New UK Data: Good Fraud Prevention Is Vital to Attract New Customers

FICO survey demonstrates the importance of fraud protection to today’s customers and the need to effectively balance security with convenience

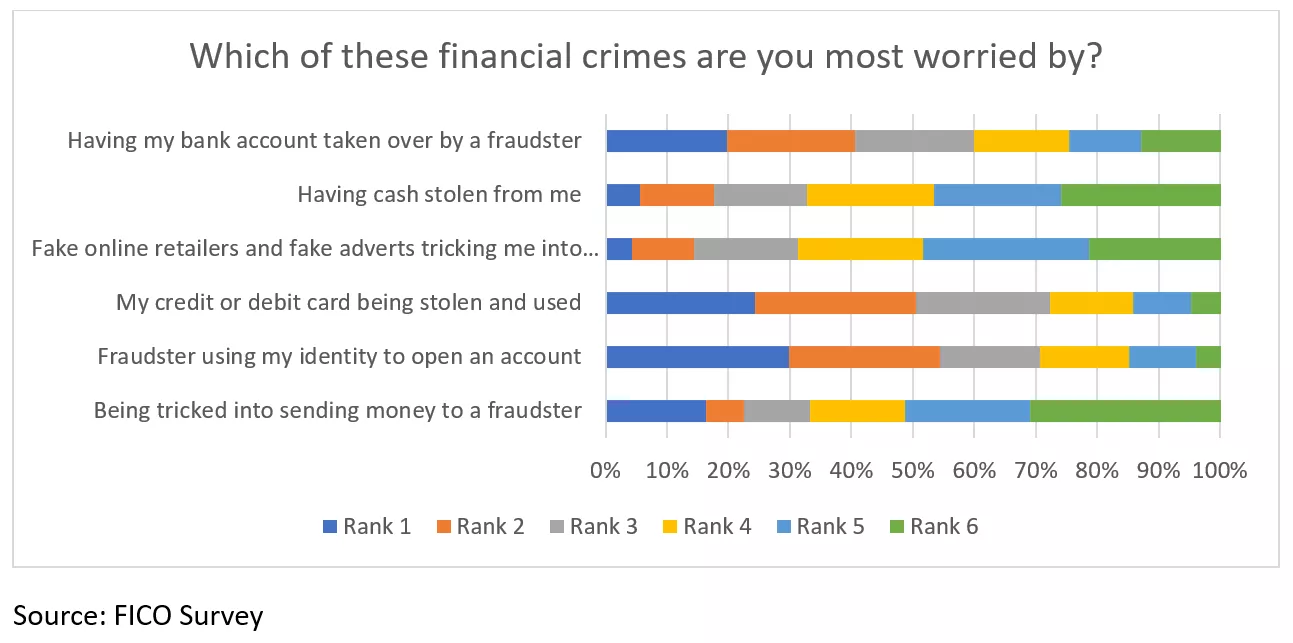

Fears around ID theft haunt Brits after it emerged nearly a third (30%) of the UK population admit to being worried about their identity being stolen by fraudsters to open financial accounts. A further one in four people (24%) have expressed concerns about their credit or debit card being stolen and used, while 20% worried about their bank account being taken over by a fraudster. Given that in the first half of last year, £340.7 million of fraud losses in the UK were from unauthorised transactions and fraud now accounts for around 40% of all crime there, these concerns are very much justified.

Despite these rising levels of fraud and noticeable anxiety that people are feeling about unauthorised transactions on their financial accounts, UK consumers are still ‘digital’ buyers and would choose primarily the digital route to opening accounts. For example, 79% want to open savings accounts digitally, 77% for current accounts, 73% for mobile phone accounts, 70% for credit cards and 59% for insurance policies.

Although fewer would take the digital route where bigger-ticket items are concerned, there’s still a significant enough desire for it - mortgages (24%), car loans (23%) or personal loans (31%).

Consumers don’t want to lose the ability to manage financial transactions digitally. What they want is confidence that the financial institutions they choose to bank with, borrow from or take out insurance with, will protect them at all times.

For the financial institutions trying to acquire and retain those customers, this means effective fraud prevention strategies.

Demand for Good Fraud Prevention Is Driving Customer Behaviours

Over a third of the population (34%) have stated that fraud prevention is the top consideration when selecting a new financial account, while nearly three in four (72%) see it as one of their top three considerations.

