Simulated FICO Score Impacts from Balance Aggregation due to Mortgage Forbearance

Research shows balance aggregation results in modest impact to FICO® Scores

This post presents new results following up our last blog post that described the FICO® Score impacts from simulating up to 12 months of mortgage forbearance accommodation. In the previous analysis, we enacted the simulation on all open mortgage accounts identified on a national sample of millions of U.S. consumers from late 2018. All stats shared in that post were based on the entire consumer population that has at least one open mortgage reported in their credit file. We have since obtained a sample from a more recent timeframe that reflects some of the early impacts of the COVID-19 pandemic (July 2020), which enables us to repeat the aforementioned analysis, but on consumers with open mortgage accounts that are indicated as being in some form of accommodation as of several months into the pandemic. Additionally, in light of proposals to extend forbearance, we have included a simulation up to 18 months of accommodation.

We ran three mortgage forbearance simulations: one assuming that monthly mortgage payments would be suspended for six months; one assuming that monthly mortgage payments would be suspended for 12 months; and one assuming that monthly mortgage payments would be suspended for 18 months. Other assumptions and aspects of the simulation were also executed the same as in the previous analysis, only on a much smaller segment of the mortgage-holding population this time, those actively in some form of accommodation.

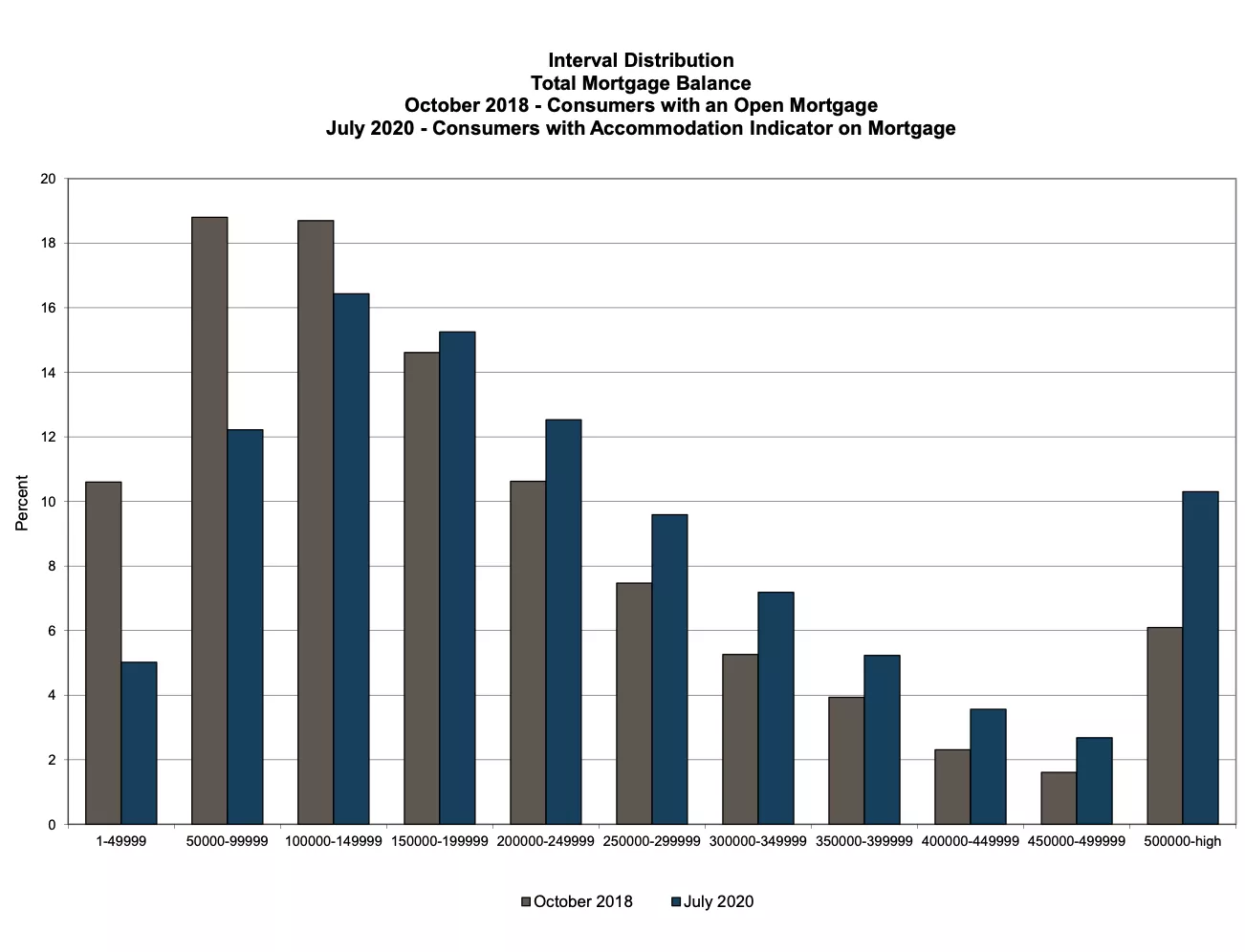

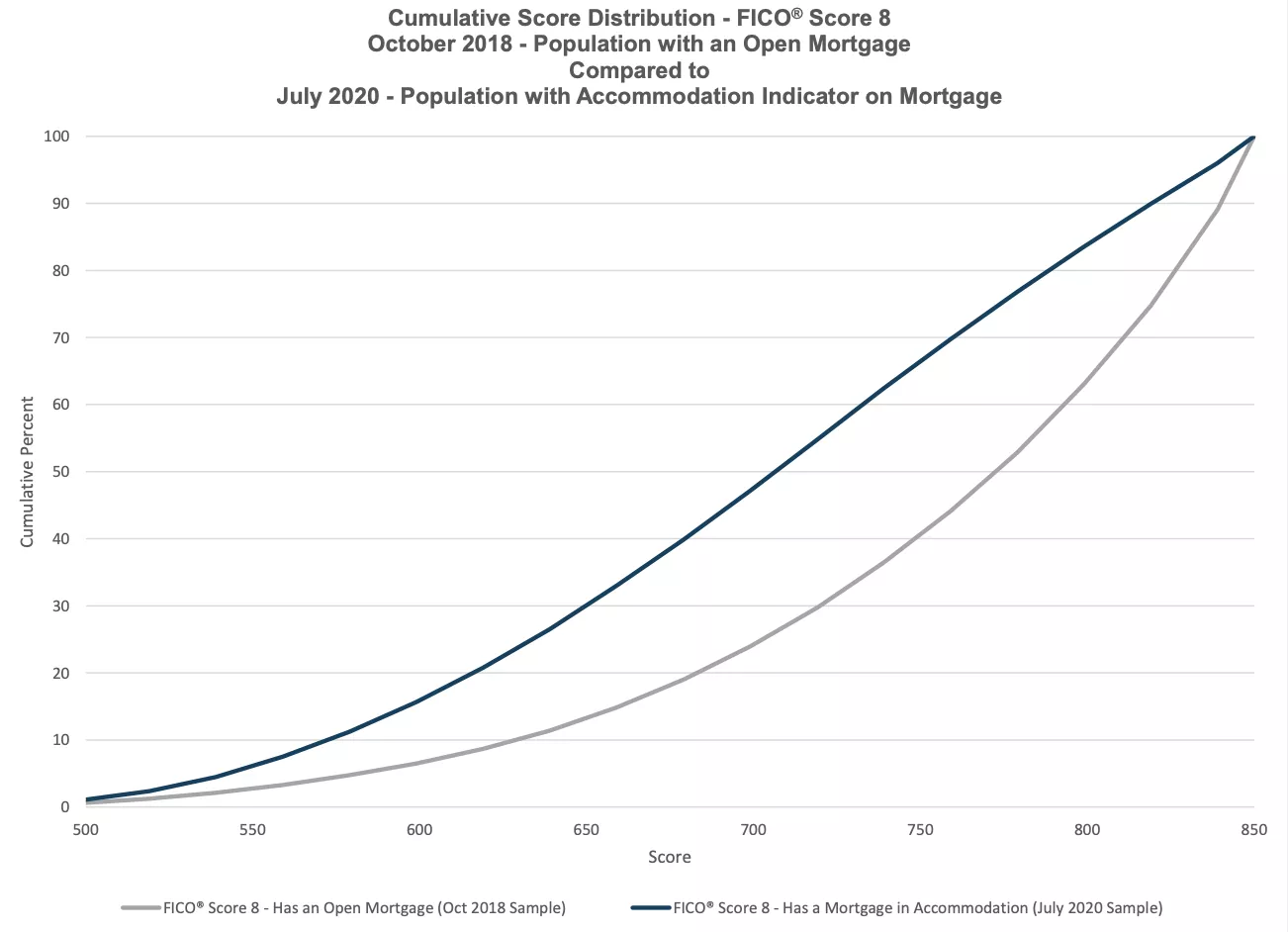

The results on this simulation are generally similar to those shown from the earlier analysis in terms of score shifts. As shown in Figure 1, the mortgage borrowers who are in accommodation as of July 2020 tend to have higher total mortgage balances compared with the overall mortgage population. Therefore, the impacts to their FICO® Scores were somewhat larger because the simulated balance changes resulting from the suspension of payments were larger. The main difference between these two studies, as shown in Figure 2, is that the affected population in this study is shown to be much lower scoring than the population of all consumers with open mortgage accounts that was used in the initial study. This finding is in-line with external findings that there is an inverse relationship between consumer’s FICO Scores and their likelihood to have pursued/received forbearance during COVID-19.

Figure 1

Figure 2

Population Used in Analysis

This analysis used a representative national sample of millions of U.S. consumers taken from July 2020 and identified those mortgages that were indicated as being in accommodation. Mortgages in accommodation were identified using logic that included the presence of codes indicating forbearance or deferred payment. The percentage of consumers who had a mortgage identified as being in accommodation out of all consumers having an open mortgage account was 5.8%. Figure 2 shows that the population indicated as being in accommodation has a much lower FICO® Score distribution than the total mortgage population analyzed on the October 2018 sample.

