Evolving Landscape of Machine Learning Relative to the FICO® Score

How does progress in artificial intelligence stack up to the FICO credit score model?

Artificial intelligence (AI) was around long before the start of my career, and back in the ‘90s, analyst tools and techniques were rooted in AI paradigms invented decades earlier. Early on during the evolution of AI, credit risk scores started out as small and manually designed linear discriminant models. In later years, when I turned toward applied business analytics, data and models grew larger. Nonlinear models, sometimes augmented with automatically discovered complex predictive features, became more widespread.

Before I delve into the evolving landscape of machine learning relative to the FICO® Score, it is crucial to clarify that AI is not used in the final version of the FICO® Score algorithm. However, AI is employed during the research phase to help identify data that has the potential to be highly predictive. This approach contributes to improving the overall effectiveness of the FICO credit score model.

Recently, I caught up with an industry leader, Rob Jasper, Advisor for the Pacific Northwest National Laboratory, for a thought-provoking discussion about the historical impact of AI and its influence on credit scoring. We drew comparisons between FICO’s augmented intelligence philosophy and the common perspectives on the use of AI and machine learning in applied business analytics. Rob took stock of the astonishing advancements of AI and machine learning spanning more than six decades. He explained that the latest advances have increasingly focused on sheer predictive power, often to the detriment of explainability, and given way to the black box problem. I expanded on Rob's insights by contextualizing how the human-centric modeling culture that underpins the FICO® Score has evolved for several decades to the need for providing credible explanations, not just predictions, foreshadowing some more recent developments in the field of explainable AI/machine learning.

After defining AI as “computer systems capable of performing complex tasks that historically only a human could do,” Rob explained that this definition is a moving target because technologies that were regarded as AI decades ago are now regarded as computer science. Intellectually demanding tasks once viewed as only achievable by humans were shockingly accomplished in a superior manner by AI and then subsequently became normalized as computer science, such as handwritten digit recognition or playing chess, leaving the ever-shifting forefront of AI to keep tackling more complex tasks.

Developing a new credit risk scoring algorithm for the FICO® Score is an example of a complex modeling task that we accomplish with a diverse team of experienced data scientists and subject matter experts. Ironically, what makes the task so complex and dependent on domain expertise is that the credit scoring algorithm must be transparent, reliable, and intuitive for all human stakeholders in the financial ecosystem, including the borrower, lender, regulator, and investor.

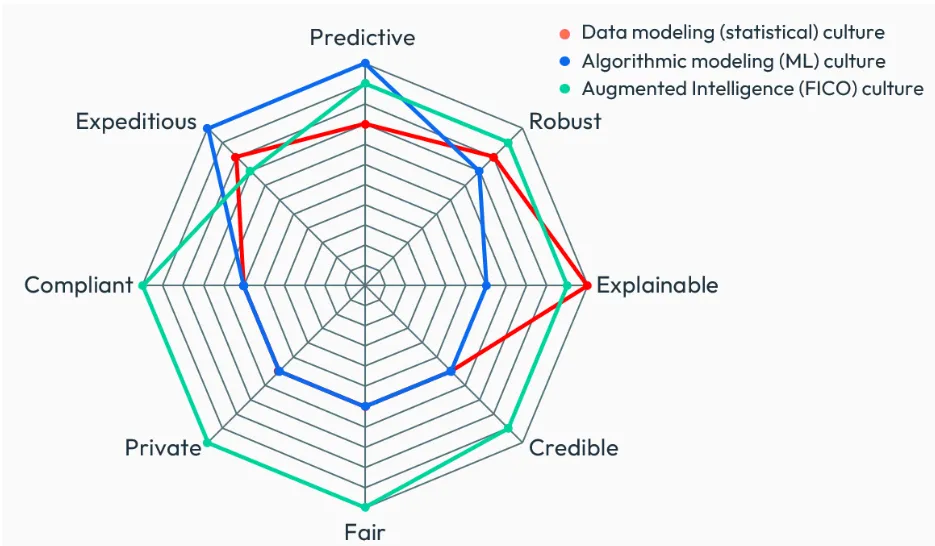

The radar chart below lists multiple objectives for the FICO scoring algorithm: It needs to be highly predictive and this score power needs to be robust in the face of data drift as economic tides are ever shifting and the consumer credit landscape is always evolving.

The scoring algorithm also needs to be explainable and credible for humans and should be expeditiously developed and deployed. Fairness, privacy, and compliance are non-negotiable requirements. Tradeoffs may exist between certain objectives where they may oppose each other. Striking the responsible balance is a fundamental requirement for the FICO® Score.

Professor Leo Breiman, a statistician and machine learning pioneer, highlighted important tradeoffs between model development objectives in his landmark paper “Statistical Modeling: The Two Cultures.” For example, Breiman’s random forests, a class of machine learning models, might be expediently trained in the algorithmic modeling culture. This approach, with minimal human involvement in the model training phase, aims to achieve greater accuracy and predictive performance than a regression model painstakingly developed by a statistician adhering to the data modeling culture while focusing on objectives of inference and explanation, rather than prediction. The machine learning model might then be harder to explain than the regression model, as the red and blue lines in the radar chart illustrate. Rob agreed, vividly describing differences between members of the two modeling cultures in their attitudes towards modeling.

The objectives on the radar chart are a simplification. Underneath some objectives, there may be further sub-objectives. For example, the FICO® Score must be highly predictive for numerous use cases characterized by alternative prediction targets (e.g., default on a car loan or credit card payment), similar to the sub-field of multi-task learning in machine learning.

To satisfy the requirements for the FICO® Score and to strike the best balance across multiple objectives, FICO’s data scientists leverage inherently interpretable and constrainable, multi-objective machine learning techniques for credit risk model development to capture robust predictive signals from the data sources in the form of explainable predictive features that drive the FICO® Score. Data scientists and domain experts are in the driver’s seat to steer machine learning toward a responsible balance. Enhancing the perspective of Breiman’s paper, we embrace a “third culture” of augmented intelligence rather than artificial intelligence, which sits between the two extreme cultures highlighted. The augmented intelligence approach tailors the scoring algorithm to human needs and is done with the help of machine learning to add effectiveness and efficiency to the tedious parts of model development. Developing a new FICO® Score is not something today’s mostly data-driven artificial intelligence could accomplish without major human guidance, which leads to my claim that “AI alone just doesn’t cut it.”

We are continually advancing our algorithms, tools, and processes to improve on all objectives on FICO® Scores. A recent example targeting the “expeditious” objective is “data sculpting.” This novel capability we’re piloting in our FICO® Scores Innovation Lab initiative shows promise to help accelerate lender adoption of new credit scoring models. Lender-specific applicant populations often differ from FICO's development baselines. Data sculpting adjusts FICO's development population to match the distribution profiles of individual lenders, resulting in more accurate simulation outcomes and improved KPI projections – allowing lenders to reduce time to value for a new or updated credit scoring model.

Learn More About Augmented Intelligence and Data Sculpting:

Watch my full discussion with Rob Jasper here: The Evolving Landscape of Machine Learning Relative to the FICO® Score 2024 | FICO

View the presentation deck here: The Evolving Landscape of Machine Learning Relative to the FICO® Score Presentation

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.