Top 5 Scores Topics of 2021

Our top FICO Scores posts explored the expansive reach of the FICO® Score suite, as well as dispelling common misconceptions surrounding FICO® Scores.

In 2021, the financial services world continued to grapple with the uncertainty brought on by year two of the COVID-19 pandemic. Despite the continued concerns, we were encouraged to see the growth of the average U.S. FICO® Score, as stated in our top post of the year. Other top FICO Scores posts explored the expansive reach of the FICO® Score suite, as well as dispelling common misconceptions surrounding FICO® Scores.

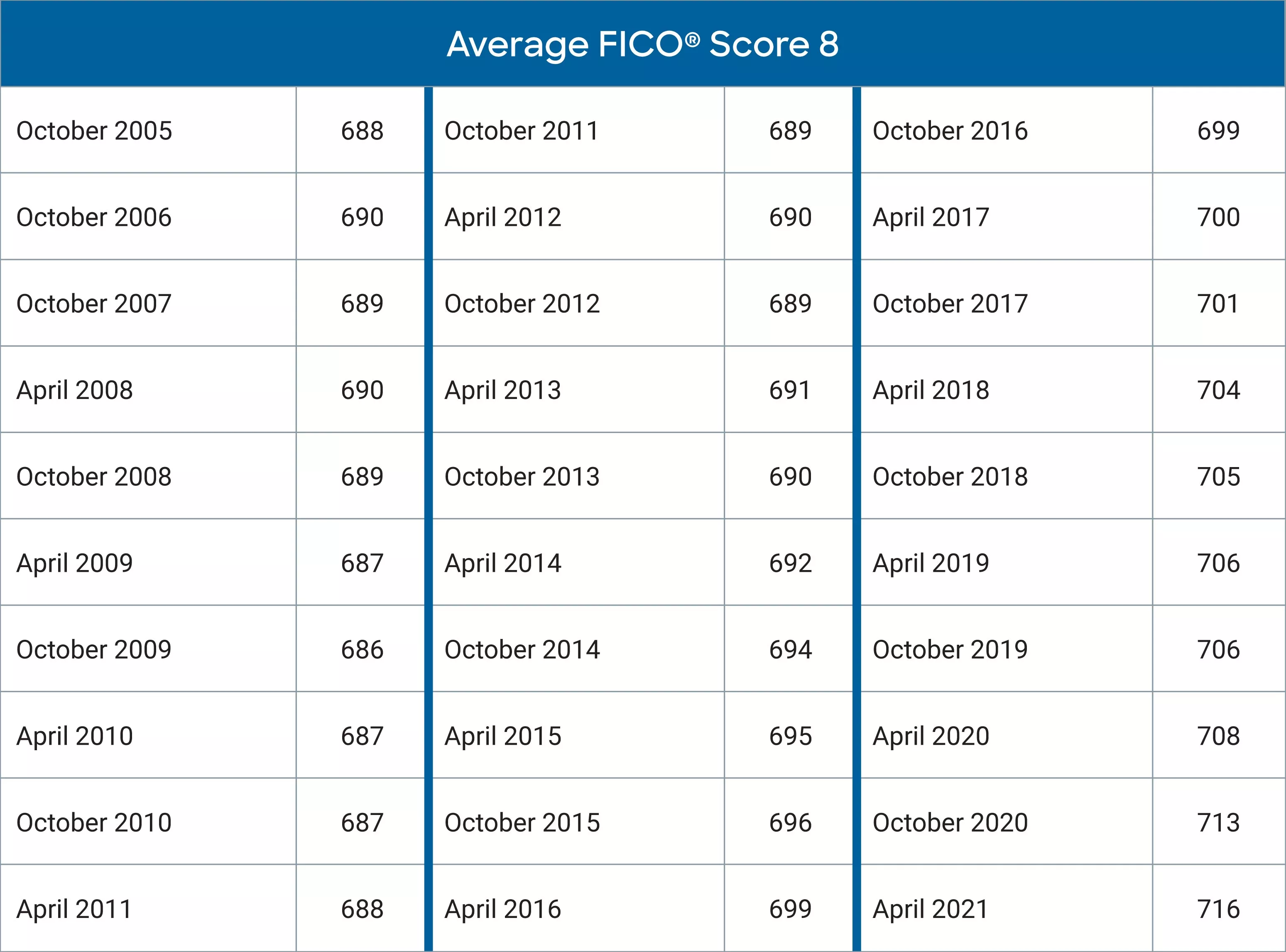

Average U.S. FICO® Score At 716, Indicating Improvement In Consumer Credit Behaviors Despite Pandemic

Ethan Dornhelm wrote: The FICO® Score is the lingua franca, or common language, for the credit scoring industry. It serves as a broad-based, independent standard measure of credit risk. It is relied upon by stakeholders across the entire lending ecosystem – from regulators, investors and boards to consumers, lenders, and brokers – as a baseline metric for assessing credit risk that is fair to both lenders and consumers.