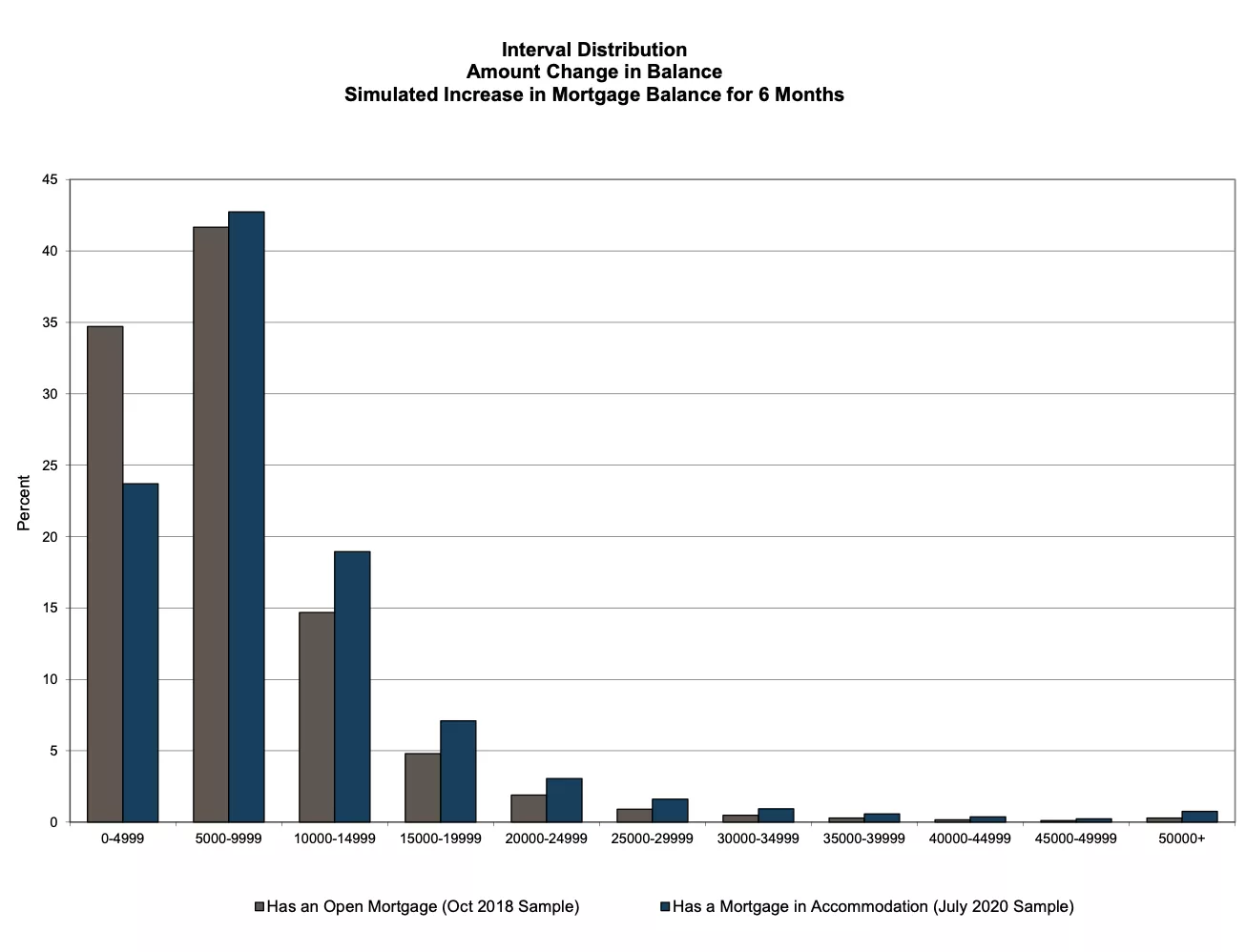

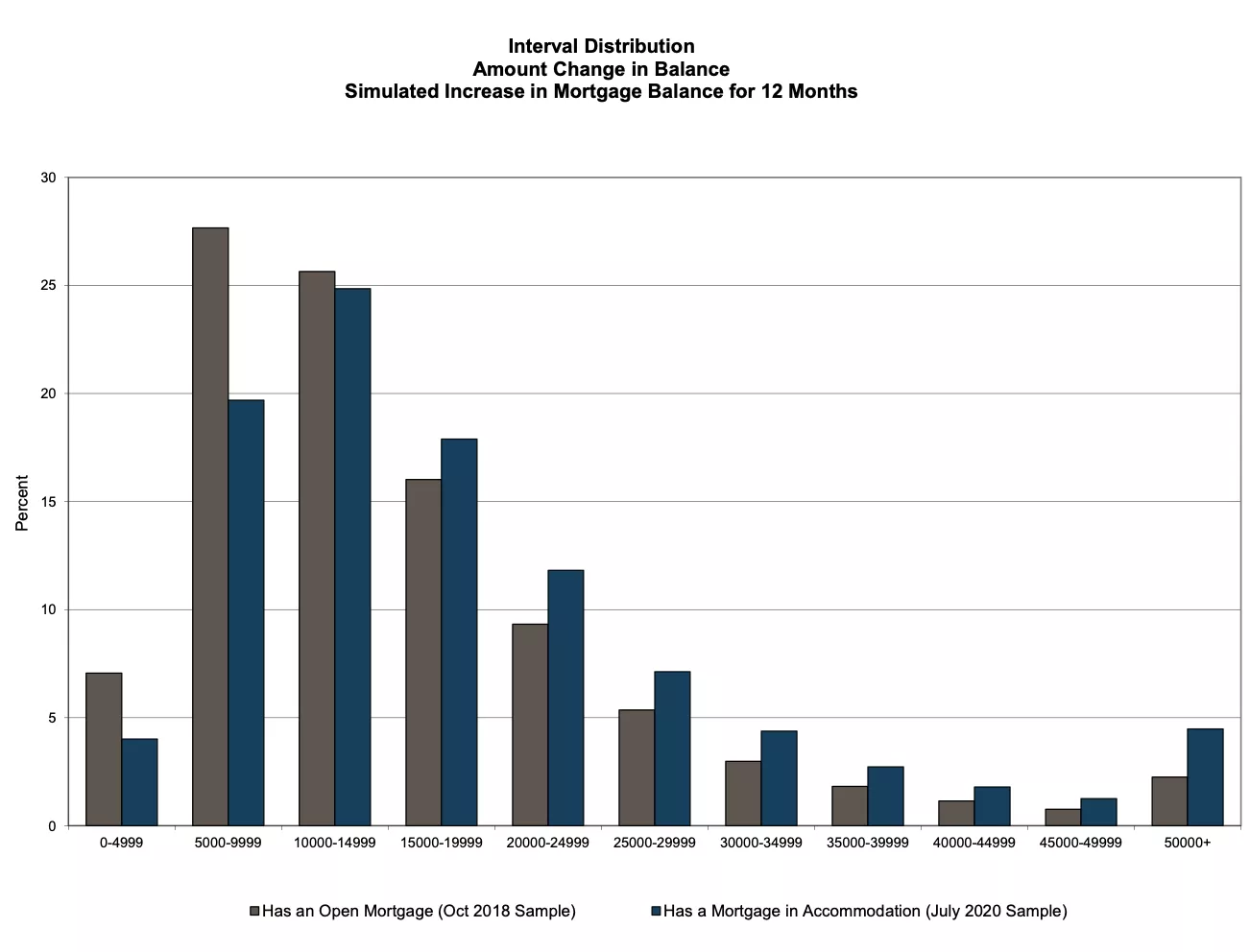

Last time, we described the logic for simulating the imputed balance change: balances were estimated to aggregate in the amount of 80% of the total scheduled monthly payment amount per month. Figure 3 shows a comparison of the imputed balance changes over six months of accommodation between the two populations, and Figure 4 shows the same comparison over 12 months.

Figure 3

Figure 4

The distributions of the balance changes over six and 12 months are generally higher on the population that has a mortgage in accommodation. We see higher percentages for this population in all of the balance change ranges above $5,000 over the 6-month simulation, and higher percentages in all of the ranges above $15,000 over the 12-month duration. The higher distribution of imputed balance change on the accommodation population is due to balances being higher at the onset of this balance aggregation simulation, as we saw in Figure 1. The average mortgage balance of the mortgage population that was in accommodation as of July 2020 was $273,000 compared with an average mortgage balance of the total mortgage population observed on the October 2018 data being $209,000.

