The GSE Data Is Public. Here's What It Shows About Credit Score Modernization.

Independent Milliman analysis of GSE historical data confirms what anyone can now verify directly: FICO® Score 10T is the most predictive score.

The FICO® Score has been foundational to the safety and soundness of America's $13 trillion mortgage market for decades — helping standardize credit risk evaluation across originations, secondary market transactions and portfolio management. We take that responsibility seriously.

That responsibility is why FICO has supported the credit score modernization process from the start. And realizing that promise depends on choosing the best, most predictive score, a determination that new data can now inform directly.

On July 1, 2026, Fannie Mae and Freddie Mac released expanded historical loan-level datasets that, for the first time, include FICO® Score 10T data spanning more than 12 years from April 2013 through September 2025. Global actuarial firm Milliman analyzed this newly released, publicly available data.

The findings: FICO® Score 10T outperformed VantageScore 4.0 across every measure tested, across every vintage, and across different borrower profiles. Any lender, analyst or investor can download the same data and verify FICO Score 10T outperformance for themselves.

The next chapter in a consistent story

When Fannie Mae and Freddie Mac completed their own independent evaluation under the FHFA’s Validation and Approval of Credit Score Models final rule, they recommended FICO® Score 10T and recommended against VantageScore 4.0. That recommendation was made by analyzing some of the very same data now publicly available. That conclusion was made public through FOIA requests and shared by the Housing Policy Council.

Additionally, in May 2026, Milliman published an analysis comparing predictive performance across nearly 20 million mortgage tradelines based on data from a major credit bureau. FICO® Score 10T outperformed VantageScore 4.0 across all mortgage types and statistical measures tested.

Different data sources. Different time periods. Independent methodologies. The same result: FICO® Score 10T is the most predictive credit score available for use by the mortgage industry.

Why this dataset changes the conversation

This is loan-level performance data from Fannie Mae and Freddie Mac, the actual loans backing the conforming mortgage market. And because the data is publicly available, the findings are reproducible: any lender, analyst or investor can download the same files and reach their own conclusions — and we encourage all lenders, analysts and investors to do so by downloading the data here:

Fannie Mae: https://historicalcreditscores.fanniemae.com

Freddie Mac: https://sf.freddiemac.com/general/credit-score-models

The research already completed: what Milliman found

Milliman applied the same three statistical measures to the GSE public datasets that were specified in the Joint Enterprise Credit Score Solicitation (see page 10) — the criteria Fannie Mae and Freddie Mac themselves established for evaluating credit score models:

K-S Statistic — overall ability to rank-order borrowers by default risk

Bottom Decile Lift — how well the score identifies the highest-risk borrowers

Gini Coefficient — overall predictive power across the full score distribution

Summary of key findings:

FICO® Score 10T outperformed VantageScore 4.0 on all three measures and across every origination year studied, both individually and in aggregate.

FICO® Score 10T demonstrated particularly strong improvement versus VantageScore 4.0 on the most recent origination vintages, which are of particular interest, because they carry some of the highest default rates found in the dataset.

FICO® Score 10T's predictive advantage is even more pronounced for first-time homebuyers, offering predictive lift over VantageScore 4.0 in excess of 10% for those borrowers.

For the K-S statistic, FICO® Score 10T's improvement relative to VantageScore 4.0 is approximately 5% across non-COVID origination years, over 6% when all origination years are included, and over 8% when focusing on the most recent vintages.

FICO® Score 10T has now demonstrated superior predictive performance across two independent datasets and analyses, while applying the same rigorous methodology.

Running the analysis for yourself

We welcome everyone to analyze this data for themselves. Credible analysis requires careful attention to methodological considerations, including truncation effects and outcome window consistency. For a summary of some important analytical considerations, see FICO’s guide here: Analyzing the GSE Historical Data: Key Considerations in the Evaluation of Credit Scores.

Why the FICO® Score 10T predictive advantage matters for lenders and borrowers

A consistent improvement in default predictive accuracy compounds across thousands of mortgage decisions: in approvals extended with confidence, and in loans not approved for potential borrowers who cannot sustain them. FICO® Score 10T can expand mortgage approval rates by up to 5% without adding incremental risk relative to Classic FICO® Score or reduce delinquency rates by up to 17% for new originations.

