UK Cards: Signs of Risk in Rising Balances

FICO’s data on UK credit cards for July 2025 shows a YOY growth in balances and delinquent balances

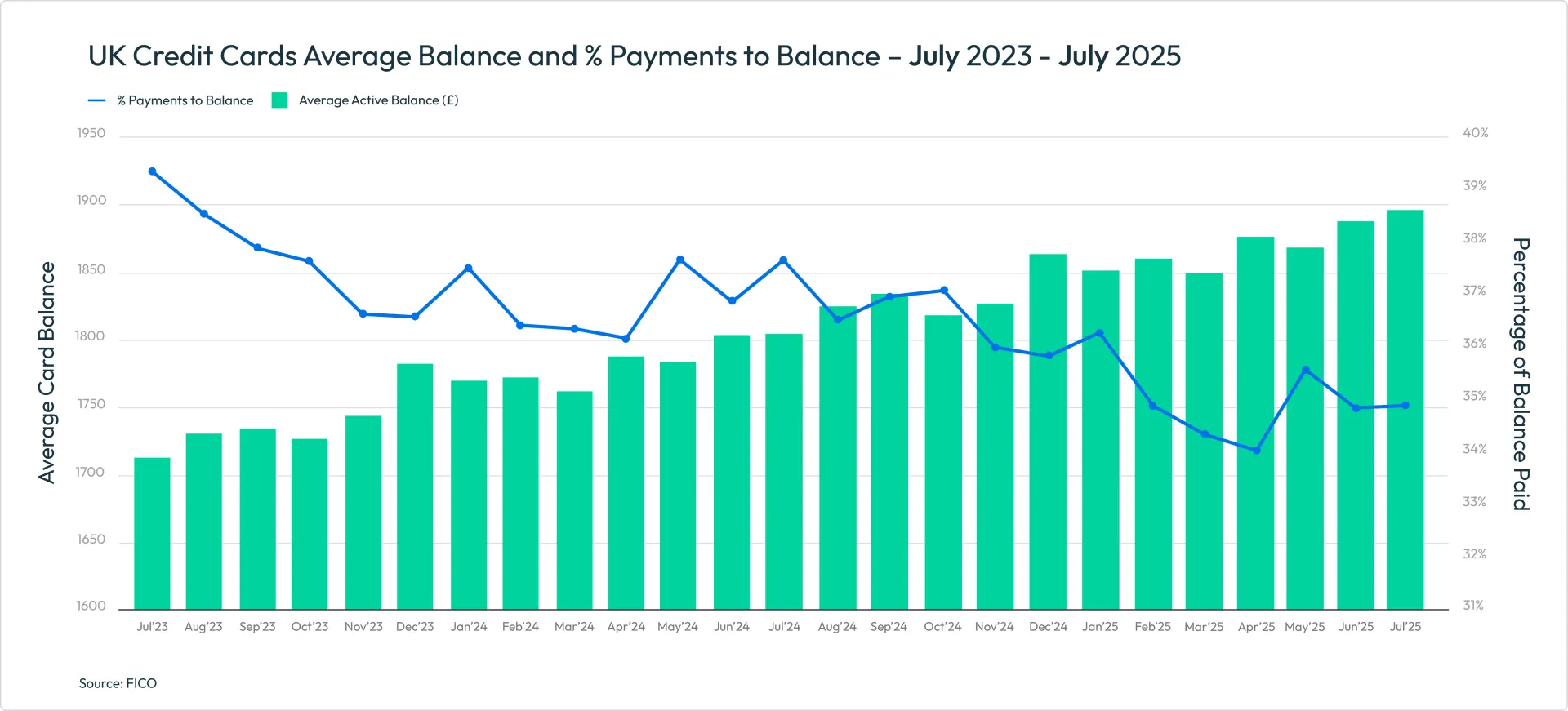

Credit Card Risk Trends and Payment Patterns in UK Cards - July 2025

In our review of our data on UK credit card performance, one thing that stands out as a concern is the increase in the average active balance on UK credit cards. Despite a typical seasonal reduction in spending, balances grew to £1,895, 5.1% higher year-on-year. Also, the percentage of the balance being paid off by customers fell year-on-year by 7.7%.

