What Does The Rest of 2023 Have in Store for U.S. Credit Risk and FICO Score Trends

So far in 2023, consumers have braced inflation, a balanced housing market, looming prospect of a recession, removal of medical collections data, and student loan forgiveness plan

We’re almost at the mid-way point of 2023, and it is shaping up to be a year of opposing forces. Consumers face debt burden challenges that could impact U.S. credit risk and FICO® Score trends. At the same time, increasing adoption of recent innovations in credit scoring solutions should benefit consumers, leading to greater consumer empowerment opportunities and credit access.

At the start of the pandemic, uncertainty surrounded where the U.S. economy, credit scores, and credit risk trends were headed. There was an immediate and large-scale effort by both the U.S. government and financial institutions to implement significant guard rails and safety net programs for consumers such as the government stimulus, extended unemployment benefits, and payment accommodations. Consumers, in turn, responded by reducing spending, paying down debt, increasing savings, and seeking less credit. Not surprisingly, there was a noticeable uptick in the average U.S. FICO® Score in 2021 despite the pandemic.

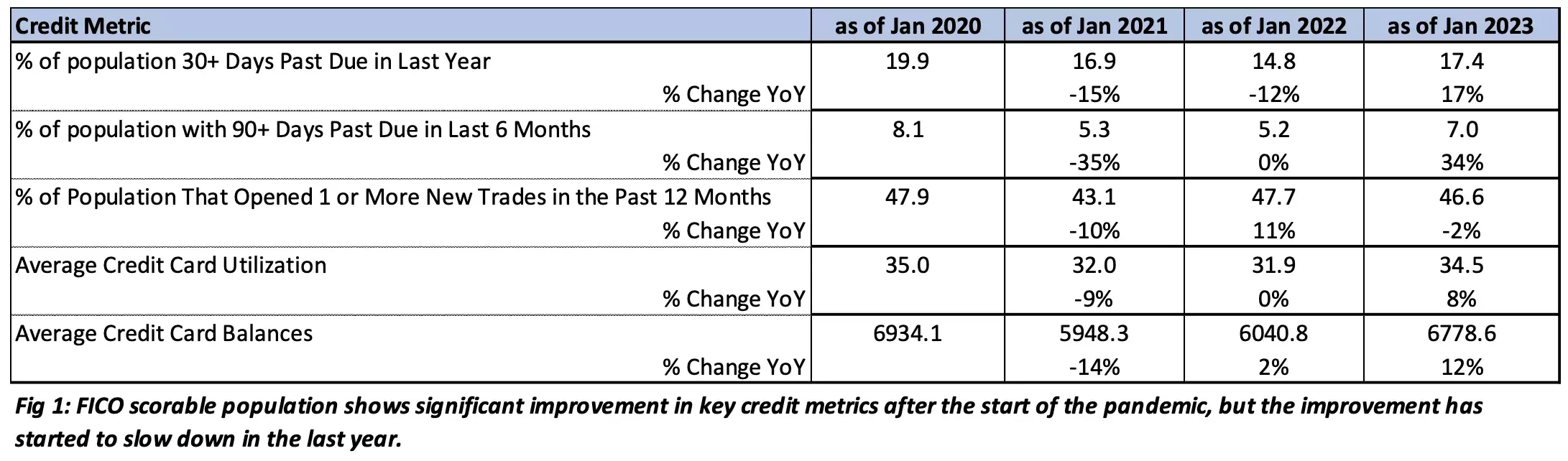

However, since April 2021, the average FICO® Score in the U.S. has remained steady at 716. This is noteworthy because it breaks the decade-long streak of year-over-year increases in the average FICO® Score. This can be linked to the guard rails implemented at the start of the pandemic having gradually ramped down. The removal of these safety nets, coupled with the re-opening of the economy, have driven consumers to carry increased levels of debt and exhibit greater amounts of credit seeking behavior and elevated missed payments (as shown in Figure 1), leading to a leveling off of the average FICO® Score. It should be noted that there is a bit of a lag between when a major macroeconomic event occurs and when the FICO® Score reflects that event on an aggregate basis. And that’s because it generally takes a few months for the effects of that event and the accompanying financial strain to start to show up in consumers’ credit reports, such as in the form of rising balances, credit seeking behavior, and eventually for some, missed payments.

It has been almost fourteen years since the average FICO® Score of U.S. consumers decreased on a year-over-year basis. As consumer debt and delinquencies trend back towards pre-pandemic levels, could 2023 be an inflection point for the average FICO® Score of U.S. consumers?