The GSE data confirms this advantage extends especially to first-time homebuyers — a population that carries meaningfully higher default risk, and where the accuracy of the credit score is critical to providing a strong foundation for long-term financial success.

The real cost of a less predictive score — at the loan level and the portfolio level

The cost question that matters most isn't the one being debated loudest. It's the cost of less accurate default prediction, and it compounds.

At the loan level, the problem is structural. Under the FHFA's current policy, lenders can choose between FICO® Score 10T and VantageScore 4.0 on a loan-by-loan basis. That flexibility creates adverse selection incentives that concentrate risk, bias default rates and create pricing uncertainty for MBS investors.

At the portfolio level, the performance gap is significant, and it widens in the segments that matter most for comparison: the most recent origination vintages, where stress shown via default rates are highest.

The more predictive score is not just the better analytical choice. It is the structural foundation that keeps the system liquid and stable for lenders, investors and borrowers alike.

The FICO® Score advantage

Let’s be clear – the advantage is not in the data. The data both scores have access to is the same, despite claims to the contrary. Both scores fully incorporate trended credit data and reported rental payment history. The advantage FICO® Score 10T has is the experience we utilize in developing the score on how to use that data. Our techniques create a score that is not only the highest performing in default prediction, but the most stable and trusted signal in the marketplace.

We take our responsibility of building a score that will stand the test of time very seriously. It is why we don’t build our score with a single goal of “scoring more,” but with dual goals of “scoring more, better.”

VantageScore 4.0 claims to score more consumers because they have access to more data. This is false. VantageScore uses looser scoring criteria to generate more scores. More scores does not equate to more approvals. Scoring more, better — FICO's goal — is what will put more Americans into homes.

Attempting to expand access through reduced accuracy is not a tradeoff FICO makes: FICO® Score 10T expands access via improved predictive accuracy and without penalizing first-time homebuyers through the use of variables that should be questioned by the industry.

The GSE data proves the point: it evaluated both scores on the same borrowers and the same outcomes; the question it answers is which score predicts default more accurately for that population. On that question, the Milliman analysis is unambiguous.

What you can do next

The GSE data is public, the methodology is established, and the findings are reproducible. Here are some next steps you can take today:

Start your own evaluation on your loan portfolio.

Three paths make that evaluation accessible now:

The FICO® Score 10T Free Access Program provides FICO Score 10T at no cost alongside Classic FICO® Score, enabling side-by-side performance testing on live originations without adding to your credit data spend.

The FICO® Archive Score Program offers mortgage lenders up to two million free archive FICO® Scores using depersonalized historical consumer credit data for retrospective testing and validation across existing portfolios.

The FICO® Mortgage Direct License Program offers a straightforward path to production deployment for lenders ready to move FICO® Score 10T into their origination process.

To learn more or discuss the right path for your institution, visit the FICO Score 10T Migration Resource Center or contact FICO's Mortgage and Capital Markets team directly.

Download the GSE data and run the analysis yourself.

Fannie Mae: https://historicalcreditscores.fanniemae.com

Freddie Mac: https://sf.freddiemac.com/general/credit-score-models

Educate yourself on the actual differences in how these models are built and the implications for your business and potential borrowers (cut through the noise and misinformation in the marketplace).

