICO® Score reflects that event on an aggregate basis.

Here are the top five posts from 2020 related to the FICO Score:

FICO Resilience Index Now Available For Lenders To Pilot

“Unlike the FICO® Score, which ranges from 850 to 300, the FICO® Resilience Index outlines a scale from 1-99. Consumers with scores in the 1 to 44 range are viewed as the most prepared and able to weather an economic shift,” Sally Taylor explains in her blog post announcing the June 29 release of the FICO the FICO® Resilience Index, which “provides an additional layer of insight to help more accurately capture the resilience of a consumer and empower lenders to provide access to credit during difficult economic times.”

Sally notes that analysis of FICO® Resilience Index data by Tom Parrent, former chief risk officer for Genworth Financial, shows that from 2010 to 2015, nearly 600,000 additional mortgages could have been originated to consumers with FICO® Scores between 680 and 699, had the FICO® Resilience Index been available to lenders at the time. In a white paper, Tom called the FICO® Resilience Index, “a significant step forward in consumer credit modeling” and “a significant addition to the toolkits used by risk managers, portfolio managers, loan servicers, originators and regulators,” with a wide range of use cases for the mortgage industry, ranging from stress testing to risk-based pricing to loan servicing.”

“By studying past recessions, we know that in a down economy credit criteria goes up and access to credit goes down as lenders try to mitigate credit risk. The FICO® Resilience Index can be helpful in navigating through changing economic cycles,” Sally continues. “The desired outcome is for lenders, borrowers, and investors to benefit from a system that is even more precise in assessing risk, and less prone to broad credit restrictions and undifferentiated risk pricing, which can tighten the flow of credit during an economic downturn.”

For more information, you can listen to Sally’s FICO virtual resilience keynote here.

Protecting Your Credit During The Coronavirus Outbreak

“As the number of coronavirus cases spreads, it is also having negative impact on the financial health of the economy at large and the economic well-being of individuals across the United States,” Tom Quinn noted in his post discussing the pandemic’s impact on credit scores. “The unusual nature of this pandemic has resulted in the temporary closing of schools, cancellation of events and the disruption of the distribution of goods and services that may have the unintended consequence of impacting some people’s ability to pay bills on time.”

In other words, no reader of Tom’s blog was alone in wondering what might happen if they missed a payment on a loan or credit card, or how decisions forced by the pandemic might affect their access to credit in the future.

To help readers affected by COVID-19, Tom offered the following tips:

- Medical conditions or diseases are not considered by FICO Scores and will not directly impact a FICO Score. However, the potential financial “fall out” of missing a payment, charging credit cards up to and over their limit or opening several new credit accounts over a short period of time can have a negative impact on the scores.

- Before bill payments are due, you should contact your bank and other creditors as soon as possible to make them aware of your situation. Your lender will likely have procedures in place to work with customers impacted by this unique health emergency.

- Try discussing a credit increase or deferred payment plan with your lender, or request to temporarily place the loan in forbearance (meaning you may get temporary relief from having to make full payments on your credit obligations). The placement and reporting of an account in forbearance or a deferred payment plan in and of itself does not negatively impact a FICO® Score, and this holds true with all versions of the FICO Scores.

- Keep in mind that your prior history of payments will continue to be considered in the calculation of your FICO® Scores. So too will other information that your lender regularly updates on the account, such as current balance and payment status. As such, you may want to also check with your lender on how they intend to report these fields while the account is in forbearance or a deferred payment plan.

Credit Reporting in the U.S. During the COVID-19 Pandemic

Also landing in the top five during a unique market environment, this FICO-penned update shared our response to Americans worried about the COVID-19 pandemic’s impact on FICO® Scores:

“We at FICO recognize the significant challenges faced by both borrowers and lenders in these extraordinary times. We've been working closely with lenders as well as our Credit Reporting Agency (CRA) partners throughout the COVID-19 pandemic to provide awareness of the various reporting options open to data furnishers, as well as how those reporting options can impact consumers' FICO® Scores.

“Many lenders are offering multiple options to consumers, including temporary deferred payment plans and/or placing loans in forbearance.

“We have emphasized to data furnishers that while special comment codes (like AW for natural disasters or CP for forbearance) are an additional option for reporting a borrower's situation, these are temporary codes that will only be reflected in the credit file for as long as they are being furnished, which is typically only while the extraordinary circumstances are in effect. There is an alternative approach that can better protect COVID-19-impacted consumers' FICO® Score over the long term.

