Canada Bankcard Industry Benchmarking Trends: Q1 2026

Credit card data shows Canadians are carrying higher balances and paying down less of their monthly debt

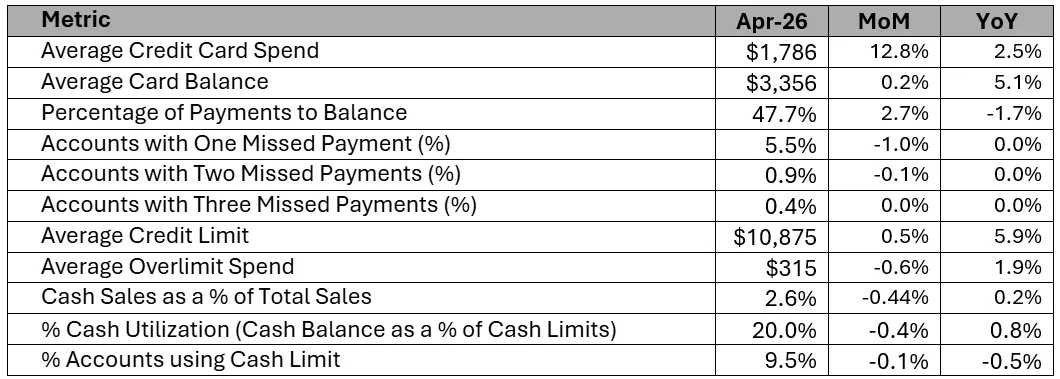

As we close out the first quarter of 2026, the Canadian credit card landscape continues to show resilience, with all delinquency rates remaining stable and average spend increasing to $1,786 in April — a healthy 2.5% year-over-year increase from April 2025.

However, a closer look reveals a few trends that merit attention: the payments-to-balance rate has eased to 47.70% from a peak of 53.02% in early 2025, while average balances have gradually climbed 5.1% year-over-year to $3,356. While there is no immediate concern, together they suggest consumers are slowly carrying more debt and paying it down at a more modest pace — trends that are worth keeping a close eye on as we head into the latter half of 2026.