Each year, we share the average U.S. FICO® Score, which now stands at 716. This is eight points higher than it was one year ago, and five points higher than the last time we reported on the average FICO Score in October 2020. At that time, the news that the FICO Score had trended up in the early months of the COVID-19 pandemic was greeted with some surprise. But there is considerably less surprise about these latest results: the data shows that a growing economy, accompanied by historic home price appreciation, strong performance of equity markets, and evidence that the payment accommodation programs offered by lenders since the onset of the pandemic have helped (and are continuing to help) affected borrowers bridge the gap that opened up in their finances as a result of COVID-related income loss.

Figures 1. National Average FICO® Score Has Continued to Rise Through the Pandemic; FICO Score® Distribution Shows Similar Trend Towards Higher Scores

Figures 1. National Average FICO® Score Has Continued to Rise Through the Pandemic; FICO Score® Distribution Shows Similar Trend Towards Higher Scores

Though it might sound obvious, the drivers of the continued improvement in the average FICO® Score are continued improvements in key metrics considered by the score: fewer missed payments, lower consumer debt levels, and reduced credit seeking behavior. Let’s dive into each of these in a bit more depth:

- Missed payments reported in the credit file are down significantly. As of April 2021, just 15% of the population has had a 30+ day past due missed payment in the past year. This is down from 19.6% as of April 2020. As shown in figure 3, recent missed payments are down across key product types. While millions of U.S consumers have experienced disruption to their income since the onset of the pandemic, the combination of government stimulus programs such as the CARES Act and payment accommodation programs being offered by lenders continues to enable many consumers to avoid falling behind on their bills. Staying up-to-date on your bills can have a substantial and positive impact on your FICO® Scores. In fact, this ‘payment history’ dimension of the credit file represents some 35% of the overall FICO Score calculation.

- Consumer debt levels are decreasing. The uncertainty brought on by COVID-19, coupled with the fact that consumers simply had fewer opportunities to engage in discretionary spending during the lockdown phase of the pandemic, had a material impact on consumers’ willingness and ability to spend. Mix in the fact that many consumers – enabled, in part, by historic levels of savings at least partly driven by government stimulus such as enhanced unemployment benefits – have shifted their focus to paying down their credit card debt, and the result is a greater than 10% decrease in the average credit card balance and utilization of the U.S. consumer. “Amounts owed” comprises some 30% of the overall FICO® Score calculation and is heavily weighted towards credit card balances and utilization---so the observed reduction in credit card debt is helping to drive scores upwards.

- Fewer consumers are actively seeking credit. There has been a 12.1% year-over-year decrease in the average number of hard credit inquiries in consumers’ credit files. Hard credit inquiries represent instances where a credit file was requested by a lender in response to a consumer-initiated application for credit. This dip in credit seeking behavior likely goes hand-in-hand with the renewed consumer focus on reducing spending and paying down debt. The “new credit” dimension of the FICO® Score represents ~10% of the overall score calculation.

Read the full post: Average U.S. FICO® Score At 716, Indicating Improvement In Consumer Credit Behaviors Despite Pandemic

FICO Fact: Does FICO’s Minimum Scoring Criteria Limit Consumers’ Access To Credit?

In a new blog series called FICO Fact, FICO experts dive into the common misconceptions surrounding FICO® Scores. In the first post of the series addressing whether minimum scoring criteria limits the consumers’ access to credit, Joanne Gaskin wrote: Simply put, the answer is no. Over the last 30 years, FICO has continued to analyze the minimum amount of credit bureau data that is necessary to deliver a reliable, predictive FICO® Score to the market - which benefits both consumers and lenders alike.

As a reminder, we have found that at least 6 months of credit history, as well as data reported within the past 6 months, is required in order to best ensure that the consumer’s current financial position is sufficiently reflected. Our research has consistently found that models that rely solely on sparse and/or outdated credit information are less reliable at forecasting future performance.