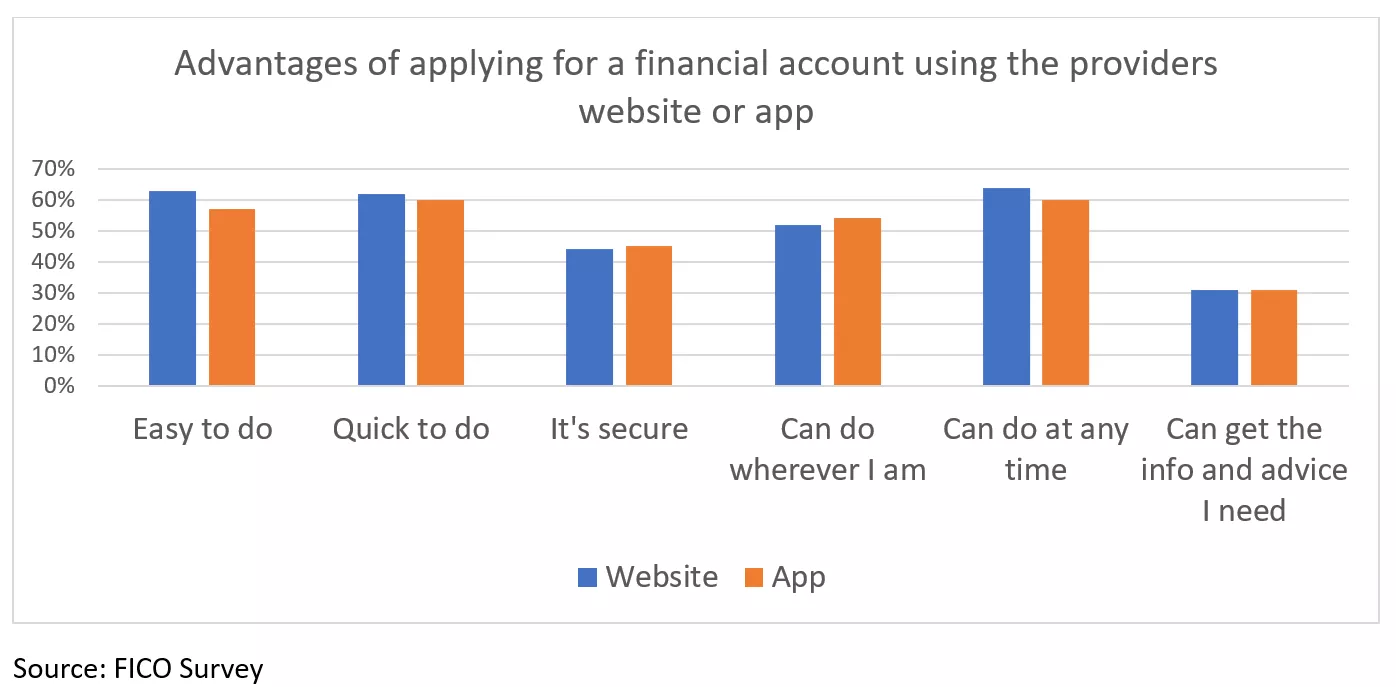

Customers both desire and appreciate the convenience of being able to apply for a new financial account digitally, but at least one in two still have reservations about how secure providers’ website or apps actually are when it comes to opening financial accounts through them. 57% of the population do not think websites are secure, while 55% have the same misgivings about providers’ apps. In fact, three in four (70%) still believe that going into a branch to open an account is more secure.

This is the green flag for organisations to shout about how they are protecting their customers from fraud. With £651 million of unauthorised fraud stopped in the first six months of 2023, the increased levels of security that financial institutions have implemented are making a difference. For the people they serve, these details matter.

Customers are, of course, noticing the increase in checks while making online purchases (66%). More than one in two (57%) have seen it when logging into their bank accounts. However, as long as fraud checks are appropriate and proportionate to each individual and interaction, they are not always translating into a negative customer experience.

In fact, they are often helping to build a positive digital experience, giving customers the sense of protection they need. For example, 47% of consumers would be willing to answer up to 10 questions during an application process and two thirds of the population (66%) would be prepared to spend up to 30 minutes on a current account application. It’s worth noting, however, that if the process takes any longer than this or requires more questions, the likelihood of them giving up on the process is high.

