Canada Bankcard Industry: A Look Back at Q4 2025 Trends

FICO risk benchmarking data covering roughly 90% of card transactions in Canada reveals a market at an inflection point - improving delinquencies mask structural shifts in payment

The Big Picture: Surface Stability, Underlying Strain

As we reflect back on 2025, the Canadian credit card market presented an interesting paradox. Delinquency rates improved meaningfully across both bank and monoline segments, with the late 2024 postal strike disruption now fully resolved. Yet beneath these encouraging headlines, payment capacity is eroding at an accelerating pace - and for the first time in our four-year dataset, the average bank card holder is paying less than half their monthly balance.

This isn't a crisis. But it represents a fundamental shift in how Canadians manage credit card debt, with implications for household wealth and financial resilience heading into 2026.

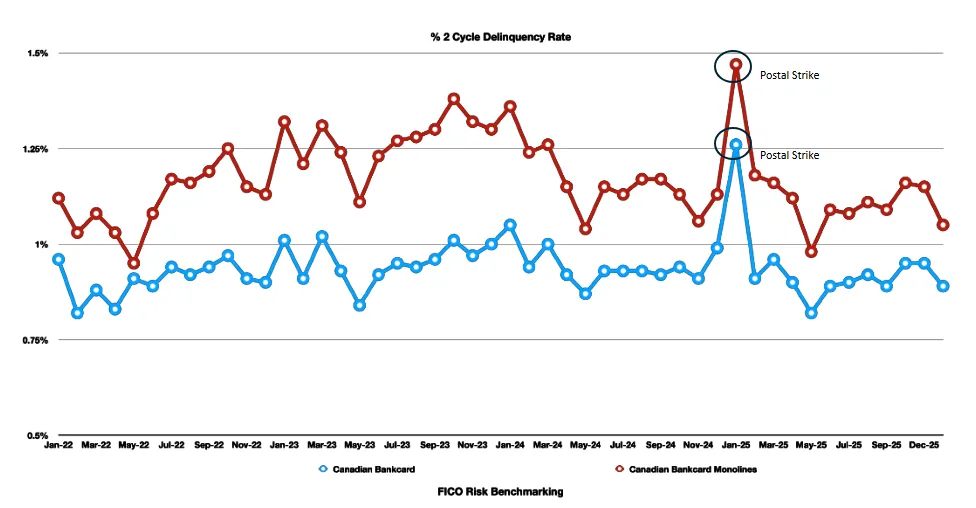

The Good News: Delinquencies Normalized After Postal Strike Disruption

The late 2024 Canada Post strike created temporary distortions across credit card metrics. Consumers relying on mail-based payments experienced delays, pushing delinquency readings artificially higher through November-December 2024 and into January 2025 - when Bankcards hit 1.26% and Monolines reached 1.47%.

These elevated readings reflected payment processing disruptions rather than genuine credit deterioration. As the strike resolved and payment channels normalized, the market self-corrected quickly.

By December 2025, bank card delinquencies fell to 0.89%, the lowest December reading since 2022. Every vintage improved. Monolines followed suit, dropping to 1.05% - better than three years ago.

This recovery confirms that the late 2024/early 2025 spike was an operational anomaly rather than systemic credit stress. The underlying health of the portfolio remained intact throughout the disruption.

The Concerning Trend: Three Years of Payment Capacity Erosion

While the postal strike explains the delinquency spike, it doesn't explain the longer-term deterioration in payment behavior. This trend spans the entire three-year observation period and has continued through 2025.

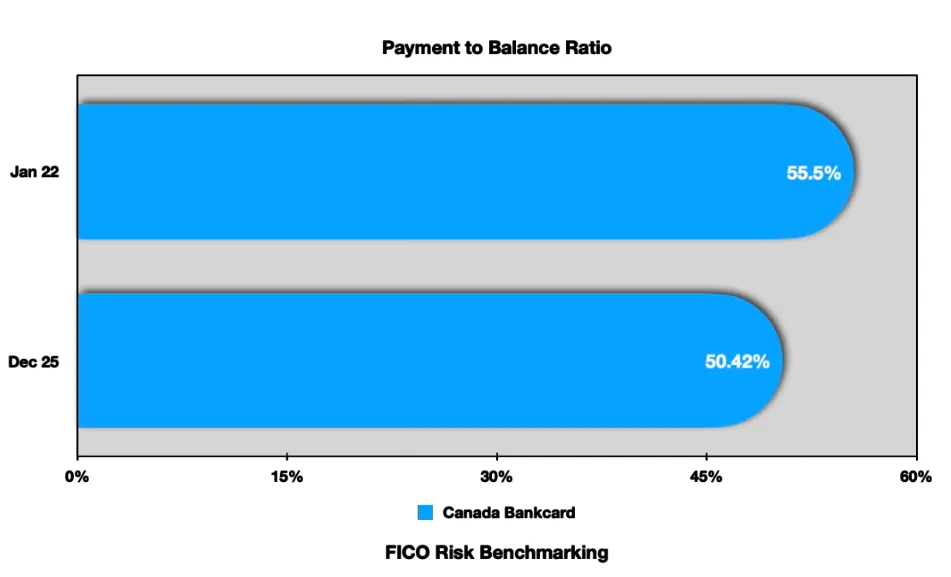

Bank card payment ratios declined from 55.5% in December 2022 to 50.4% in December 2025 - a five-percentage-point erosion over three years. That drop crosses an important threshold: the typical consumer is now in "balance accumulation mode" rather than "paydown mode."