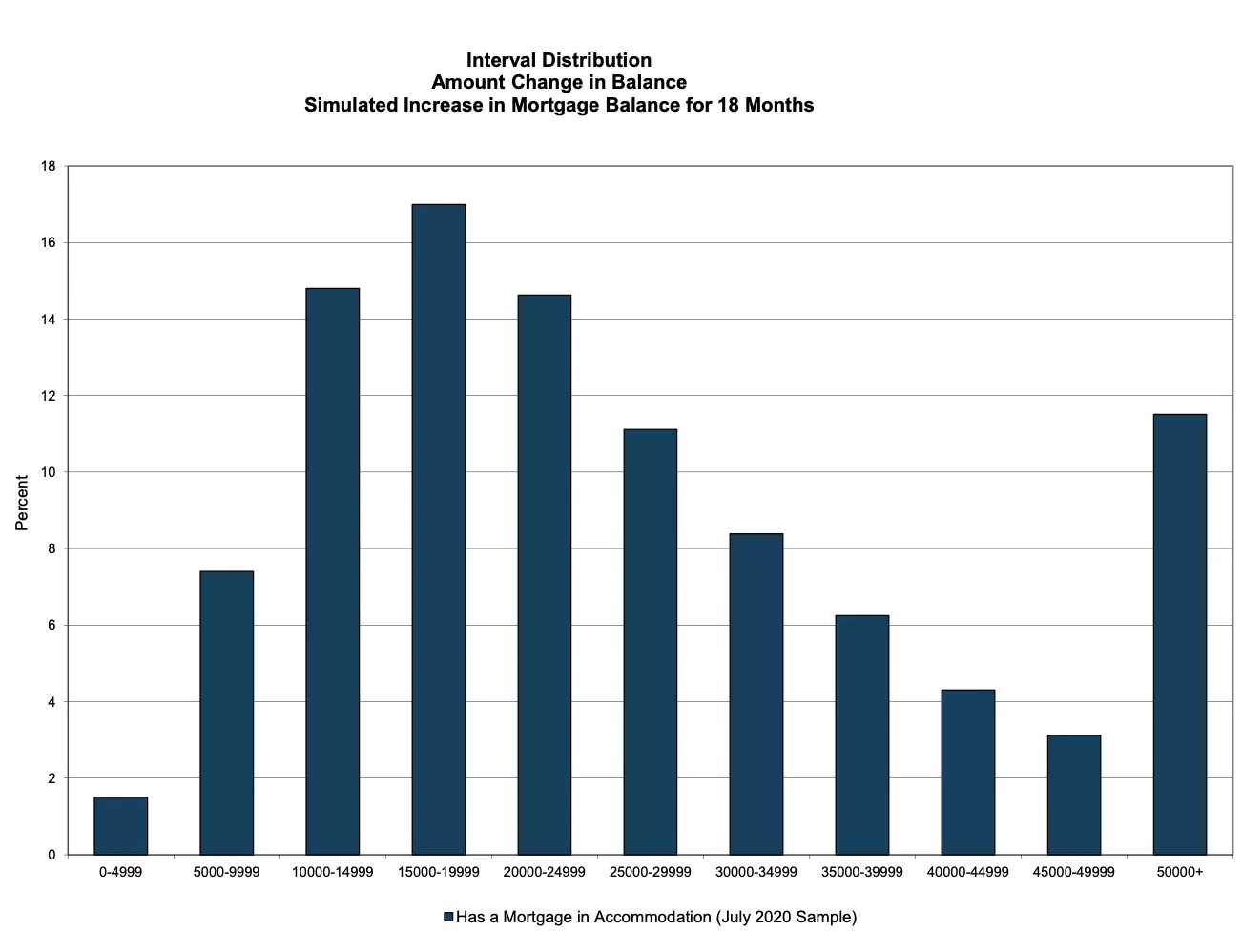

Figure 5 shows the distribution of the imputed balance change on the July 2020 sample (the equivalent analysis was not conducted on the October 2018 sample). By design, the change in balance over 18 months is three times the change in balance over six months.