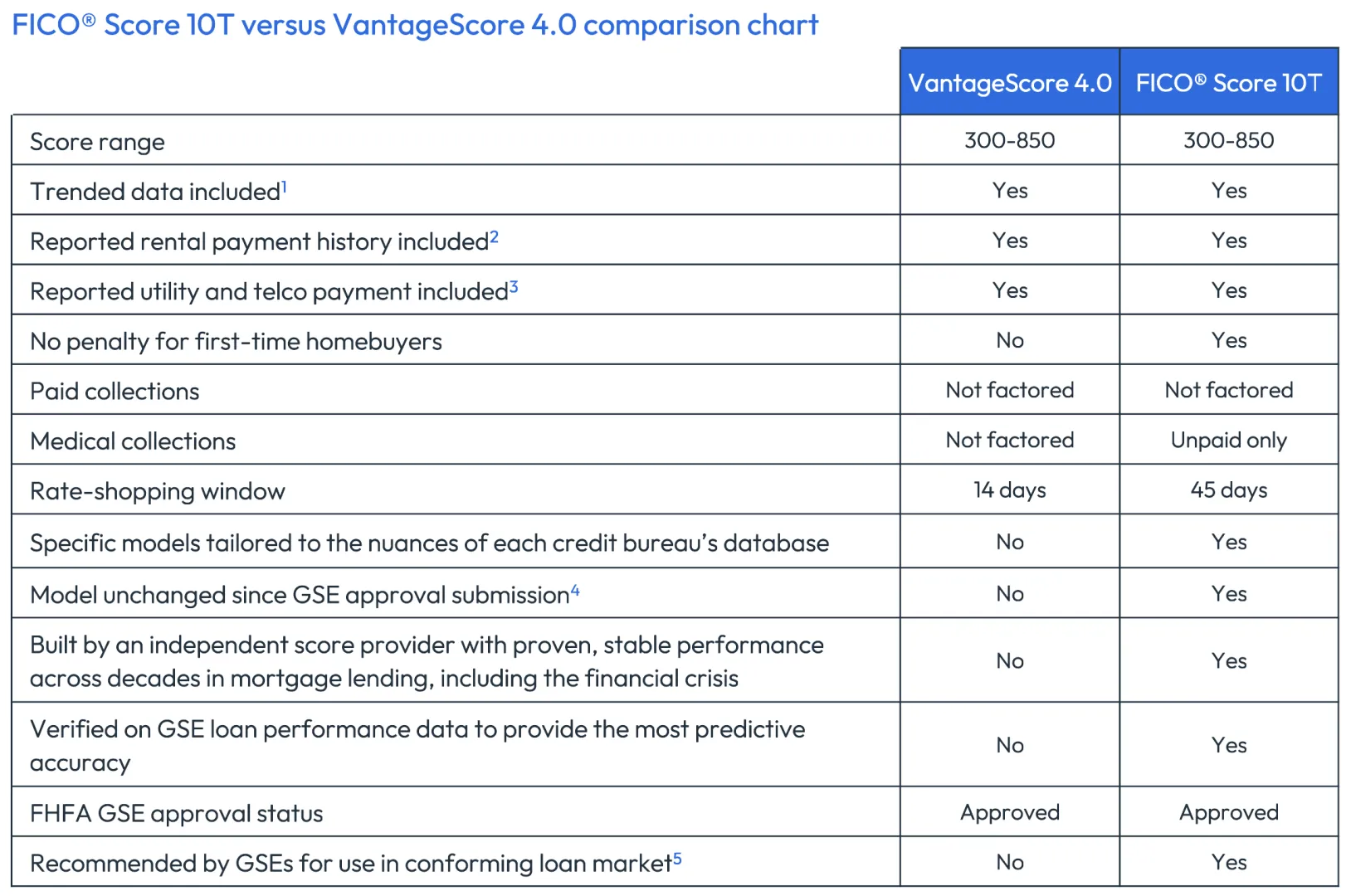

1Trended credit data was first made available from all three credit bureaus in 2011.

2FICO® Score versions since 2015 have included reported rental payment history data, including FICO® Score 9, FICO® Score 10, and FICO® Score 10T.

3FICO® Scores have always considered utility and telco payment data that is furnished to the three nationwide U.S. credit bureaus.

4VantageScore removed all medical collections from VantageScore 4.0 calculations in 2023

5On 2/2/26, the Housing Policy Council published a FOIA response from the FHFA detailing the results from the Credit Score Assessment conducted in 2021. What’s clear from unredacted documents: FICO® Score 10T was determined to be the sole credit score model recommended by the GSEs.

The performance findings speak for themselves — and now, so can the data for all of you.

This study was commissioned by FICO and conducted by Milliman.

