New UK Credit Cards Data Shows Lower Spending, More Delinquencies

Financial pressures on UK consumers are evident in drop in spend and rise in delinquencies on credit cards

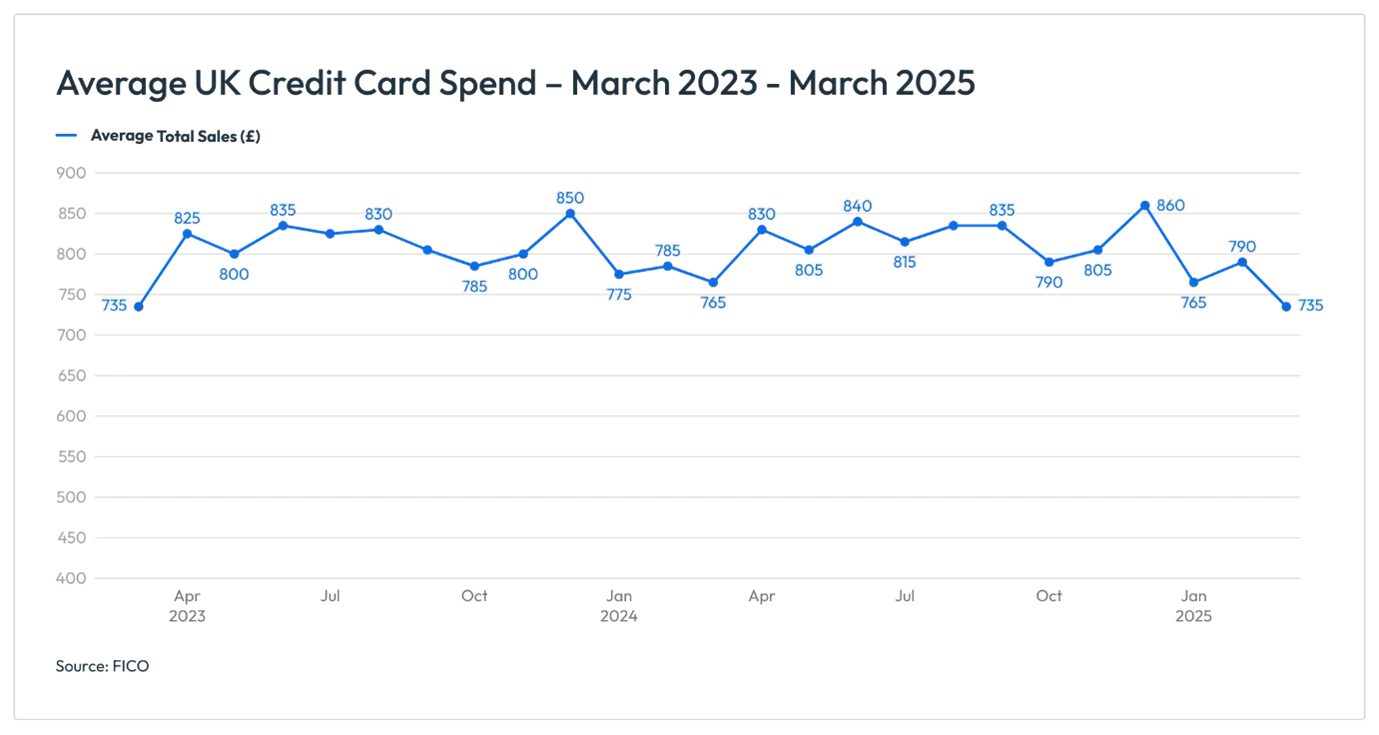

While the months after Christmas typically see spend on credit cards fall, our latest UK Credit Market Report underlines the financial pressures impacting UK borrowers.