Diving in a bit deeper, this means that, unlike with other scores in the market, consumers that just opened their first trade line, such as a credit card, would not be eligible for a FICO® Score before they have ever made a single payment. A payment history of at least 6 months is necessary to derive a consistently predictive and reliable credit score. At any time, there are approximately 2.5M consumers that have recently opened a credit account, but don’t yet have the necessary 6 months of repayment experience in order to obtain a FICO Score based solely on traditional credit bureau data. Allowing consumers to build their credit repayment history over six months before assigning them a FICO Score will result in a consistently more accurate assessment of their credit risk, and with it, confidence by lenders to extend credit to these consumers at more favorable terms.

Delivering less predictive and often low scores to the market using only sparse and/or stale credit bureau data is not a recipe for helping consumers gain access to credit. FICO has found the answer to supporting lenders in identifying credit ready consumers is to augment traditional credit bureau data with FCRA compliant alternative data such as telecom, utilities, public record, and checking account data to provide a predictive and reliable score that lenders can use to responsibly expand access to credit.

Read the full post: FICO Fact: Does FICO’s Minimum Scoring Criteria Limit Consumers’ Access To Credit?

FICO Fact: Do FICO Scores Consider Telco And Utility Data?

Joanne Gaskin wrote: The unequivocal answer is yes! FICO® Scores have always considered telco and utility payment data that is furnished to the three nationwide U.S. credit bureaus: Equifax, Experian and TransUnion. The inclusion of telco and utility payment information dates back to the release of the very first FICO Scores in 1989.

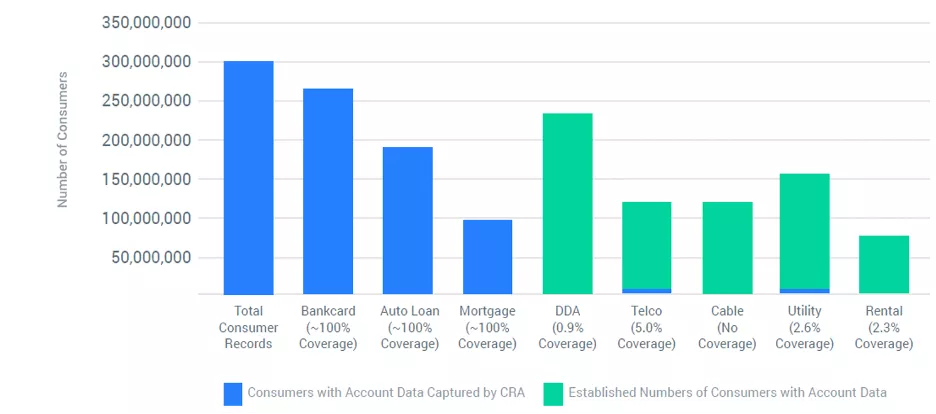

The next natural question is: how much of this data is available at the three nationwide credit bureaus? The answer is that while the availability of this data has been increasing, it remains far below other tradeline data such as credit cards, auto loans or mortgages. For example, in the US, 92 percent of consumers have cell phones, but just 5 percent of consumers have telco data reported in their traditional credit bureau files.

Figure 1: Credit bureau coverage is greater for some types of data than others

The story is similar for utilities, where over 60% of American adults pay for utilities such as gas, electricity and water, but just 2.4% of consumer credit bureau files contain utility (non-telco) payment information.

Read the full post: FICO Fact: Do FICO Scores Consider Telco And Utility Data?

FICO Fact: How Current Is The Data In My FICO Score?

Joanne Gaskin wrote: While the FICO® Score has been trusted by consumers, lenders and investors for decades, the data that goes into a FICO® Score can be as recent as a payment reported by your lender today.

When a FICO® Score is pulled, say, when a consumer applies for a loan or credit card, the most up-to-date information available at the credit bureaus is used to calculate the score. In fact, while other credit scoring models may generate a credit score based on stale credit information, our minimum scoring criteria requires that at least one credit account has updated information reported in the last six months.

How frequently the data is updated depends on where it resides:

Credit Bureau Data

FICO® Scores use data from the three main credit bureaus. This data is updated by thousands of data furnishers, usually on a monthly basis. It’s generally monthly because most loans (auto loans, mortgages, credit cards, etc.) are billed on a monthly cycle. As a result, these accounts are generally reported to the bureaus on a monthly cycle with information being reported each day of the month by different furnishers. Then, when a FICO® Score is pulled, it reflects the most up-to-date data reported to the credit bureaus. That information may have been reported to the credit bureaus as recently as that very same day.

