How Did the Pandemic Affect UK Consumers’ Card Payments?

FICO data reveals that the positive payment behaviour from the pandemic is still persisting

The pandemic had many negative consequences for the economy in the UK and other markets, but it also appears to have had a lasting positive effect on UK consumers’ payment patterns. Our analysis of UK credit card payments data from the past six years has revealed that consumers developed healthier credit card payment patterns during the pandemic. What’s more, these patterns have persisted.

Why? The COVID-19 lockdown reduced spending opportunities, and some consumers received financial support from the government furlough scheme. Thus, many consumers were more able to make card payments.

Since the pandemic, consumers are paying off more of their outstanding balances and more are paying off the full balance. There are now fewer consumers paying off just the minimum and fewer pay off less than the minimum due.

Key Trends in UK Payments

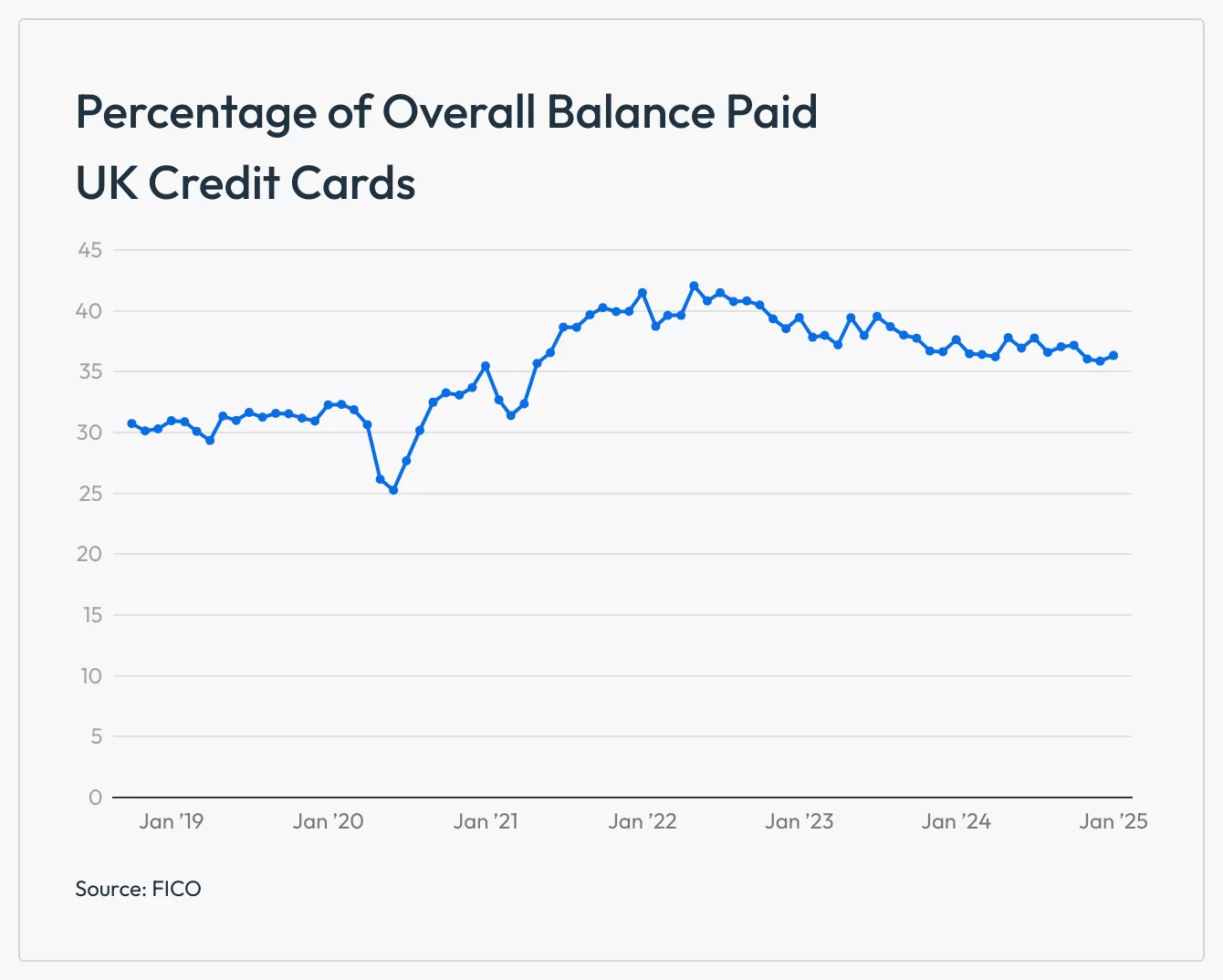

- The percentage of overall credit card balance paid has been trending down since peaking at 42% in May 2022, but remains 5% higher than pre-pandemic levels

- Since the end of the lockdowns, in July 2021, there has been a slight drop in the percentage of overall balance being paid, impacted by a 2% decrease in the percentage of consumers paying off the full balance

- From June 2020 the percentage of consumers paying off their full balance increased steadily, peaking at 55% in December 2022 and remaining steady at around 52% since