Figure 5

Impacts to FICO® Score 8

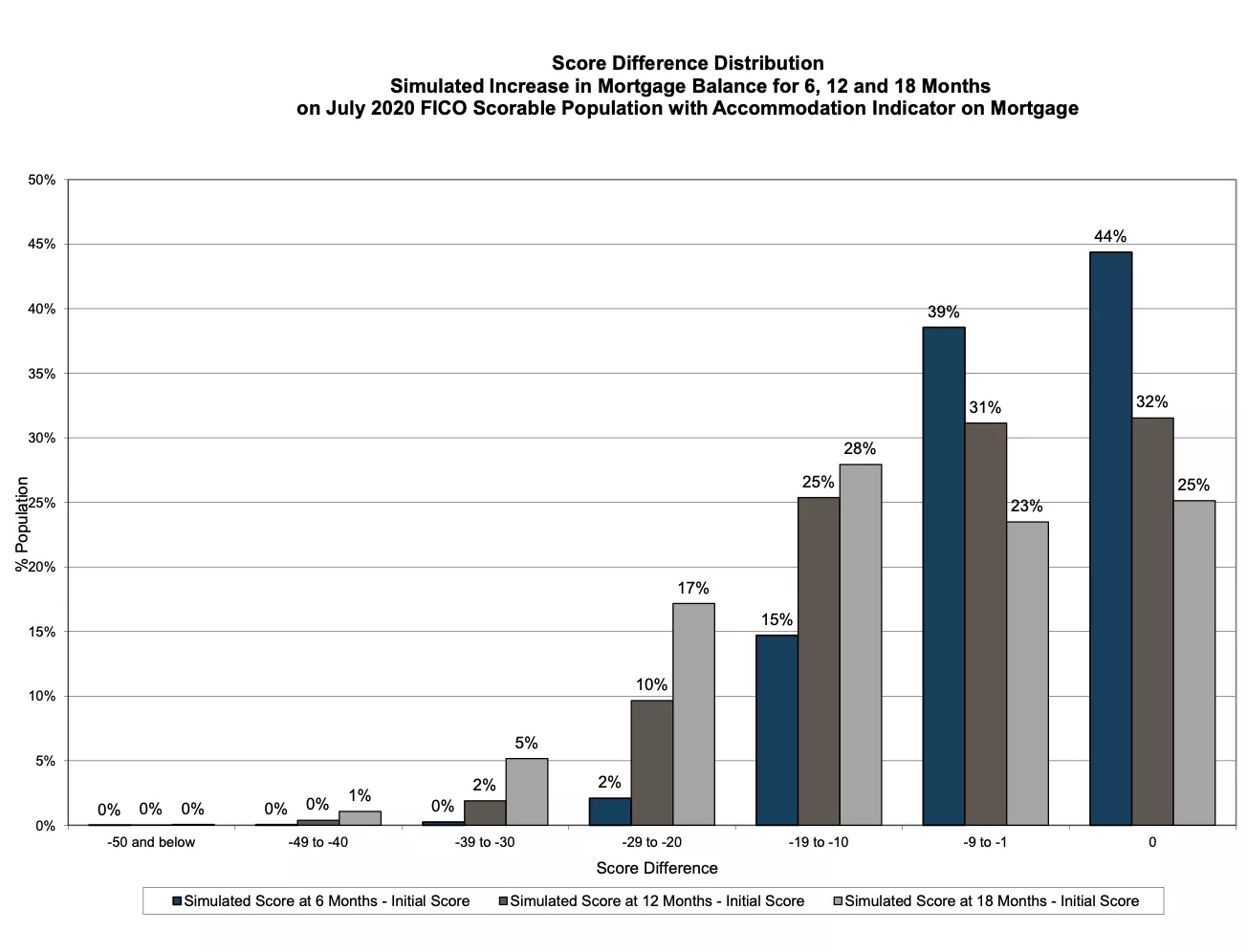

As shown in Figure 6, over 6 months of deferment, 44% of FICO® Scores didn’t change in this simulation, 39% decreased by 1-9 points, 15% by 10-19 points, and 2% decreased by 20+ points. The average score change after 6 months was -4.4 points. Among those scores that changed, the average score change was -7.8 points.

Over 12 months of deferment, 32% of FICO® Scores didn’t change in this simulation, 31% decreased by 1-9 points, 25% by 10-19 points, and 12% decreased by 20+ points. The average score change after 12 months was -8.3 points. Among those scores that changed, the average score change was -12.1 points.

In the 18-month simulation, 25% of FICO® Scores didn’t change, 23% decreased by 1-9 points, 28% by 10-19 points, and 23% by 20+ points. The average score change after 18 months was -11.7 points. Among those scores that changed, the average score change was -15.6 points.

Figure 6

The following table compares these stats with those observed on the broader mortgage population from the previous report, showing that the changes are modestly more pronounced on the recent accommodation population.

