How to Manage the Rise in Credit Delinquencies

Skyrocketing delinquencies in the US and other markets pose a threat that demands the use of decisioning-as-a-service

Guest post by Navdeep Gill, senior industry principal and head risk practice, Infosys, and Sharan Bathija, Infosys Knowledge Institute

Lenders in many countries are facing a rise in consumer credit delinquencies, a domino effect from the pandemic. Our research with FICO’s Robert Jones and Amir Sikander describes the crisis and how technology can help lenders manage this increase in delinquencies.

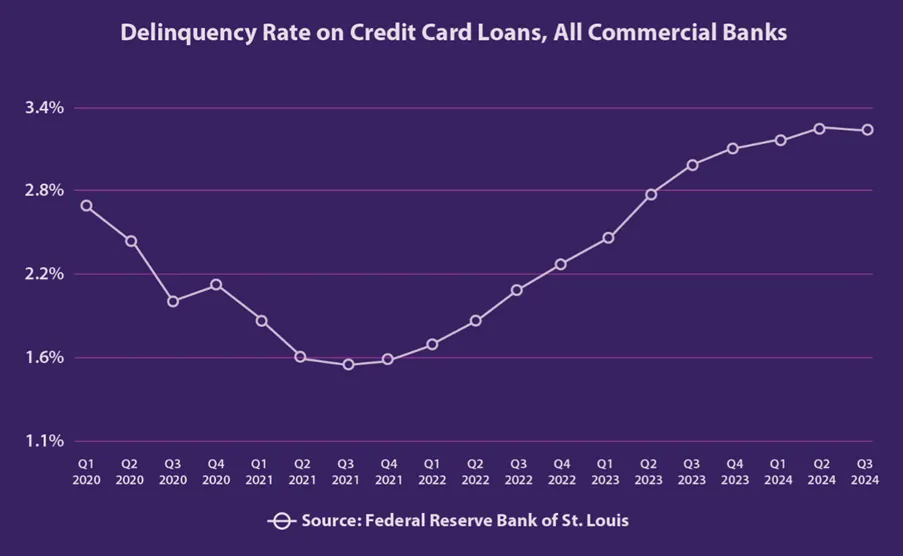

Years after the pandemic, credit delinquencies remain high. For instance, credit card delinquencies in the US (defined as outstanding balances that have not been paid for more than 30 days) doubled from 1.6% in 2021 to 3.4% in 2024, reaching a four-year high.

Since January 2020, unit delinquency rates in the US (the percentage of individual loans that are delinquent) have increased by over 50%. However, balance delinquency rates (the dollar amount of loans that are delinquent) have risen at an even steeper pace. Notably, balance delinquencies have surged by 51% over the past two years, yet this is only one part of a broader and growing concern.

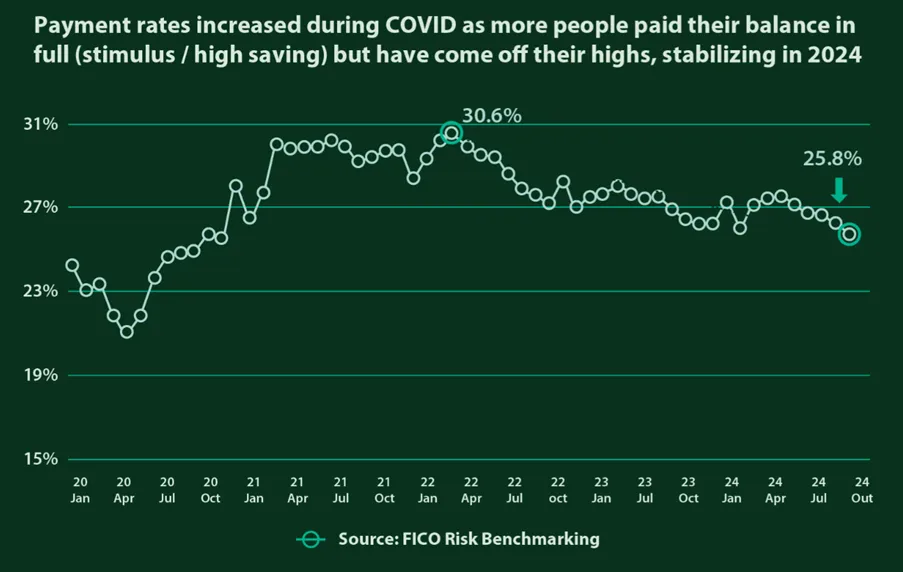

Card Payment Rates Also Trending Downward

Initially buoyed by heightened savings and government support during the COVID-19 pandemic, payment rates on US credit cards surged. However, they have steadily declined since peaking in 2022. While it remains uncertain whether this trend will persist, lenders must be prepared for a sustained environment characterized by rising delinquencies and declining payment rates.