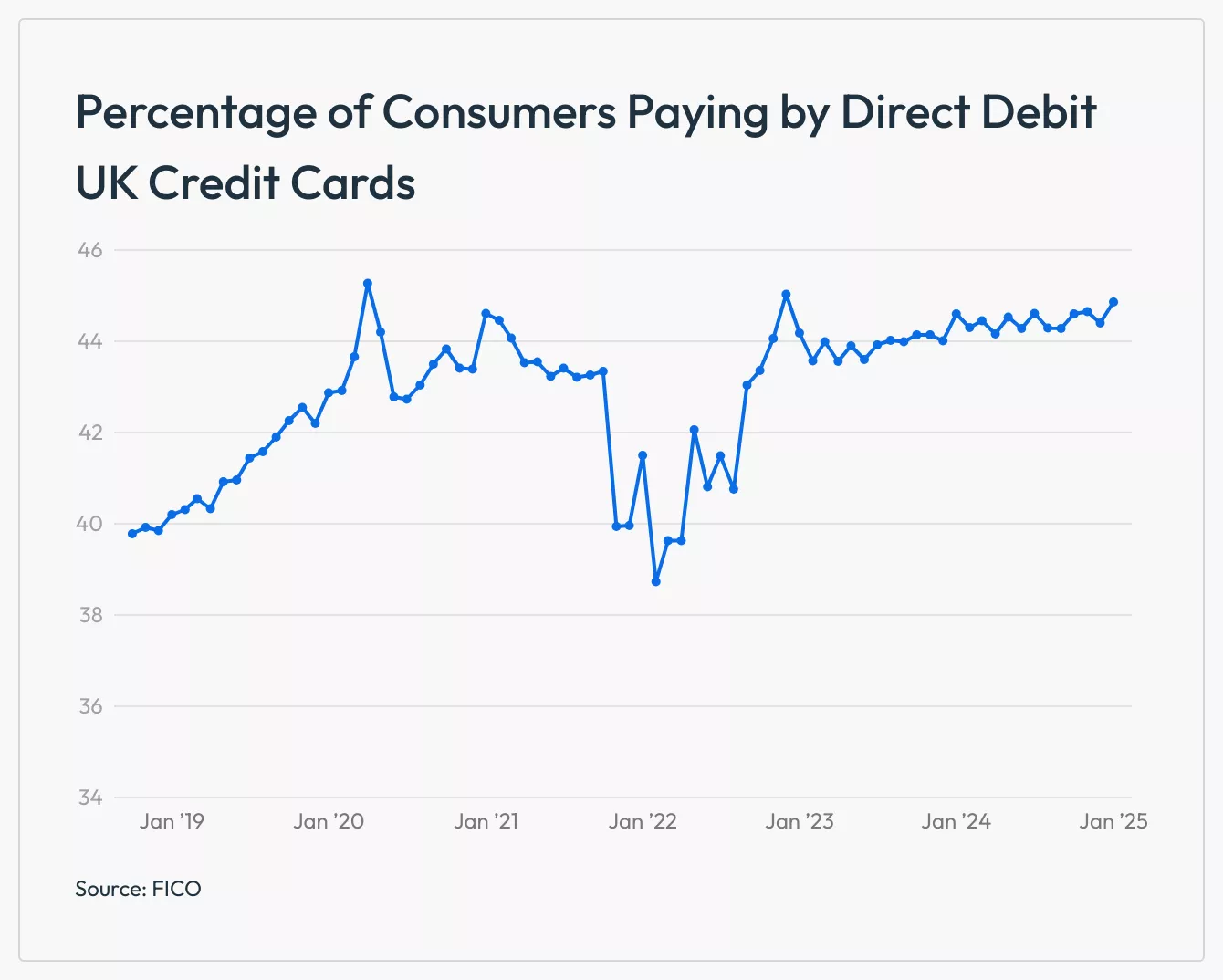

- Fewer Britons pay off less than the full credit card balance and more pay by direct debit, compared with pre-COVID

During the pandemic, the largest shift in UK credit card payment behaviour was that higher volumes of consumers paid off the full credit card balance, helped by fewer spending opportunities and the ability to save more. Consumers have continued to prioritise credit card payments, even during the cost-of-living crisis, and are still paying off more than just the minimum due. Fewer consumers are now paying off less than the minimum due.

As these customers have the potential to increase spend, issuers will want to ensure they get that business. Personalised offers and rewards based on their spend preferences, along with targeted promotions and flexible payment options, help to increase spend and loyalty.

Changes in UK Card Risk Patterns

Percentage of balance paid

Pre-COVID, an average of around 32% of the overall balance was paid each month. When the pandemic hit and lockdowns were enforced, consumers were paying off more of their outstanding balances, peaking at 42% in May 2022. This behaviour has been trending down ever since but is still approximately 5% higher than it was pre-pandemic.

Full balance paid

Before the pandemic, 45% of consumers were paying off their full balance. This increased every month between June 2020 and January 2021, reaching nearly 53%, then continued rising gradually until peaking at 55% in December 2022. While Christmas is usually a time of reduced payments, this peak clearly highlights the impact the pandemic had on typical spending habits. Since then, it has steadied and by January 2025 50% of consumers were paying off the full balance, still substantially higher than pre-COVID.

Minimum payments

Pre-pandemic, approximately 4.6% of consumers were paying off less than the minimum due. When the first lockdown began in March 2020, this increased, reaching a peak of 5.3% in May 2020. As the pandemic continued, the numbers paying less than the minimum due declined and since January 2022 volumes have remained steady, averaging 2.8%.

Direct debit payments

In October 2018, 40% of consumers were paying off balances by direct debit. This increased and peaked at 45% in April 2020, at the start of the first lockdown. By February 2022, this had dropped to a low of 39% before climbing back up to 45% in December 2022. Since then, it has remained fairly flat, averaging just under 45% each month. However, this percentage has been declining for newer customers.

Promoting payment by direct debit will help to reduce the number of sloppy payers and in turn, reduce the number of customers missing payments.

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80% of UK card issuers.

How FICO Can Help You Manage Credit Card Risk and Performance

- Explore our solutions for customer management

- See my post on UK Credit Card Trends 2023-2024: More Spend and Delinquencies

- Read more posts on UK cards

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.