“Therefore, as lenders are assessing how customers have been impacted by the COVID-19 pandemic, and how to report all key credit data fields in a manner that best reflects each customer's situation, using special comment code alone should not be viewed as providing consumers relief with respect to the FICO Score. Placing borrowers in a temporary deferred payment plan or in forbearance, along with reporting an account status as "current" instead of as "delinquent", will permanently ensure that a borrower's FICO® Score won't be impacted by late payments related to the effects of the COVID-19 pandemic.”

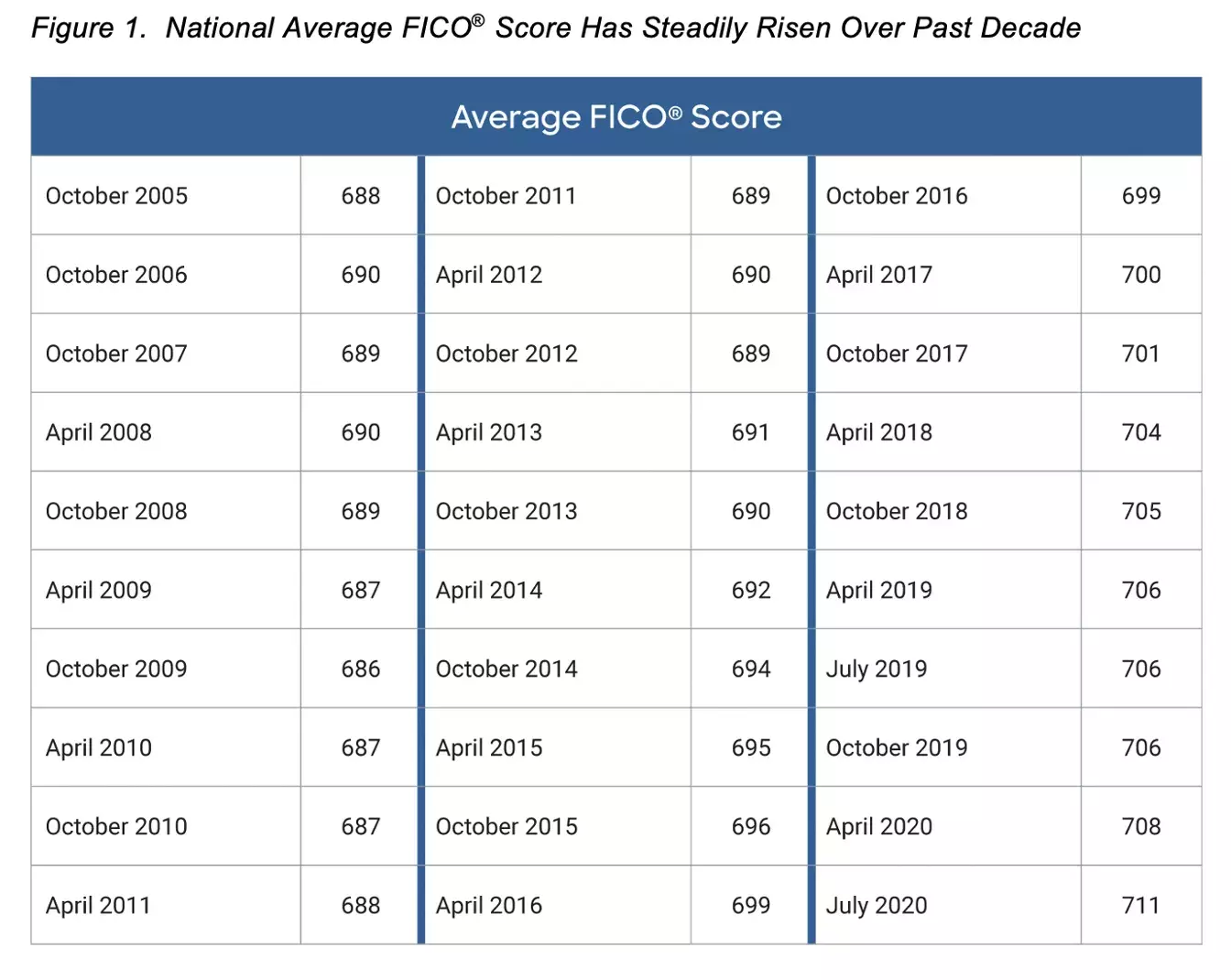

Average U.S. FICO Score at 711, But Uncertainty Abounds

The first of two updates from Ethan Dornhelm on our list, this blog explained why the average U.S. FICO® Score was 711 in October 2020 – a full 5 points higher than the average FICO® Score reported a year before.

Acknowledging that this number “is likely to be viewed as a surprise result in light of the impacts that the COVID-19 pandemic has had on U.S. consumers and the global economy,” Ethan clarified that, rather than measuring the economy’s direction, “there is a bit of a lag between when a major macroeconomic event occurs and when the FICO® Score reflects that event on an aggregate basis.”