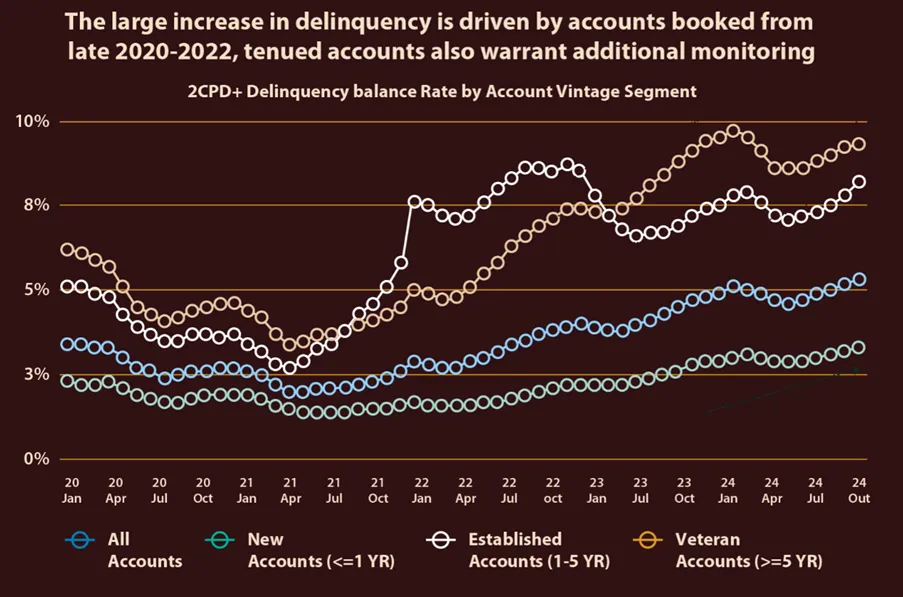

Even longstanding accountholders are now at risk of delinquency, pointing to broader economic pressures. New tariffs, recession concerns, and ongoing uncertainty suggest delinquency rates may stay high in the near term.

With macroeconomic conditions unlikely to ease delinquency rates and high household debt, many lenders are concerned about their balance sheets. However, those willing to take decisive action have an opportunity to implement targeted, timely, and effective data-driven interventions. An advanced decision infrastructure is key.

Solving the Delinquency Dilemma

Lenders must first address delinquencies by gaining a clear understanding of their underlying drivers. Several factors contribute to the upward trend in delinquencies, including:

- Lenient credit standards during the pandemic

- Government stimulus in the recovery phase

- The post-recovery rise in inflation

The rising delinquency trends highlight the urgent need for financial institutions to have a 360-degree view of their customers’ financial profiles. Whether it’s a missed payment or a significant dip in cash flow, a comprehensive perspective enables proactive monitoring and the early detection of financial distress signals.

However, most lenders still struggle with siloed data, which creates several blind spots that impede overall delinquency management. Financial institutions with access to integrated, real-time data are better equipped to respond swiftly and implement tailored interventions, such as personalized payment plans or proactive engagement strategies.

"We want to be able to look at the whole relationship when making decisions about any customer,” notes Chip Clarke, SVP, Risk Management at KeyBank. “The advantage we’re seeing is the ability to bring all these disparate data sources together to make our decisions. It enhances our scoring models and our strategies and helps direct the collections department in applying those strategies once they get them."

Applying Transaction Data in Risk Management

Analyzing transaction data is crucial to understanding customer behavior, preferences, and creditworthiness. Through advanced analytics and timely action, financial institutions can better support their customers while minimizing risk.

In the case of delinquencies, advanced analytics enable early warnings for lenders to manage customer risks with insights. Many lenders are already capturing the relevant customer data but have not applied the advanced analytics necessary to act on it.

One lender that has seen a major advantage using transaction data and FICO Platform is Australia’s ANZ Bank. "As a Chief Risk Officer, transaction scoring makes my job more fun and makes me feel more connected to the customer,” says Jason Humphrey, CRO at ANZ Bank. “Not only can we see the types of transactions changing, we know exactly who these customers are. By getting to them earlier and contacting them in their time of need, we've had a positive reaction when it comes to our pre-delinquency and collections strategies. Better predictiveness means more targeted and better outcomes for our customers. And our customers is how we win as a bank."

A Customer-Centric Solution for Pre-Delinquency

Financial institutions often focus on delinquencies after they have occurred. But with the advantage of customer insights, lenders can identify customers experiencing hardship before a missed payment, enabling delinquency strategies that are predictive, proactive, and preventive.