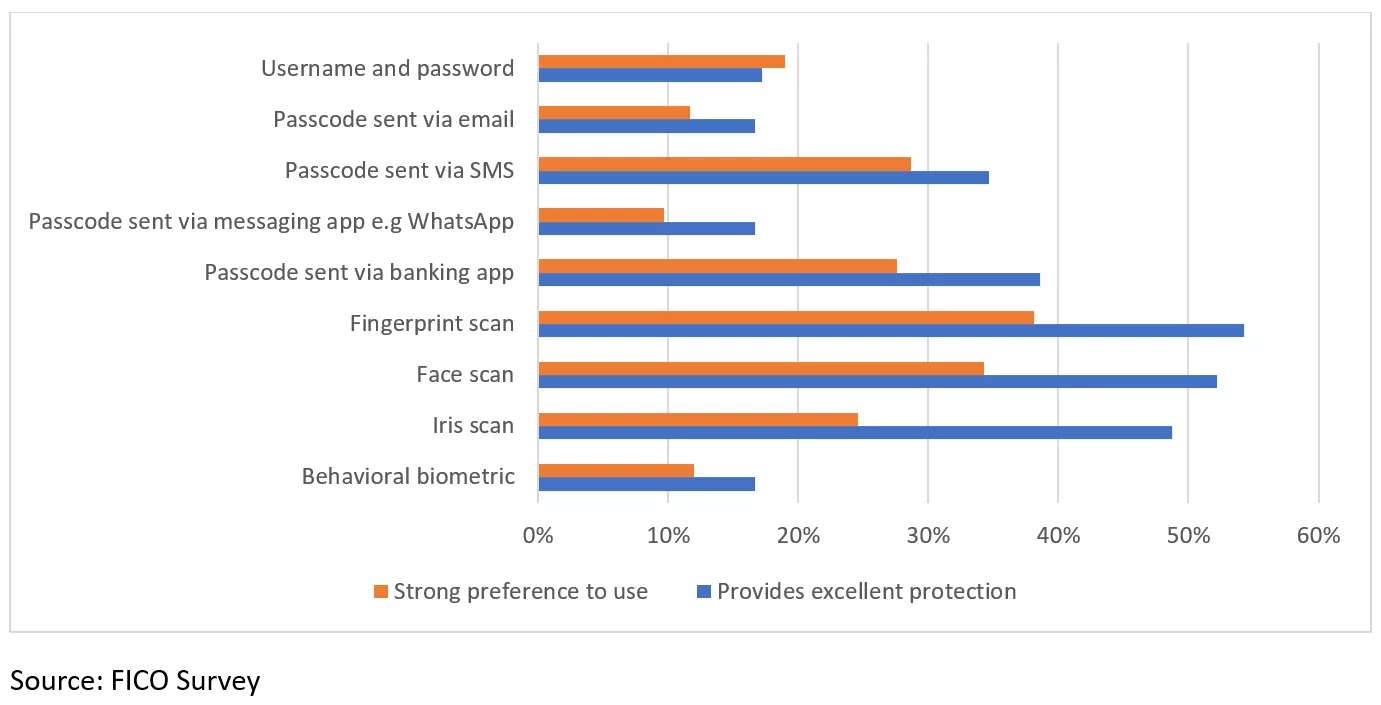

It’s also worth noting customer preferences and views on the relative effectiveness of identity solutions. For example, when making online payments, username and password are still widely used and considered good or excellent in terms of security by 61% of consumers. However, there is a very strong and growing preference for the use of biometrics, despite their historically controversial position. Far more consumers, 87%, believe that finger scans are good or excellent for security; 83% believe the same for face scans and 74% for iris scans.

When Strong Fraud Prevention Clashes with Convenience

There is a clear and growing appreciation for effective fraud prevention strategies among consumers, but they still want, and expect, to access accounts as quickly and as painlessly as possible. Good fraud protection, however, has been known to clash with demand for accounts that are easy to access and use.

This is because, while fraud prevention is a vital part of the process to onboard new customers in most organisations, fraud departments operate separately with their own processes which are simply ‘layered on’ to other processes. Information is not shared, nor is it brought together with data from other point solutions and data providers g to create a single decision that gives appropriate weight to all the information. The result for the consumer is a poor experience, repeatedly being asked to provide the same information.

For financial institutions, it means elevated costs due to the unnecessary level of extra checks taking place, increased fraud risks due to the lack of information shared and increased risk of irritating and losing those customers.

Our research has shown that 18% of consumers would abandon a current account application or reduce their use of an account if identity checks were too difficult or time-consuming.

It is worth noting, however, that this is an improvement from the 25% abandonment rate we saw in our survey the previous year and suggests greater tolerance of and appreciation for fraud prevention strategies – as long as they are proportionate and personal to each customer and interaction.

The fact remains, however, that there are no second chances with customers that have abandoned a process. They are not coming back, so there is still a need to pinpoint when people are abandoning and why.

Organisations should consider altering the order in which checks are made and use orchestration to determine which solutions are most appropriate to the unique circumstances of each verification. They should also introduce two-way, automated, but personalized and timely, communications about the process to help applicants overcome difficulties and encourage them to complete.

Conclusion – Fraud Prevention Is a Selling Point, not an Overhead

Fraud prevention has always held importance when it comes to who people choose as providers, but it hasn’t always been the driving factor. This is now changing and fraud prevention is increasingly taking a front seat in the minds of consumers.

However, when fraud protection works separately from the rest of the originations process, it creates inefficiencies that increase cost and duplications that frustrate customers. Although tolerance levels are higher than they have in previous years, they are still fragile. The reality is that there is only so much friction customers will accept.

To work well, fraud strategies must be integrated and managed from a single API-first applied intelligence platform (such as FICO Platform) that can orchestrate their use and supplement them with core competencies and vital data from specialist solutions.

That’s when organisations will be able to appreciate the hero that fraud prevention strategies truly are.

How FICO Helps

- Read more results from the UK Survey on fraud and digital banking

- Understand how FICO helps financial institutions balance fraud prevention and customer experience

- Learn how to break down the siloes between application fraud and originations

- Read the white paper The changing face of application fraud

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.