3 Ways Spanish Banks Can Stop Fraud with Customer Communications

As bank fraud increases and more customers fall victim to scams, banks in Spain need to enhance fraud protection but not at the risk of damaging customer experience

According data from Spanish banks, fraud attacks increased by 117% in 2023, reaching recorded losses of €250 million. These increases spanned a variety of different fraud types, including ATM fraud, debit card fraud and fraud in bank transfers. Spanish banks are paying attention and have made positive moves to share data and tackle fraud through the establishment of FrauDfense. However, the rapid rise in fraud losses means there is more that banks should do to protect themselves and their customers.

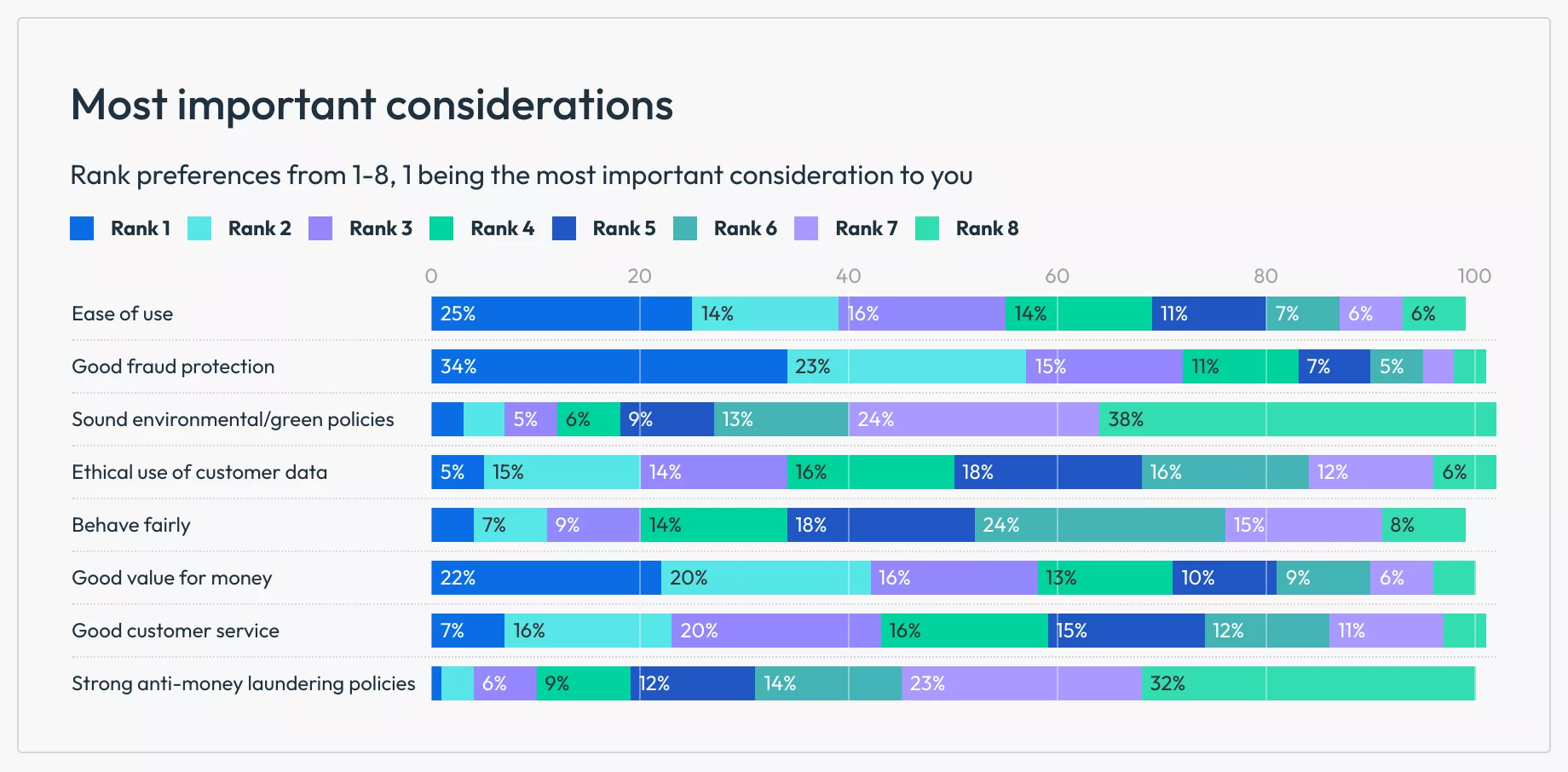

Regardless of the type of fraud banks face, they share one crucial element – the customer. Whether it’s through education, better processes or improved interactions, putting customers at the heart of fraud prevention is vital – and it matters to them. A December 2023 survey by FICO found that having good fraud protection was a deciding factor for the Spanish when selecting a new bank account. 34% said it was their number one consideration and 72% listed it as a top three consideration.