Nearly 25% of first payment default conditions in the US card industry are related to not having accurate customer contact information.

With a proactive pre-delinquency strategy powered by connected data and advanced analytics, financial institutions can launch tailored treatments with minimal effort that yield higher collection rates.

Using Decisioning-as-a-Service to Manage Risk

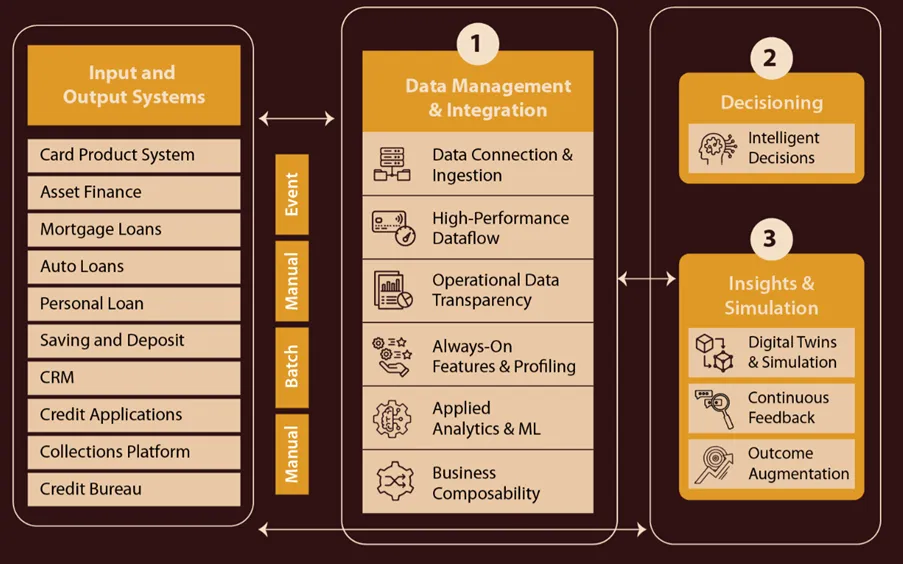

Legacy systems, disjointed across lines of business, are difficult to integrate, inefficient to maintain, and lack transparency in terms of results and regulatory requirements. Understanding that real-time customer insights go a long way, we developed Infosys Decisioning-as-a-Service, powered by FICO. Decisioning-as-a-Service (DaaS) is a unique, cloud-based solution that accelerates the modernization of an enterprise's decision-making capabilities.

As financial institutions look to modernize decisioning frameworks, the need for speed, consistency, and intelligence in every choice becomes critical. DaaS addresses this by unifying fragmented systems into a cohesive, cloud-native platform, enabling institutions to respond to change with confidence and precision.

From revenue growth to cost optimization and reduced losses, our solution helps enterprises transform from a fragmented application and data landscape to a unified platform with best-in-class capabilities.

Our approach, built on three foundational pillars, enables financial institutions to harness internal and external data seamlessly, utilize AI and machine learning for smarter decisions, and score transactions efficiently for enhanced risk management.

Pillar 1. Data management and integration

Achieving a 360-degree view of the customer is no longer optional, it’s essential. By integrating data across sources in real-time, DaaS leverages advanced AI/machine learning to provide customer profiles that are contextual and comprehensive.

Pillar 2. AI-driven decisioning

DaaS’s capabilities ensure decisions related to credit risk, fraud prevention, or personalized offers are based on the most up-to-date insights, enabling strategic, timely shifts on the fly.

Pillar 3. Insights and simulation for predictive excellence

As financial institutions navigate rising complexity, the ability to simulate, test, and refine decision paths in real time becomes a critical differentiator. With configurable intelligence embedded into the process, organizations can continuously evolve their strategies to adapt to shifting market dynamics and to create value at every step of their way. It is a shift from decision-making as a function to decision-making as a strategic asset.

Whether it’s detecting the early signs of delinquency, enabling proactive customer engagement, or ensuring decisions are aligned with customer needs and organizational goals, DaaS enables decisions with measurable outcomes.

Predict. Personalize. Prevent.

DaaS empowers financial institutions to integrate data across internal and external sources, leverage AI/ML for smarter, faster decisions, and apply real-time scoring to manage strategies, risks, and delinquencies. This comprehensive approach not only enhances decision-making but also ensures proactive and personalized engagement with customers and loyalty in the long run.

How Infosys and FICO Can Help You Manage Delinquencies and Customer Relationships

- Read our ebook, Reimagine Delinquency Management: Predictive, Proactive, Progressive

- Learn about the Infosys FICO partnership

- See more about Infosys Decisioning-as-a-Service, Powered by FICO

- Discover the power of FICO Platform

- Email askus@infosys.com

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.