What June Data Says about UK Credit Cards and Consumers

Rising spend and falling payments to balance continued to push up average balances on UK credit cards, demonstrating underlying risk

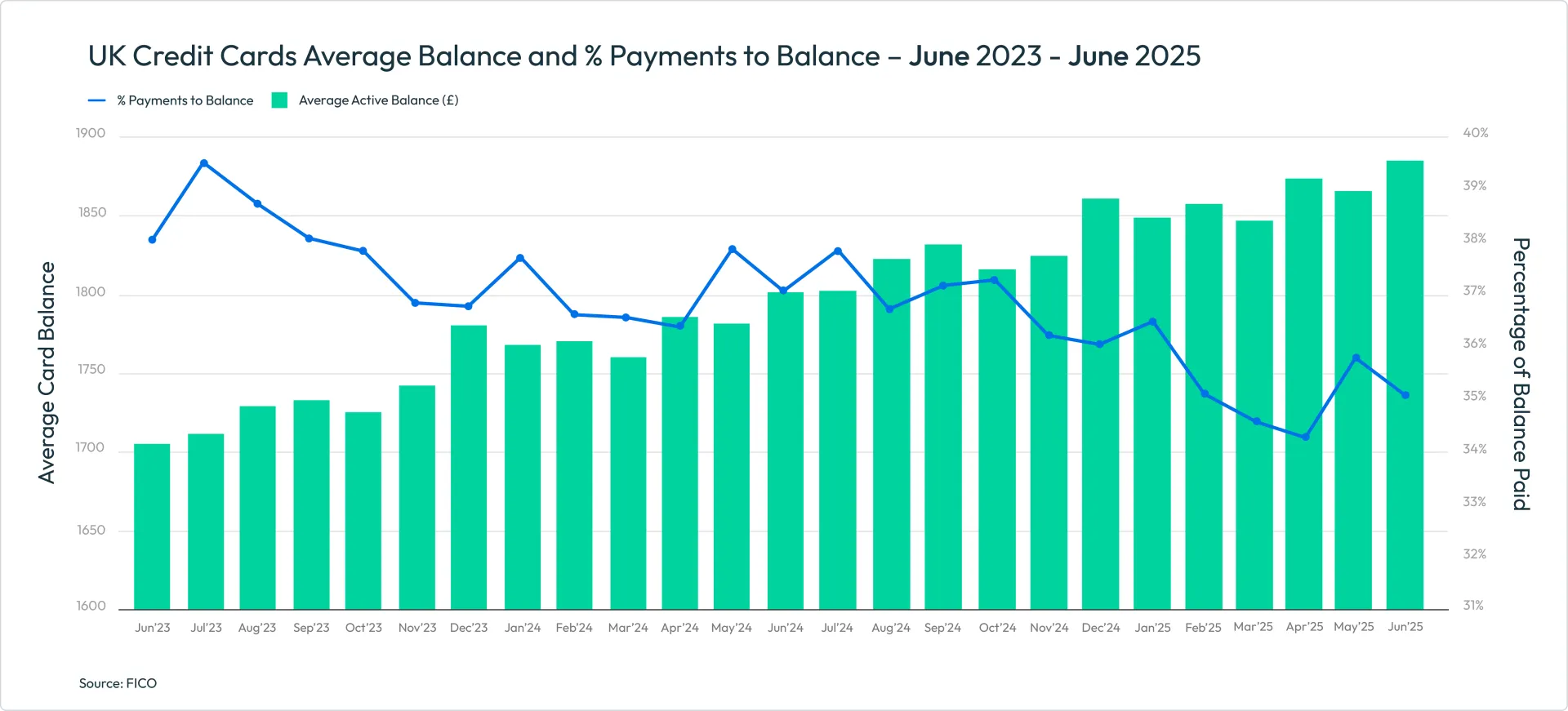

Our latest data on UK credit cards shows how rising spend and falling payments to balance are continuing to push up average balances. Increased spending follows expected seasonal trends, but the percentage of balance paid continues to trend downwards, which will be a concern for lenders.

- Spending rose by 4.6% month-on-month to £825, although was 1.4% lower than June 2024

- Average balances continued to trend upward, reaching £1,885 — 1% higher than May and up 4.6% year-on-year

- The percentage of payments to balance dropped 2.1% month-on-month and 5.7% year-on-year

- Customers missing one and three payments fell month-on-month while those missing two payments rose compared to May

Key Trend Indicators UK Cards – June 2025

| Metric | Amount | Month-Month Change | Year-Year Change |

| Average UK Credit Card Spend | £825 | +4.6% | -1.4% |

| Average Card Balance | £1,885 | +1.0% | +4.6% |

| Percentage of Payments to Balance | 34.83% | -2.1% | -5.7% |

| Accounts with One Missed Payment | 1.26% | -11.3% | -16.8% |

| Accounts with Two Missed Payments | 0.31% | +5.8% | -1.9% |

| Accounts with Three Missed Payments | 0.19% | -11.8% | -4.8% |

| Average Credit Limit | £5,870 | +0.3% | +2.9% |

| Average Overlimit Spend | £90 | -3.2% | +5.8% |

| Cash Sales as a % of Total Sales | 0.88% | +2.8% | -3.7% |

Source: FICO

Spending Patterns on UK Credit Cards

While spend in June 2025 has followed typical summer patterns to increase month-on-month, it is still 1.4% lower than the same month last year. This provides clear evidence of the lack of consumer confidence in the UK economy. The fact that average balances are continuing to trend upwards while the percentage of balance paid continues on a downward trajectory further underlines the financial balancing act being played out in UK households.

Missed Payments and Average Balances Trends

Another factor is the pattern of missed payments and average balances across the first half of the year. This has been erratic, but the percentage of customers missing one payment is trending down overall, with June seeing a monthly drop of 11.3% and an annual drop of 16.8%. The percentage of customers who missed three payments also fell month-on-month in June by 11.8% month-on-month, and is 4.8% lower than June 2024. The percentage of customers missing two payments has, however, risen month-on-month by 5.8%; it is 1.9% lower than in June 2024.

Average balances on accounts with one or two missed payments also continue to trend up. For one missed payment, the average balance is now £2,395 — 0.6% higher than May and 7.2% higher than June 2024. For two missed payments, the average balance is £2,885 — 2.9% higher month-on-month and 7% higher year-on-year. Average balances for three missed payments continued on a downward trend seen since March, by falling 0.3% month-on-month; however, they are 4.9% higher than in 2024 at £3,200.

Cash spend on credit cards also continues to increase. Whilst, again, this follows typical patterns, with a 2.8% increase month-on-month it is another factor lenders will want to consider in managing vulnerable customers. Trending up since March, cash usage is expected to continue increasing until September.

Focus for Card Issuers

As FICO data shows early-stage average missed payment balances continuing to trend up, card issuers should focus on early detection and specialised contact treatment, particularly for those customers who are especially vulnerable to the continued high cost of living and year-on-year inflation increases. These customers may also be struggling with Buy Now Pay Later payments, as affordability checks will only come under regulation in July 2026.

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80% of UK card issuers. For more information on these trends, contact FICO.

How FICO Can Help You Manage Credit Card Risk and Performance

- Explore our solutions for customer management

- See my post on UK Credit Card Trends 2023-2024: More Spend and Delinquencies

- Read more posts on UK cards

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.