Banks that are perceived as unable to safeguard customers not only face fraud losses but will struggle to attract and retain customers. While customers want great fraud protection it can’t come at the expense of customer experience. Our survey revealed that 19% of Spanish respondents have reduced use, or stopped using their personal bank account because identity checks were too difficult or time consuming; 18% have taken similar actions with credit cards.

Communicating with customers has always been a core competency for banks but in the context of fraud why is it so important?

1. Communication helps to prevent more fraud

Customer communications that are tightly integrated with the fraud prevention process can go a long way in helping prevent fraud. Essentially you can recruit your customer to be part of your fraud department. Rapid intervention when fraud is suspected can help confirm fraud and stop a transaction, but this communication must be delivered so that a customer responds. Not all customers like or have access to the same communications channels, so a fraud solution that can adapt to customer preferences and needs is vital. At FICO we’ve seen many scenarios where flexible, two-way, and multi-channel communications’ strategies have prevailed in fraud prevention.

- In a card fraud scenario where transactions appear suspicious, contacting a cardholder as soon as possible is vital to determine if card activity is legitimate, or due to card theft or account takeover. The ability to automate this process so that customers are contacted immediately, using their channel of choice, and attempts to contact can be repeated until successful, accelerates confirmation of a fraud. Cards can then be blocked and re-issued before additional fraudulent transactions occur.

- When money is sent using P2P apps or online banking there is a growing risk of scams or authorised push payment fraud. When people have been tricked into sending money to a fraudster, for example due to a romance, bank impersonation, or investment scam, intervention is vital to break the fraudster’s spell. Too often banks and apps rely on generic message “pop-ups” warning of scam risk, but these messages are so general and ubiquitous that they do not resonate and are easily clicked-through.

We have seen significant success when banks use customer communications capabilities to deliver highly relevant messages to customers that are tailored to the customer and the potential scam transaction. By sending multiple messages in a thoughtful manner, banks see their customers more frequently stop the transaction or request to speak to the bank’s scams specialist. Even when a customer has ignored initial messages, when properly presented and worded a third or even fourth message is cutting through the scammer’s deception and successfully alerting the customer.

2. Communication enhances the customer experience

Customers undoubtedly want good fraud protection; however, they expect it to come without the downsides of extra effort or a poor experience for them. When good customer communications protocols aren’t in place two issues occur:

- The management of false positives becomes a bad experience. There is a wide grey scale between obvious fraud and obvious non fraud. While effective fraud analytics and transaction monitoring can reduce the number of doubtful cases, there will always be incidents that require further investigation. In many of these cases a customer is attempting to legitimately carry out a transaction or apply for an account. Frequently, determining if a case is fraud requires more information from the customer. By using communication capabilities that are integrated with case management, your customer outreach can be automated and responses can be managed for faster and less disruptive case resolution.

- Necessary fraud prevention processes ruin customer experience. When transactions occur or new customers are onboarded, fraud prevention is vital but in many cases the customer is required to prove their identity to prevent fraud. Disrupting the customer experience with checks that are lengthy, intrusive, and difficult to respond to causes customers to stop using their accounts or abandon opening new accounts. The FICO survey shows that up to 20% of Spanish respondents say they have abandoned opening an account because of difficult or time-consuming checks.

By using customer communications capabilities to inform customers about what is needed and why, collect necessary information and respond to questions, the inconvenience of fraud checks can be minimized.

3. Communication improves operational efficiency and cuts cost

Managing the fraud resolution process can be lengthy and complex, particularly when a customer is making a claim to be refunded. Having a representative respond to each of the numerous customer interactions is time-consuming and costly. However, a streamlined, self-service based, omnichannel communications approach integrated into your fraud claims strategy can help you reduce operational expenses.

In a traditional fraud case each step of the fraud claims lifecycle — from the initiation of the case, to completing forms, to attaching additional information, to sending that information back to the financial institution’s system, to the follow-up communications — requires manual input by fraud prevention or customer management teams. With the right technology, all of these can be automated. No more need for costly and cumbersome mailing of forms and letters either — customers can now receive status updates throughout the entire process. This not only gives them peace of mind but removes their propensity to want to speak to an agent. Inbound call avoidance is key to unlocking significant savings for your organization.

How FICO Helps You Communicate More Effectively to Stop Fraud

FICO’s customer communications capabilities offer an intelligent, automated, two-way communication solution that allows real-time communication with consumers using voice, SMS, mobile applications, email, social media, and other channels. Tightly integrated to FICO’s market-leading fraud detection for card fraud, payments fraud and application fraud, it is a vital part of end-to-end protection that stops more fraud and enhances customer experience.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.