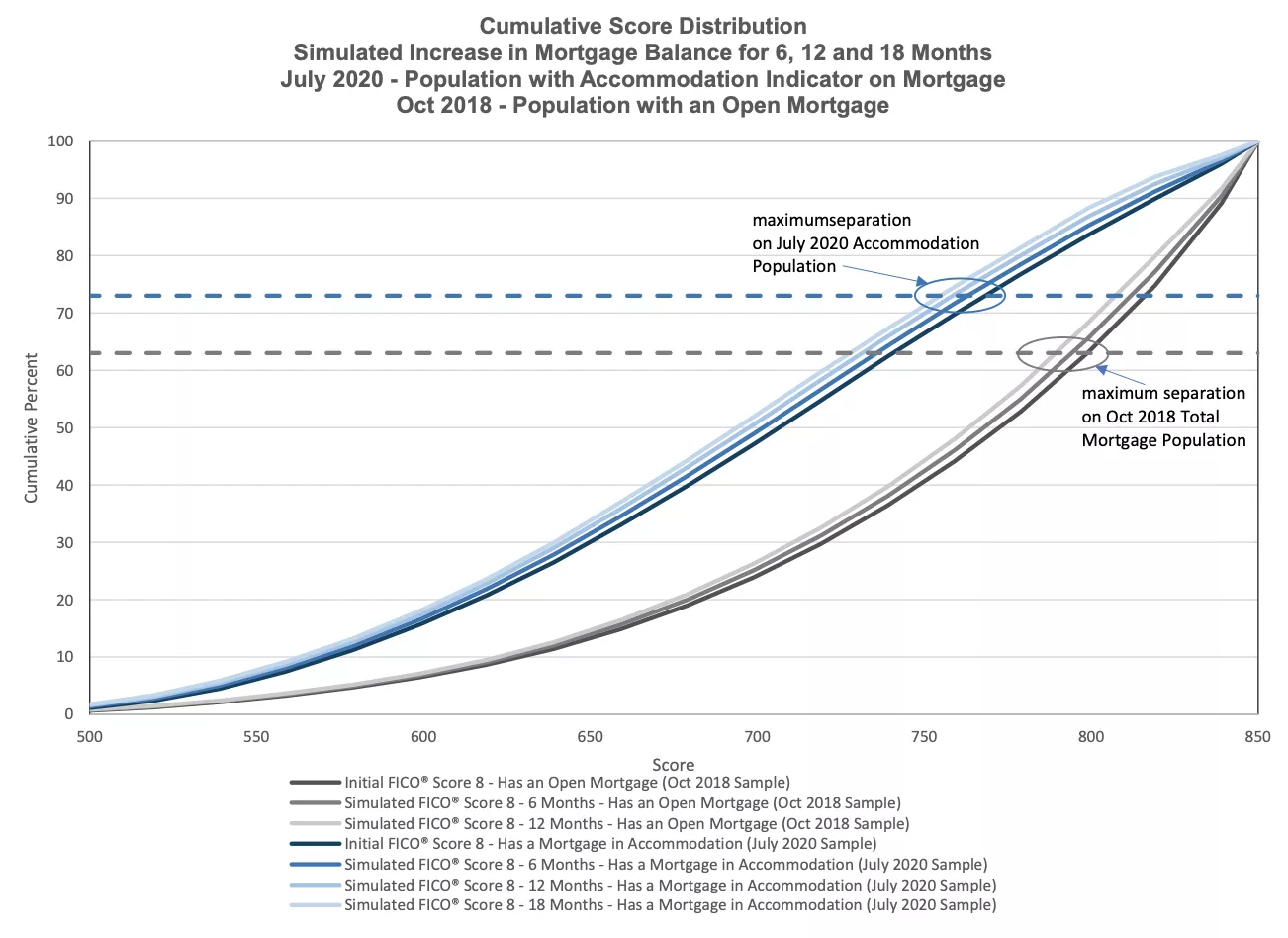

On a cumulative score distribution view (Figure 7), we see the downward shifts over six months, 12 months, and 18 months on the July 2020 accommodation population, as we did on the October 2018 total mortgage population. The score distributions on the July 2020 population are much lower, but the magnitude of the shifts is similar. The magnitude of maximum separation is a downward shift of approximately 5 points after six months of deferment, 10 points after 12 months of deferment and 14 points after 18 months, occurring in FICO® Scores in the mid 700s. We observed similar maximum shifts on the 2018 data at around the 790s.

Figure 7

As the previous analysis highlighted, the impacts to FICO® Scores from imputed balance increases associated with accommodation programs are generally modest. The latest simulation results based on actual mortgages reported as being in accommodation as of July 2020 show the impacts to be similarly modest.

As a reminder, the indication of payment accommodation does not in itself result in any impact to the FICO® Score. Accommodation can be an important way for consumers to get through a period of hardship. These results should provide some degree of reassurance to both lenders and consumers alike who are concerned about potentially substantial adverse impacts to FICO® Scores resulting from a request for mortgage payment accommodation.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.