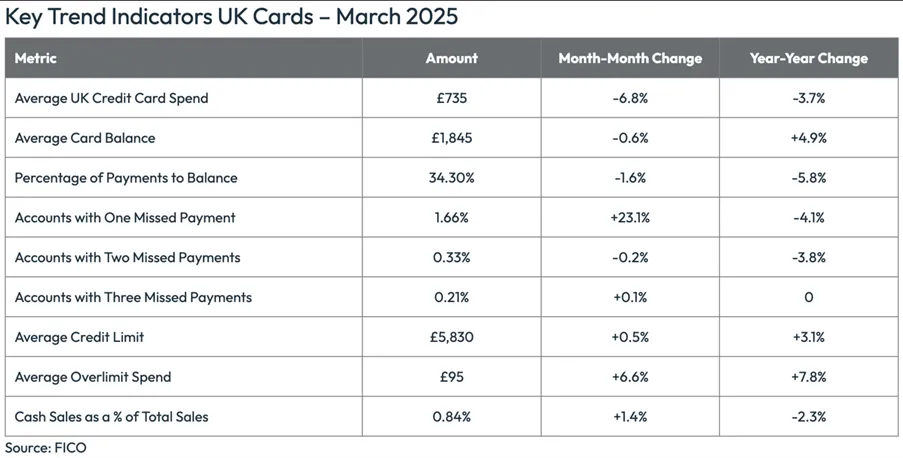

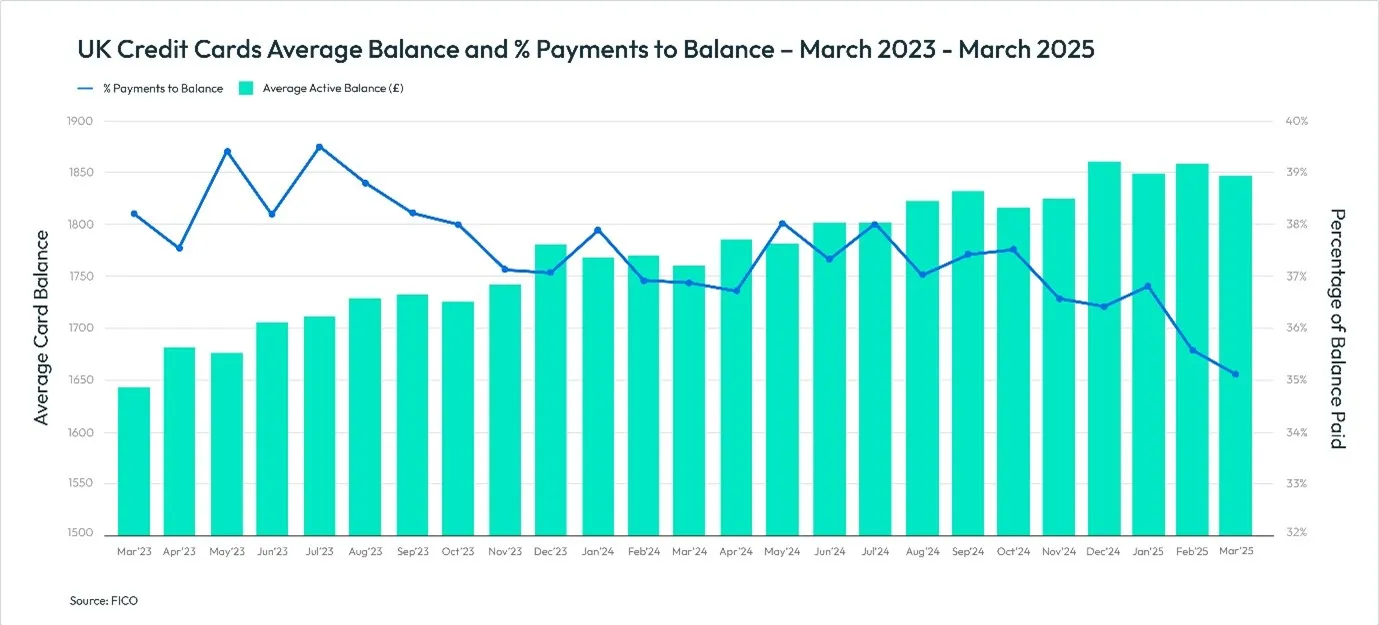

Following seasonal patterns, average spend was 6.8% lower than February and 3.7% down compared to March 2024. However, payments to balance also fell in March, by 1.6% month-on-month and 5.8% year-on-year, resulting in higher average balances compared to 2024. Established cardholders who have had their cards between one and five years, and who have missed one payment, saw the largest drop in payments to balance, which will be a concern to lenders managing credit risk.

Highlights in UK Credit Card Trends

- Average credit card spending fell 6.8% month-on-month and 3.7% year-on-year

- Average balances rose by 4.9% year-on-year

- The number of customers missing one payment rose by almost a quarter (23%) compared to February 2025

- The average balance of one missed payment is 5.6% higher year-on-year

- Average balances for customers with one, two or three missed payments are higher than the same period in 2024

· The percentage of customers using credit cards for cash fell for the sixth month in a row and now stands at 2.9%, a 2.1% monthly decrease and an 8.7% annual decrease

With spend having decreased by 6.8% month-on-month and 3.7% year-on-year, average spend now stands at its lowest point for two years at £735. However, higher living costs have contributed to higher balances, which have increased 4.9% compared to March 2024, now standing at an average of £1,845.

UK Credit Card Delinquencies Trends

The trend in missed payments will be a concern for lenders, in particular the sharp increase of 23% month-on-month for one missed payment. The average balance decreased 1% month-on-month to £2,320 but is still 5.6% higher year-on-year and is trending upwards.

The percentage of consumers missing two payments dropped 0.2% month-on-month and 3.8% year-on-year, while customers missing three payments has been increasing since October 2024. The average balance of two missed payments is also trending upwards. With an average of £2,875, it is 2.5% higher than February and 6.4% higher than March 2024. The average balance of three missed payments is also trending up, by 0.9% on the previous month and by 6.6% on the previous year equating to an average of £3,220.

Although the average delinquent balances are trending upwards, so is the overall balance. When comparing the delinquent balance to the overall balance, the increase in balances for one missed payment is comparable. However, since January 2025, the increase in balances for customers with two or three missed payments balances has increased at a higher rate.

Lenders should, therefore, review balance and risk score breaks within debt collections strategies, ensuring customers with higher balances at risk are prioritised and receive flexible and tailored treatment. Particular focus should be given to customers who have had their cards between one and five years, especially for those who are coming off promotional offers and who may now be struggling to pay off higher APRs, to prevent defaults.

These card performance figures are part of the data shared with financial institutions that subscribe to the FICO® Benchmark Reporting Service. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80% of UK card issuers. For more information on these trends, contact FICO.

How FICO Can Help You Manage Credit Card Risk and Performance

- Explore our solutions for customer management

- See my post on UK Credit Card Trends 2023-2024: More Spend and Delinquencies

- Read more posts on UK cards

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.