Can Alternative Data Expand Credit Access?

Widespread adoption of credit scoring by financial institutions over the past 25 years has made credit available and affordable to a majority of US consumers. But millions don’t cu…

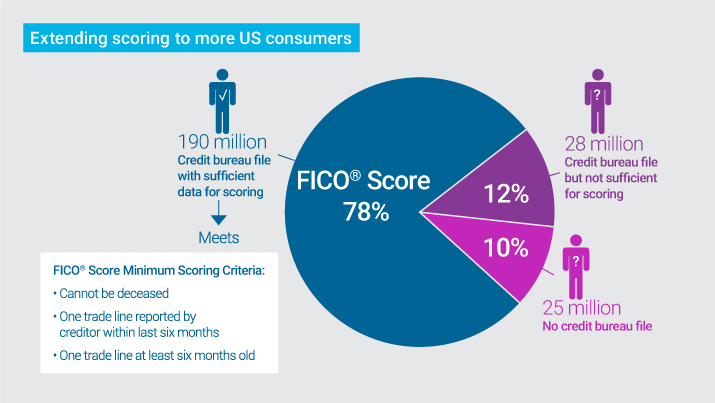

Widespread adoption of credit scoring by financial institutions over the past 25 years has made credit available and affordable to a majority of US consumers. But millions don’t currently have FICO® Scores because of sparse or old data in their credit files, or because they lack a credit file all together. This makes it difficult for them to establish credit, with many excluded from the mainstream financial system. This group frequently includes new immigrants, recent college graduates and those recovering from prior financial missteps.

Can scoring help lenders safely and responsibly extend credit to these consumers? New FICO research says yes—but only when credit bureau data is augmented by the right alternative data.

In fact, our research found that this approach makes it possible to generate predictive credit scores for more than 50% of previously unscorable credit applicants. Our study also showed that scores using alternative credit data help provide unbanked consumers a safe onramp to mainstream credit.

For further details on this study, I invite you to download our new Insights white paper: Can Alternative Data Expand Credit Access? In it, we present key findings showing how:

- Scoring more people without more data harms consumers and creditors

- Unscorable credit applicants are not all alike and shouldn’t be lumped together when building credit scores on this population

- Alternative data scoring releases millions stuck in a credit catch-22

- Millions can score high enough to qualify for credit, with most going on to improve their credit status

Our research has led us to conclude that there is demand and value in offering a score for lenders based on alternative data and the principles discussed in this white paper. To learn more, see the FICO® Score XD press release.

Popular Posts

Business and IT Alignment is Critical to Your AI Success

These are the five pillars that can unite business and IT goals and convert artificial intelligence into measurable value — fast

Read more

Average U.S. FICO Score at 717 as More Consumers Face Financial Headwinds

Outlier or Start of a New Credit Score Trend?

Read more

FICO® Score 10T Decisively Beats VantageScore 4.0 on Predictability

An analysis by FICO data scientists has found that FICO Score 10T significantly outperforms VantageScore 4.0 in mortgage origination predictive power.

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.