UK Cards Delinquencies Show Troubling Trends

Our analysis of UK cards data from the FICO Benchmarking Service has revealed some troubling trends in UK cards delinquencies. All average delinquent balances reached over two-year…

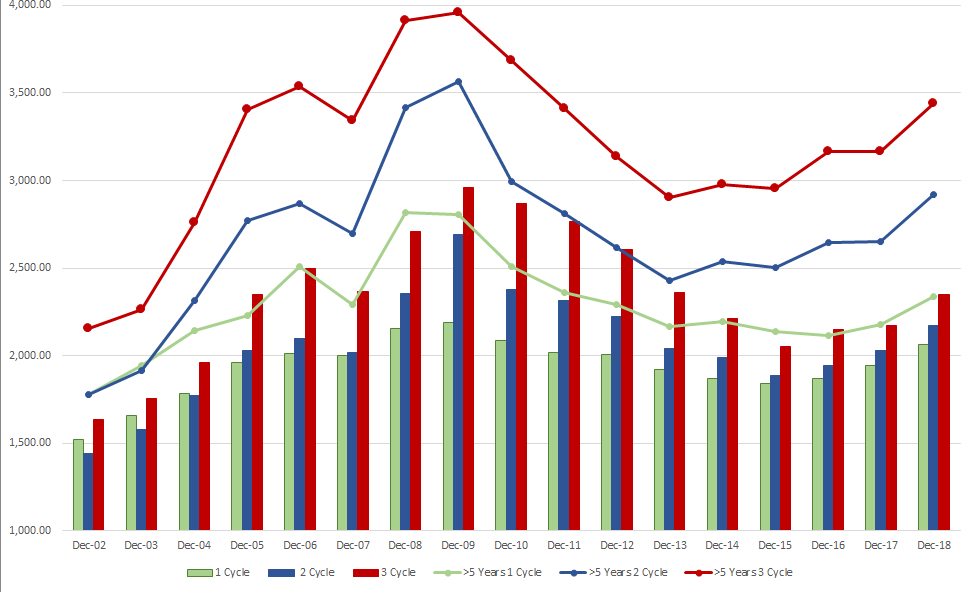

Our analysis of UK cards data from the FICO Benchmarking Service has revealed some troubling trends in UK cards delinquencies. All average delinquent balances reached over two-year highs in the fourth quarter of 2018.

Early cycles (1 to 2) were influenced by accounts >1 year on book and later stage (3+) by all vintages. The last time 1 cycle average balances were higher than December 2018 was 7 years ago and 2 and 3 cycles 8 years ago, in and post the last economic downturn.

When reviewing the data, it is important to look at different sub populations, including how mature the account is. For example:

- Accounts up to 1 year on book (New) produced the highest percentage of 1 to 3 cycle accounts.

- Accounts 1 to 5 years on book (Established) the highest % of balances in December 2018.

- Accounts 5 + years on book (Veteran) at 2 cycles report £748 above the overall average due to higher credit limits. Veteran average 2 cycle balances have grown 10% from December 2017 compared to a 0.9% growth in the average credit limit.

UK Classic Credit Cards — Average Delinquent Balances All Cards vs. Veteran Cards (5+ Years on Book)

New and Veteran Accounts

There are potentially concerning signs for New and Veteran accounts, as their percentage of 2 and 3 cycles reached over two year highs in December 2018, as did their average balances. The percentage of New delinquent balances was 32% higher than in December 2017 and % accounts were up 12.6%.

The New average amount overlimit also reached over a two-year high. As the percentage of accounts was stable, it means that higher amounts rather than a higher number of accounts are driving this result.

Although New average interest per active account was at its highest level in over two years, it is less positive for issuers if this is stemming from delinquency results.

Whilst the percentage of New accounts using cash decreased over the quarter, the percentage of the cash limit used was at its highest in over two years, up 7.2% compared to December 2017, which had a similar result to December 2016. This indicates that fewer accounts are using cash, but the amount they use is higher; this is typically considered risky behavior, taking into consideration the higher interest rates and fees associated with cash withdrawals.

In my next post, I will discuss the unused exposure on credit cards and share some more troubling data.

To learn more about our cards benchmarking service, or FICO’s new Risk Benchmarking Service which forms part of the Fair Isaac Advisors P&L Insight Service, please contact me at staceywest@fico.com.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.