These figures reflect the affordability challenges many UK consumers face. What does this mean for banks and other card issuers? To manage this risk and support good customer outcomes, it’s vital to focus on limit strategies and the identification and treatment of customers in the early stages of financial difficulties.

UK Credit Cards in July - Highlights

- Spending decreased to an average of £800 in July, 2.9% lower than the previous month and 1.6% lower year-on-year

- Average balances continued to move up, rising by 0.4% month-on-month and 5.1% year-on-year

- The percentage of balance paid fell by 7.7% year-on-year to 34.9%

- 10.1% more customers missed one payment compared to June 2025, with the average balance 6.4% higher than July 2024 at £2,385

- The average balance for customers with two missed payments increased 6.9% year-on-year to £2,875

- The average balance for customers missing three payments increased 3.1% month-on-month and 8.1% year-on-year to £3,300

Key Trend Indicators UK Cards – July 2025

| Metric | Amount | Month-Month Change | Year-Year Change |

| Average UK Credit Card Spend | £800 | -2.9% | -1.6% |

| Average Card Balance | £1,895 | +0.4% | +5.1% |

| Percentage of Payments to Balance | 34.87% | +0.1% | -7.7% |

| Accounts with One Missed Payment | 1.39% | +10.1% | -10.0% |

| Accounts with Two Missed Payments | 0.31% | -1.0% | -5.1% |

| Accounts with Three Missed Payments | 0.20% | +8.0% | -5.1% |

| Average Credit Limit | £5,875 | +0.1% | +2.8% |

| Average Overlimit Spend | £90 | 0% | +1.1% |

| Cash Sales as a % of Total Sales | 0.86% | -1.5% | -4.5% |

Source: FICO

UK Credit Cards – Spending and Missed Payments

Following the peak in June, spending on credit cards fell to an average of £800 in July. While a drop in spending is typical at this time of year, the fact that it is 1.6% lower year-on-year could reflect overall pressure on consumer finances.

Another area of concern for financial institutions is missed payments. Year-on-year there has been a drop in the number of customers missing payments. However, the average missed payment balance continues to trend upwards.

The percentage of customers missing one payment continues to be erratic. After June’s 11.3% drop, July saw a 10.1% increase to 1.39%. Year-on-year, this equates to a 10% decrease. The number of customers missing one payment has been trending down over the last 12 months.

The number of customers missing two payments has been steadier, standing at 0.3% in July, a 1% decrease month-on-month and a 5.1% decrease year-on-year. While average balances on these accounts were slightly down month-on-month by 0.4% to £2,875, this is 6.9% higher year-on-year. Average balances for customers with three missed payments rose by 3.1% month-on-month and 8.1% year-on-year to £3,300.

With the average balance of customers with three missed payments increasing by 3.1% month-one-month and 8.1% year-on-year to £3,300, lenders will also want to review collections prioritisation strategies to support those customers with higher outstanding balances.

When comparing delinquent balance rates to the overall balance, this ratio is gradually increasing for customers missing one payment or two, with a more apparent trend upwards for those missing three payments. Risk teams can help to mitigate this by reviewing credit card limits to ensure that those accounts more at risk of missing payments are not offered limit increases.

UK Credit Cards – Cash Withdrawals

An important warning indicator of potential financial stress, the percentage of customers using credit cards to take out cash continued to rise. Typical of the summer months, it increased 1% month-on-month to 3.21%. It is expected that cash usage on cards will continue to increase again in August and September before dropping back down during the autumn.

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80% of UK card issuers. For more information on these trends, contact FICO.

How FICO Can Help You Manage Credit Card Risk and Performance

- Explore our solutions for customer management

- See my post on UK Credit Card Trends 2023-2024: More Spend and Delinquencies

- Read more posts on UK cards

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.