Alternative Data

Some FICO® Scores use alternative data, which is predictive, regulatory-compliant and found outside of the credit bureau file maintained by the credit bureaus. Telco and utility payment data, similar to credit bureau data is generally reported on a monthly basis. The UltraFICO® Score empowers consumers to leverage their checking and savings account data to enhance their score. When the UltraFICO® Score uses this demand deposit account (DDA) data, it’s current as of the day prior to the score pull.

Read full post: FICO Fact: How Current Is The Data In My FICO Score?

Based on the 2020 US Census, the US credit-eligible population (those over 18 years of age) is 258 million people. But how many of those consumers can obtain a FICO® Score?

Calculations by FICO data scientists indicate that more than 232 million US consumers can be scored by the FICO® Score suite. That is 90% of the credit-eligible US population.

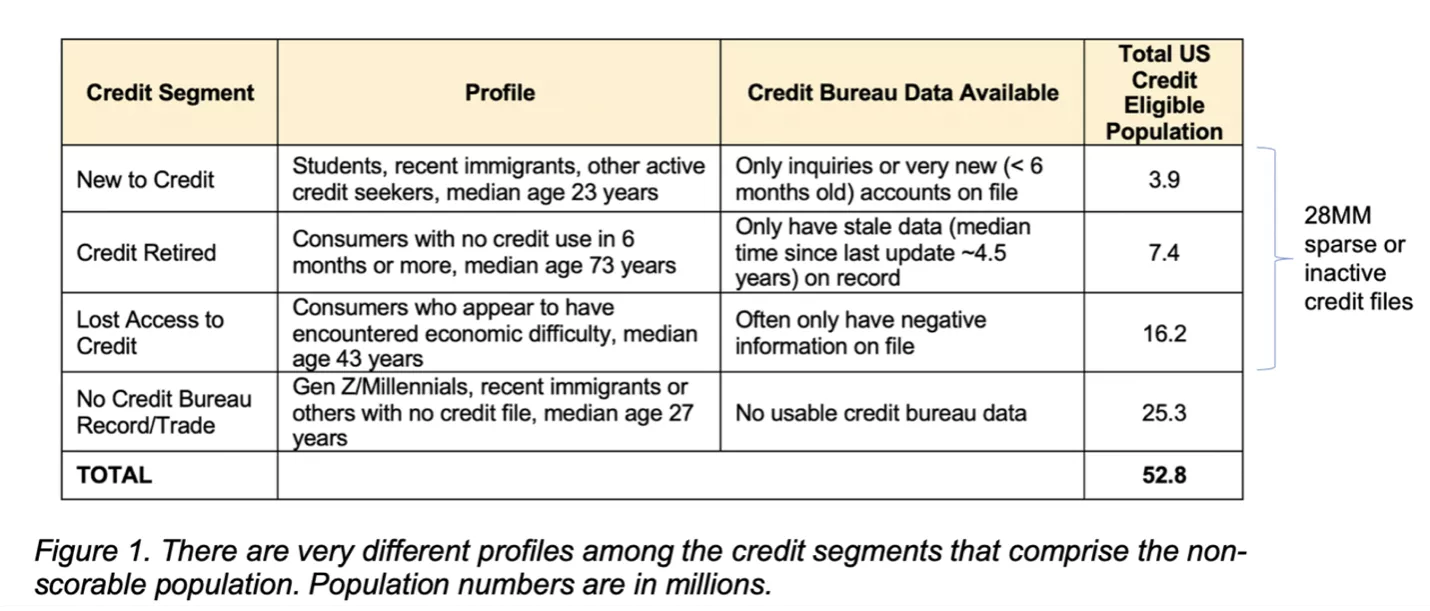

For most of the credit-eligible US population there is sufficient traditional credit bureau data available for calculating a FICO® Score. However, some 28 million consumers have minimal data available in their traditional credit bureau files, and another 25 million are considered ‘credit invisible’ and have no traditional credit bureau data at all. As shown in Figure 1, the profiles of these consumers that lack sufficient traditional credit bureau data can be quite varied.

To responsibly and reliably score consumers with sparse or no traditional credit bureau data requires a novel approach to credit scoring. Over the past decade, FICO has been developing innovative new scores – like FICO® Score XD and the UltraFICO® Score – which augment traditional credit bureau data with rich alternative data, such as telecom, utilities, public record, and checking account data.

With the introduction of these scores, the FICO Score Suite can now deliver reliable credit scores for more than 27 million additional people!

Read full post: More Than 232 Million Us Consumers Can Be Scored By The FICO Score Suite

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.