“And that’s because it generally takes a few months for the effects of that event and the accompanying financial strain to start to show up in consumers’ credit reports, in the form of rising balances, credit seeking behavior, and eventually for some, missed payments,” he continued. “For example, during the Great Recession, the average national FICO® Score didn’t hit its lowest point until late 2009, well after the recession was underway.

“In the case of the COVID-19 pandemic,” Ethan writes, “the lag between the onset of the pandemic and when credit files begin to show the financial strain that millions of Americans are feeling is further affected by the significant steps taken by both the government (stimulus spending) and private sector (lender payment accommodations) to help consumers ‘bridge the gap’.”

So why is the average American’s FICO® Score higher than consumers might expect? Ethan offers three key insights:

- Missed payments reported in the credit file are down. As of July 2020, just 7.3% of the population had a 90+ day past due missed payment in the past 6 months. This is down from 8.1% pre-COVID (Jan 2020), with the above-mentioned combination of government stimulus programs and payment accommodation programs apparently enabling consumers to keep up with their bills. Staying up to date on bills can have a substantial and positive impact on your FICO® Score, representing some 35% of the overall FICO® Score calculation.

- Consumer debt levels are decreasing. Whether due to reined in spending in the face of the economic uncertainty wrought by the pandemic, or simply due to having fewer opportunities for spending on discretionary items such as restaurant, retail, and travel, as of July 2020, U.S. consumers had on average $6,004 in credit card debt, down from an average of $6,934 back in January 2020. A reduction in amounts owed (30% of the FICO® Score calculation), and especially the amount of credit card limits being used can yield measurable gains in a consumer’s FICO® Score.

- The FICO® Score doesn’t negatively consider forbearance/deferment agreements. In fact, placing a consumer in forbearance or deferment, along with reporting the account status as "current" instead of as "delinquent", will permanently ensure that their FICO® Score won't be impacted by late payments related to the effects of the COVID-19 pandemic.

How FICO Helps Protect Your Score During COVID-19

In his second most popular blog entry, Ethan Dornhelm explained exactly how the loan forbearance or deferred payment agreements being offered by many lenders during the pandemic would affect their FICO® Scores.

“Many forbearance and deferral programs are meant to provide assistance to consumers who have seen sudden disruptions to their income as a result of COVID-19 and protect those who have been impacted financially by the pandemic from suffering immediate, short-term harm to their credit,” he explained. “However, some consumers have reported seeing non-FICO credit scores drop after entering into one of these agreements.”

With that in mind, here are a few things FICO wants readers to know about the impact that entering into a loan forbearance or deferral agreement can have on their credit.

- The FICO® Score Doesn’t Negatively Consider Forbearance/Deferment Agreements. Every FICO® Score model is specifically designed to ensure that consumers won’t see their score negatively impacted by credit reporting codes related to entering into these agreements. This approach is supported by data and ensures that consumers are treated fairly while maintaining the predictive integrity of the score. Since the pandemic first hit, FICO has been working closely with lenders on the appropriate use of these coding practices.

- Impacts to Other Credit Scoring Models will not Impact Consumers’ FICO® Scores. Even if other credit scoring models include treatment of the credit reporting codes related to loan forbearance or deferred payment plans that result in lower scores, rest assured that these score drops have no bearing on your FICO® Score. The FICO® Score is the industry standard in credit scoring, used in more than 90 percent of U.S. lending decisions (Mercator Advisory Group Analyst Report 2018). Even though consumers may also have access to other credit scoring models, such as through personal finance sites, most lenders use the FICO® Score when making a decision on credit applications.

- FICO’s Open Access Program Helps Consumers Access their FICO® Scores. Through the FICO® Score Open Access program, launched in 2013, FICO works with over 200 leading financial institutions nationwide to give consumers free access to the FICO® Scores they use to manage credit accounts, thus creating more transparency between consumers and lenders by sharing the scoring model used in most credit decisions. In addition to their FICO® Score, Open Access also provides consumers with the top two reason codes that are impacting their score, offering consumers further insight into their credit (for instance by highlighting the impacts of their credit utilization or overdue payments) and put themselves on the path to stay on top of their financial future.

Even though forbearance and deferral agreements should not be affecting their FICO® Score, Ethan notes that it’s still important for readers to regularly monitor their FICO® Score and credit report, especially during turbulent economic times.

“If you believe one or more of your accounts has been improperly reported, you should contact the lender who reported this information and file a dispute with the credit bureau(s),” he writes.

To find out which lenders participate in Open Access, visit ficoscore.com/where-to-get-fico-scores.

For additional resources on protecting your credit during COVID-19, visit ficoscore.com/coronavirus.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.