Is £90 Billion in Unused Exposure on UK Cards a Problem?

With over £40 billion of unused exposure on inactive UK cards and over £50 billion on active UK cards there is the potential for huge losses if consumers start to eat into these li…

I have commented on the worrying trends for New and Veteran UK cards, based on our analysis of delinquency trends in UK cards, however, there are further indications that Veteran accounts, traditionally the lowest-risk segment, are also starting to show signs of stress.

Veteran accounts matched their highest average amount overlimit value in the last two years. There are opportunities for issuers to identify the highest high-risk overlimit accounts for treatment to improve roll rates into delinquency and potentially IFRS 9 provisioning.

The Veteran average amount overlimit may not initially appear as a potential red flag, but when you consider that, at £5,749, average credit limits for this segment are at their highest since at least January 2002, there are possibly some very high balance overlimit accounts that can roll into delinquency. The last time limits were anywhere near this level was in July 2008, when the average was £5,675. They were just £3,963 in January 2002.

With over £40 billion of unused exposure on inactive UK cards and over £50 billion on active UK cards there is the potential for huge losses if consumers start to eat into these limits. Although the percentage of unused credit on active accounts is decreasing, issuers need to be confident that the uplift in utilisation is on the right accounts.

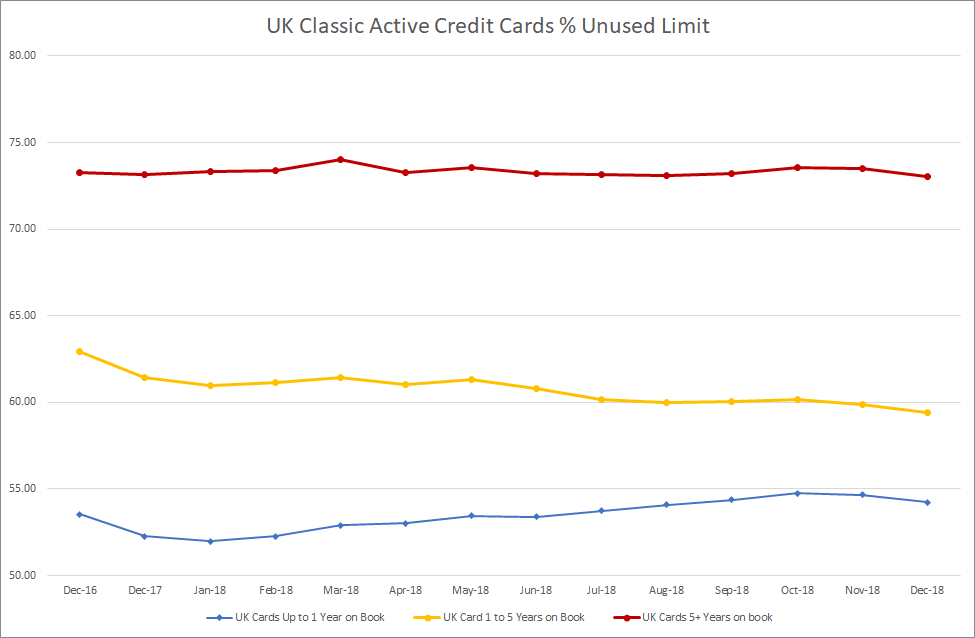

Issuers will assess affordability metrics when deciding whether to offer a line increase, but there may be a gap in the assessment process in relation to future spend within their limit, for accounts that do not qualify for an increase. These include accounts with high limits that no longer receive increases, as they exceed the maximum for that product or have requested no further increases as well as those that marginally miss out on qualifying. Consider that 73% of exposure on Veteran active cards is unused, and limits are growing. Issuers could consider performing an evaluation of profitability “corrosion” due to unused limit on their portfolios.

The Unused Exposure Problem

The average balance of UK cards with limits £5,001 to £9,999 is only £1,429 and for those with limits >£10,000 it is £2,621. Can issuers be sure at this point that if their customers were to spend this extra £3,572 to £8,570 that they could afford the jump in repayments, especially if it was over a short period of time?

There is an opportunity for issuers to assess on a regular basis to determine if these consumers can still afford a significant increase in their balance and if not adjust accordingly.

Due to the high levels of unused exposure, learnings from the last recession and introduction of IFRS 9 regulations (whole limit not just balance included in the calculation), it was anticipated that issuers would start to decrease limits on inactive, low-utilised and high-risk accounts. However, there has been minimal adoption, potentially due to the concern around customer perception, although reducing limits can be described as responsible lending. If Issuers are concerned about customer reaction, campaigns could be undertaken on a small proportion to understand the response, before rolling it out as a standard business as usual policy.

Watch for our review of the first quarter 2019, which will show the impact of the high Christmas spend on delinquency results.

To learn more about our cards benchmarking service, or FICO’s new Risk Benchmarking Service which forms part of the Fair Isaac Advisors P&L Insight Service, please contact me at staceywest@fico.com.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read more

Average U.S. FICO Score at 717 as More Consumers Face Financial Headwinds

Outlier or Start of a New Credit Score Trend?

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.