Recent developments in the U.S. economy and consumer credit data present potential headwinds and tailwinds alike for consumer credit and scores. These include federal efforts to combat high inflation, a balanced housing market, the looming prospect of a recession in the U.S economy, the removal of medical collections data from consumer credit files, and the final outcome of the student loan forgiveness plan by the current administration. Additional factors that can be mentioned here are uncertainty over raising the U.S. debt ceiling and its impacts and geopolitical risks.

While inflation has persisted since mid-2021, it appears to be slowing down, though consumer prices still remain high. Rising debt levels are likely to have been impacted by inflation, though inflation in and of itself is unlikely to have materially moved aggregate FICO® Score trends (e.g., an increase of a few percentage points in debt level isn’t likely to meaningfully impact aggregate FICO® Score). However, the impact of increased debt levels on the FICO® Score could mean a difference for that segment of consumers who are on the edge in terms of debt-to-income levels, particularly if they have seen a reduction in their savings cushion with the ramp down of government benefits and programs to mitigate the effect of the pandemic.

The U.S. Federal Reserve (Fed) increasing interest rates since mid 2022 as a response to stubborn inflation levels has led to a cooling off of the housing market, both in terms of housing demand and prices, resulting in reduced home equity values and a higher interest burden on home buyers, particularly first-time buyers.

Higher interest rates are also a big reason why many economists have been predicting a recession in 2023 in the U.S., but expecting it to be a shallow downturn. The Fed projects the unemployment rate to rise from current rate of 3.6% to 4.5% in 2023. As in previous downturns, increased job losses would impact consumer debt and delinquency levels (and by extension, the average FICO® Score). The level of impact will be determined by the sectors of the labor market that ultimately experience the most job losses. Should job losses be mainly limited to white collar/ tech sector industries, the potential impact on aggregate consumer finances could be muted, due to the presence of savings and other safety nets available to workers in those sectors. As with previous recessions, a possible scenario is that lenders for unsecured credit products may pull back on the extension of credit, potentially leading to lower consumer spend levels, and thereby suppressing the growth of consumer debt.

Additional events in 2023 could also impact the credit reports of millions of consumers. First, the three main credit bureaus in the U.S. announced that, as of April 2023, medical debt collection accounts under $500 have been removed from consumer credit reports. Additionally, if the current administration’s proposed student loan forgiveness program is allowed to proceed in 2023, it could provide meaningful debt relief for up to 43MM consumers.

Credit Risk Assessment Trends

For a couple of decades now, there has been a growth in the use of alternative data (i.e., consumer data not included in the traditional credit file) for credit risk assessment. In recent years, technological innovations such as open banking have spurred the growth in consumers sharing their banking data with lenders, i.e., “consumer-permissioned” data. In periods of economic uncertainty, a credit risk score that takes both sides of the consumers balance sheet into consideration can yield a more comprehensive and balanced assessment of consumer credit risk, which enables lenders to pair consumers with a manageable level of debt. Therefore, we expect the use of consumer-permissioned data to grow in importance in the latter half of 2023. Products such as the UltraFICO® Score rely on demand deposit account consumer-permissioned data: this type of data could become increasingly important to credit risk assessment as it provides the “assets” side of the picture, in contrast to traditional credit bureau data which provides primarily the “liabilities” view.

Why do we think use of consumer-permissioned data will expand? For one, it appeals to consumers, who more than ever, want to take control of their financial health and credit, and seek more favorable credit terms. For example, traffic to myfico.com, FICO’s consumer portal offering credit education information, grew 84% in the year after the onset of the pandemic. Also, data aggregators continue to advance technology in this field, with improving user interfaces that make it easier for consumers to permission their data, and increasing standardization of APIs as adopted by financial institutions to give consumers greater visibility and control over their financial data.

Lenders, for their part, should find this type of consumer-permissioned data attractive for credit underwriting for the following reasons:

- It is very predictive, second only to traditional credit bureau data

- It is only available for use in credit risk assessment if the consumer contributes the data

- it is easy to explain to a consumer whose application has been declined

- it has the potential to drive more access to credit

FICO will continue its process of thoughtful innovation through the development of new and powerful credit risk assessment tools along with the evaluation of new and interesting alternative data sources to drive greater financial inclusion and credit access. We will also continue to closely monitor and report on FICO® Score trends in this blog, especially if we see evidence that the decade-plus run-up in U.S. average FICO® Score has reversed. Last, but certainly not least, we will continue to strive to engage more U.S. consumers in our credit data and credit score education offerings, including via myFICO.com, FICO® Score Open Access, and Score A Better Future. An empowered consumer is better positioned to withstand whatever the remainder of 2023 has in store, regardless of whether headwinds or tailwinds prevail.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.