Key Trend Indicators Canadian Cards – end of April 2026

Highlights of Canada Card Data Patterns

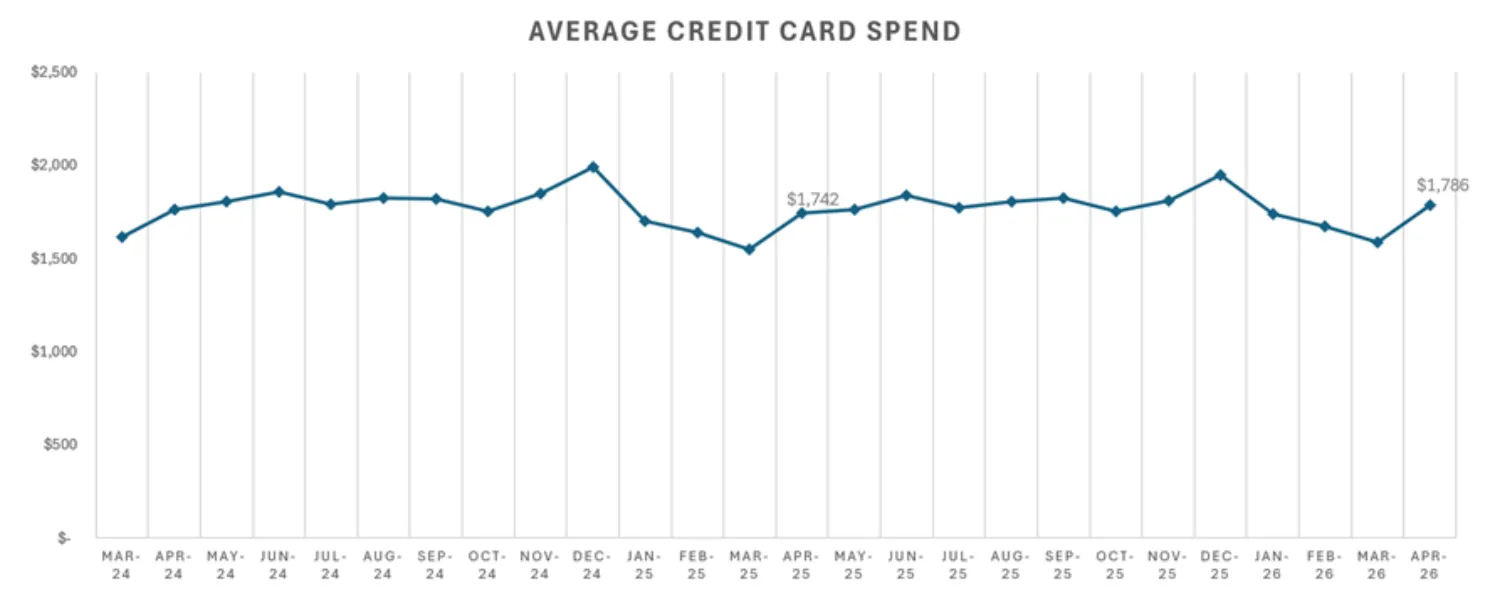

Spending is recovering but remains under pressure

Average credit card spend shows a clear seasonal pattern — peaking around December and dipping in March, reflecting the typical post-holiday pullback. The April 2026 figure of $1,786 is up 2.5% year-over-year, suggests reasonable spending growth relative to the increase to cost-of-living (CPI increase to 2.8% year over year in April 2026 Source: statscan.gc.ca).

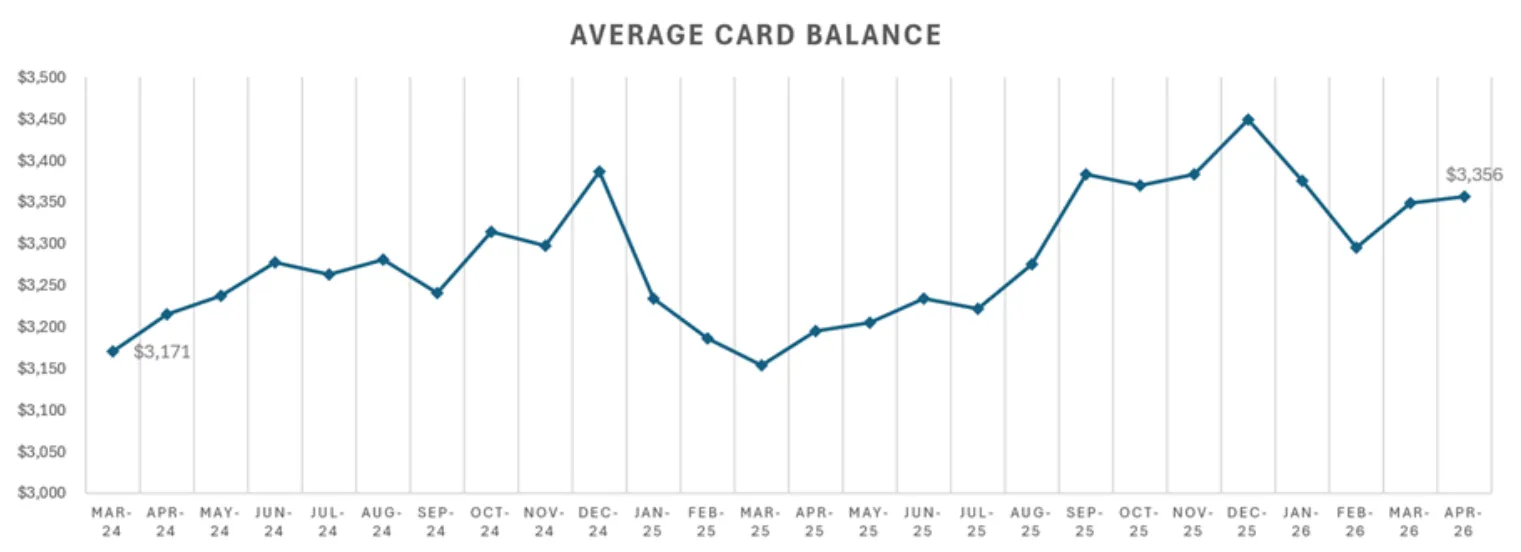

Balances are growing steadily

Average card balances have climbed from $3,171 in March 2024 to $3,356 in April 2026 — a 5.1% year-over-year increase and a 5.9% increase over the last two years. This suggests consumers are increasingly carrying more debt, which may reflect the ongoing cost-of-living pressures or a greater reliance on credit for everyday expenses.