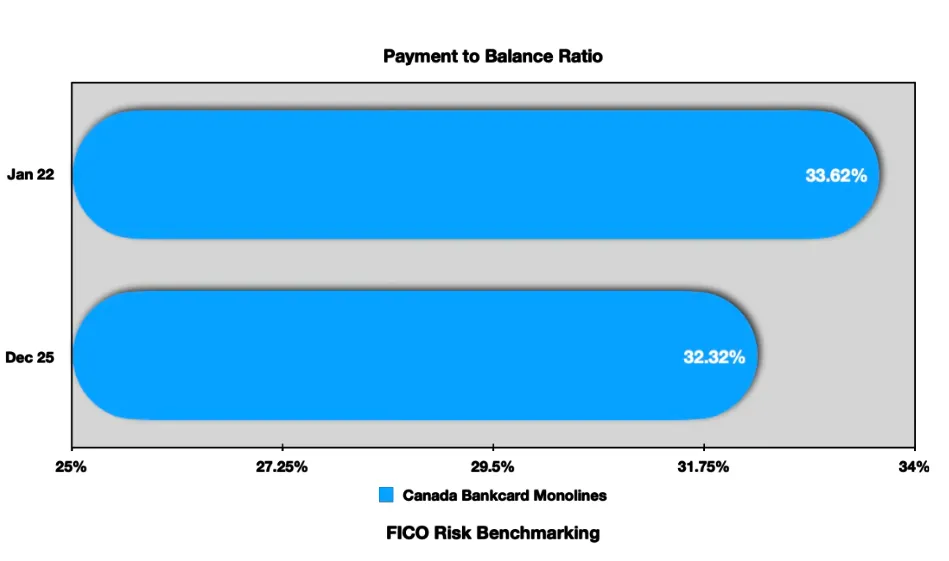

The monoline segment shows a more nuanced three-year picture. Overall payment ratios declined modestly from 33.6% to 32.3% - a manageable 1.3-point decline. However, the composition reveals stress:

New accounts (<1 YR) dropped from 43.9% to 37.2% over three years (-6.7 points), with most of that decline concentrated in 2025

Established accounts (1-5 YR) fell from 33.4% to 29.9%, breaching the critical 30% threshold

Veteran accounts (5+ YR) remained remarkably stable, declining just 0.1 points from 33.0% to 32.8%

The stability among veteran monoline customers is encouraging - it suggests that consumers who successfully navigate the credit-building phase develop sustainable payment habits. The stress is concentrated among newer and mid-tenure accounts still establishing their financial footing.

A Tale of Two Segments

The divergence between bank cards and monolines has become stark.

Bank card holders remain fundamentally healthy despite behavioral shifts. With the postal strike distortion removed, delinquencies show clear improvement year-over-year. Utilization stayed stable at 29%, and credit limits continued expanding (+7.5% for new accounts). These consumers have financial cushion.

Monoline customers face different pressures. While overall delinquencies improved once strike effects normalized, new account balance delinquencies actually worsened - the only segment deteriorating year-over-year on an underlying basis. Payment ratios collapsed across new and established vintages. Utilization ticked up nearly two percentage points.

The credit response reflects this divergence. Bank issuers kept expanding limits. Monoline issuers pulled back sharply in early 2025, with new account limits falling 10% from their November-December 2024 peak before stabilizing.

The credit limit gap between segments widened by nearly $700 over three years. A mid-tenure monoline customer now accesses almost $2,000 less credit than a comparable bank card holder - up from just $800 in 2022.

We're watching a two-tier credit market emerge. Mainstream consumers receive generous access. Credit builders face tighter limits. The gap is widening.

Looking Forward: 2026 Landscape

Employment remains critical. Current payment declines reflect pressure among employed consumers. Unemployment increases would accelerate these trends, particularly in the monoline segment.

Interest rate policy matters. Cuts would provide cash flow relief and potentially reverse payment ratio deterioration.

Credit availability decisions. Monoline tightening in early 2025 suggests lenders are watching carefully. Further payment deterioration could trigger broader restriction.

Operational resilience. The postal strike demonstrated how external disruptions can temporarily distort credit metrics. Lenders should continue encouraging digital payment adoption to reduce vulnerability to similar events.

Our base case expects gradual stabilization rather than continued deterioration. But the margin for error has narrowed. Stress concentration in newer accounts creates vulnerability to any economic shock.

The Bottom Line

Q4 2025 tells a story of managed decline rather than crisis. Once we adjust for the postal strike disruption, Canadians are meeting obligations - delinquency improvements prove that. But they're accepting higher interest costs and extending repayment timelines.

The three-year payment ratio trajectory reveals where stress is concentrated: newer and mid-tenure accounts across both segments. Veteran customers have maintained discipline, but the pipeline of credit builders is struggling to establish sustainable payment habits in a challenging economic environment.

The market has divided. Bank card customers remain healthy despite behavioral shifts. Monoline customers face acute pressure, with payment ratios below critical thresholds and lenders responding with tighter credit.

This isn't sustainable indefinitely. Either conditions improve enough to restore payment capacity, or gradual erosion eventually becomes delinquency stress. The postal strike showed how quickly external factors can amplify underlying vulnerabilities - and how concentrated stress becomes in vulnerable segments.

How FICO Can Help You Manage Credit Card Risk and Performance:

Explore our solutions for customer management.

See my previous posts on CA card performance.

Make more informed and profitable decisions with FICO’s Scoring Solutions.

Popular Posts

Average U.S. FICO Score at 717 as More Consumers Face Financial Headwinds

Outlier or Start of a New Credit Score Trend?

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read more

Average U.S. FICO® Score stays at 717 even as consumers are faced with economic uncertainty

Inflation fatigue puts more borrowers under financial pressure

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.