Frequently Asked Questions

Both scores incorporate data from the same bureau sources, and both use trended credit data. The performance gap is not explained by data access. It reflects differences in model design and architecture: what variables are included, how each score weighs and interprets borrower behavior, and the design philosophy applied during development. FICO® Score 10T achieves its performance advantage without using mortgage-specific variables that would penalize borrowers who have not previously owned a home — and it still outperforms.

Some have pointed to VantageScore 4.0's ability to generate scores for thin-file or previously unscored consumers as a "more data" advantage. That argument confuses universe expansion with predictive accuracy. The GSE dataset includes the same loans evaluated using both scores — the population, the data, and the outcomes are identical for both models in this analysis. The relevant question is which score better predicts default for borrowers both scores can evaluate. On that question, the data is clear.

Machine learning is a modeling technique, not a performance measurement. FICO uses all types of modeling techniques in our building of the FICO Score. We don’t call them out – because the technique is only as good as the scientist using it. What does matter — the measure of how a credit scoring model separates borrowers who will default from those who won't — as this is the purpose of a credit scoring model. This is precisely what the K-S statistic, bottom decile lift and Gini coefficient measure. On both the Milliman bureau data study and now the GSEs' own publicly released loan-level data, FICO® Score 10T outperforms VantageScore 4.0 on every one of those measures. The architecture used to build a model matters far less than what the model actually does with borrower data — and the independent evidence consistently shows FICO® Score 10T does it better.

Prior analyses, including Milliman's May 2026 study, drew on credit bureau data not directly accessible to the public. The GSE datasets are different: Fannie Mae and Freddie Mac have published them openly, so any stakeholder can download the same data and replicate the analysis. That transparency makes the findings independently verifiable by any lender, investor or researcher who chooses to look — and eliminates any basis for claims about data selection or methodology bias.

Yes. Under the FHFA's Validation and Approval of Credit Score Models final rule, both Fannie Mae and Freddie Mac conducted extensive testing and review. Documents obtained through FOIA requests revealed that experts within the GSEs recommended FICO® Score 10T and recommended against VantageScore 4.0 for GSE use. The Milliman analysis of the same GSE public datasets now independently confirms what the GSEs' own internal evaluation found — FICO 10T outperforms Vantage Score 4.0.

Refer to FICO’s blog published July 6, 2026, entitled “Analyzing the GSE Historical Data: Key Considerations in the Evaluation of Credit Scores” for key considerations when working with the datasets.

You can download the Single-Family Loan-Level datasets directly from Fannie Mae and Freddie Mac. Both GSEs have published historical datasets that include all three scores Classic FICO® Score, FICO® Score 10T, and VantageScore 4.0, alongside loan performance data spanning April 2013 through September 2025.

Because loan-by-loan score selection of a less predictive score introduces adverse selection risk that compounds across the system. Prior Milliman research found that FICO® Score 10T and VantageScore 4.0 place a significant share of borrowers in different LLPA pricing bands — meaning systematic selection of the higher score for each borrower concentrates borrowers for whom VantageScore 4.0 is optimistic relative to actual risk into one pool. That dynamic will increase default rates, create pricing uncertainty for servicers and MBS investors, and ultimately puts upward pressure on mortgage rates increasing cost for borrowers. The answer to the score decision is not a loan-level arbitrage strategy. It is choosing the most predictive score consistently — and using it. This ensures mortgage liquidity, execution and consistency.

Both. FICO® Score 10T can expand mortgage approval rates by up to 5% without adding incremental risk relative to Classic FICO or reduce delinquency rates by up to 17% for new originations. A score that is more precise at identifying high-risk borrowers is, by definition, also more precise at identifying low-risk borrowers. That precision translates simultaneously into fewer defaults and more confident approvals — stronger portfolio performance and a larger addressable borrower population served responsibly.

VantageScore is jointly owned by Equifax, Experian and TransUnion. The score, the data and the distribution channel are all controlled by the same organizations. FICO is independent. Its sole interest is the performance of the score. And that independence is what has allowed the FICO® Score to maintain the trust of lenders, investors, and market stakeholders for over 30 years.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.