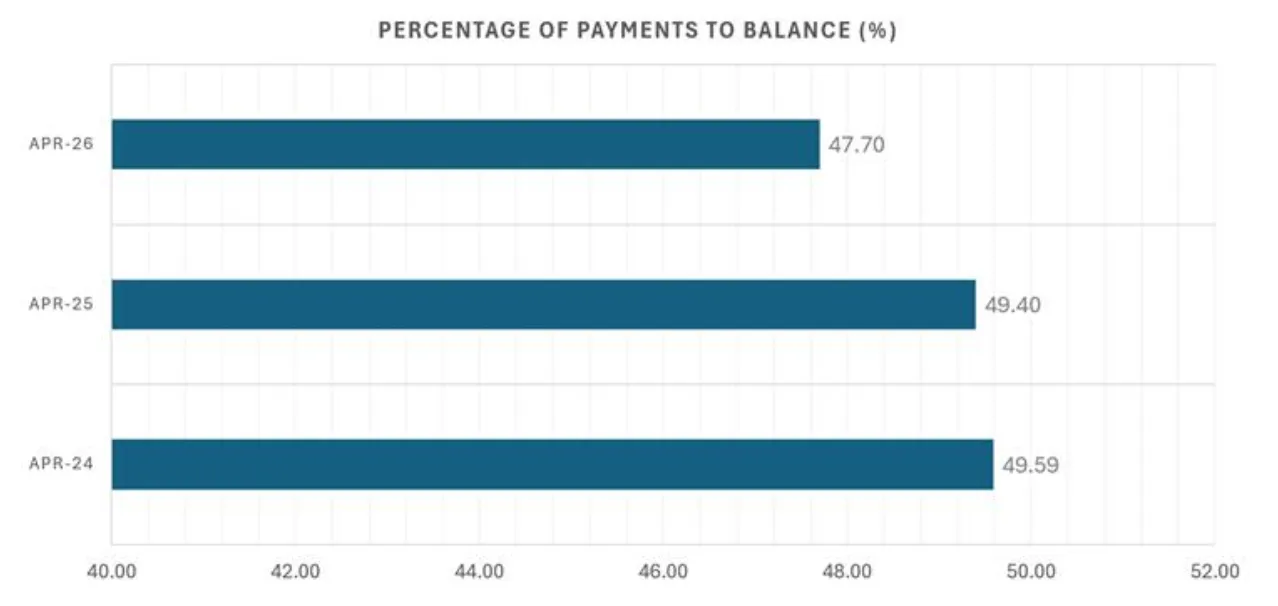

Repayment rates are slipping

The percentage of payments to balance has declined from a peak of around 53% in late 2024 to 47.7% in April 2026, which is a notable drop of 1.7 points year-over-year. This is a meaningful signal that consumers are paying down a smaller share of their balances each month — consistent with the rising balances trend above.

Delinquency is relatively stable, but worth watching

Accounts with one missed payment sit at 5.50% in April 2026, flat year-over-year. Two and three missed payment rates are similarly stable at 0.91% and 0.44%, respectively. While not alarming, these figures should be monitored closely given the deterioration in repayment rates.

Credit limits are expanding

Average credit limits have grown 5.9% year-over-year to $10,875, which could reflect lenders proactively increasing limits or consumer demand for more credit availability. This may also be contributing to the higher balances being carried.

Cash usage is ticking up

Cash utilization is ticking up slightly by 0.8% for the accounts that are using cash, but overall accounts using cash limits has decreased by 0.5%.

Overall takeaway: The data paints a picture of a Canadian credit card consumer who is spending modestly more, carrying higher balances, and paying them down less aggressively. Delinquency hasn't materially worsened, but the combination of rising balances and falling repayment rates suggests that credit risk could build if economic conditions don't improve.

Implications and Considerations for Risk Managers

Repayment Rate (Payments to Balance %)

Monitor monthly readings closely and consider setting a threshold alert for example if the repayment rate falls below 45% for two consecutive months, as this may signal accelerating consumer stress

Review collections treatment and communication channels now to ensure customers struggling with affordability receive appropriate pre-delinquent support and are on the right credit product

Average Card Balance

Assess whether credit limit increases are being extended to segments already showing repayment behaviour changes or challenges, and consider tightening limit growth policies for higher-risk cardholders

Stress-test loss rate assumptions against a scenario where balances continue to grow while repayment rates remain depressed

Early-Stage Delinquency

Review existing pre-delinquency and early-stage collections strategies and track month-over-month directional changes

Consider setting an internal watch level to trigger early intervention strategies before stress migrates to later delinquency stages

Ensure collections staffing and early hardship programs are adequately resourced ahead of any potential uptick

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 90% of Canadian card issuers.

For more information on these trends, contact FICO.

How FICO Can Help You Manage Credit Card Risk and Performance:

Explore our solutions for customer management.

See my previous posts on CA card performance.

Make more informed and profitable decisions with FICO’s Scoring Solutions.

FICO and TRIAD are registered trademarks of Fair Isaac Corporation in the United States and other countries.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.