UK Cards Data: September Data Shows Rising Consumer Stress

The FICO Credit Market Report for September shows a drop in spending and includes an increase in missed payments as cost-of-living pressures take hold

With the rise in inflation and soaring energy costs in the UK, it’s no surprise that our data on UK card trends for September 2022 offer clear signs of consumer indebtedness. These include:

-

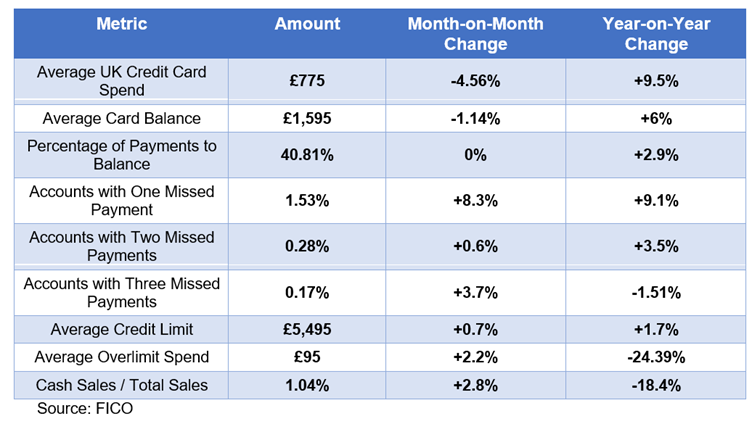

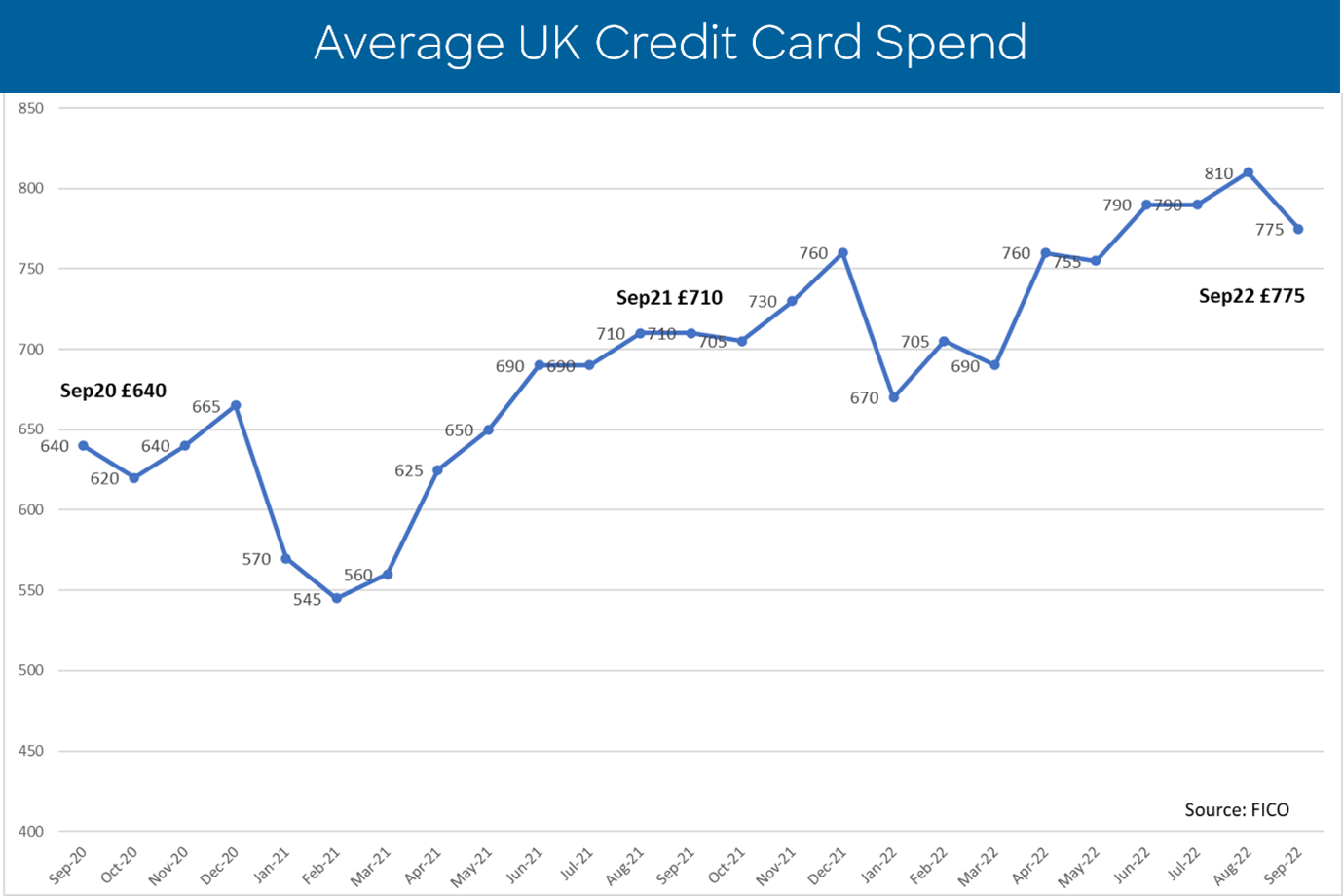

Average total sales were £775 – 4.56 per cent lower than August

-

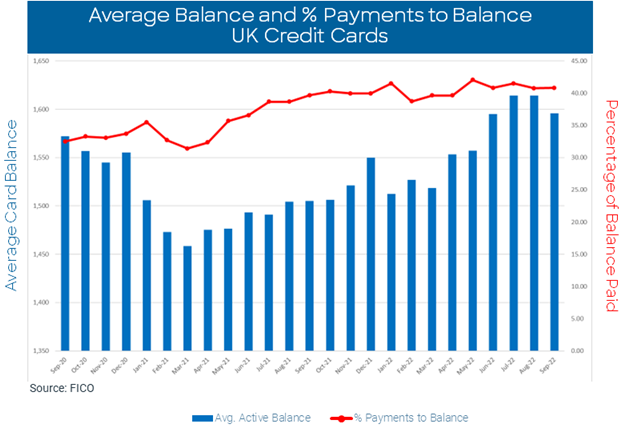

The average active balance also dropped in September to £1,595 – 1.14 per cent lower than August and reversing the upward trend seen over the previous 18 months

-

Customers missing one payment increased by 8.3 percent compared to August and 9.1 percent this time year-on-year

-

Accounts with two missed payments increased marginally month on month — by 0.6 per cent — but those missing three payments increased by 3.7 per cent compared to August

Veteran credit card accounts — those that have been open for a time of five years or more and which are normally considered low-risk by lenders — have shown an increase in the average balance where they have missed two or more payments. This will be a concern for credit card providers.

The percentage of cardholders missing one-time payment is also rising, although, overall, the average balance for customers missing two payments is trending downwards. This suggests that lenders have already taken targeted activity earlier in the year to help customers who have missed one payment to avoid the debt escalating. This targeted activity will be critical now as the numbers of cardholders missing one payment increases.

Another indicator of consumers reining in spending includes the total average sales on credit cards. This dropped in September, in contrast to the summer months.

There is, however, another worrying trend in the percentage of payments to balance. Cardholders are starting to pay less than earlier this year, perhaps suggesting they are no longer able to rely on pandemic savings. The percentage of accounts paying the full balance has also decreased for the last three months, which may be a reflection that customers are now not able to make the full balance.

Lenders can use segmentation analysis on their portfolios to ensure that their web and mobile applications encourage consumers in distress to make contact at the first indications of difficulty, and to consider establishing special payment plans for those struggling to stay on top.

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service produced by FICO® Advisors, the business consulting arm of FICO. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80 percent of UK card issuers.

How FICO Can Help You Manage Credit Card Risk and Performance

-

Work with our FICO Advisors team

-

Explore our solutions for credit line management and collections prevention

-

See my post on UK Credit Card Trends: From 2008 Crash to Cost-of-Living Crisis

-

Read more posts on UK cards

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.