UK Cards and Credit Risk: Further Decline in Balances Paid

April data on UK cards shows spending declined and average balances increased, signalling slow rise in credit risk for UK consumers

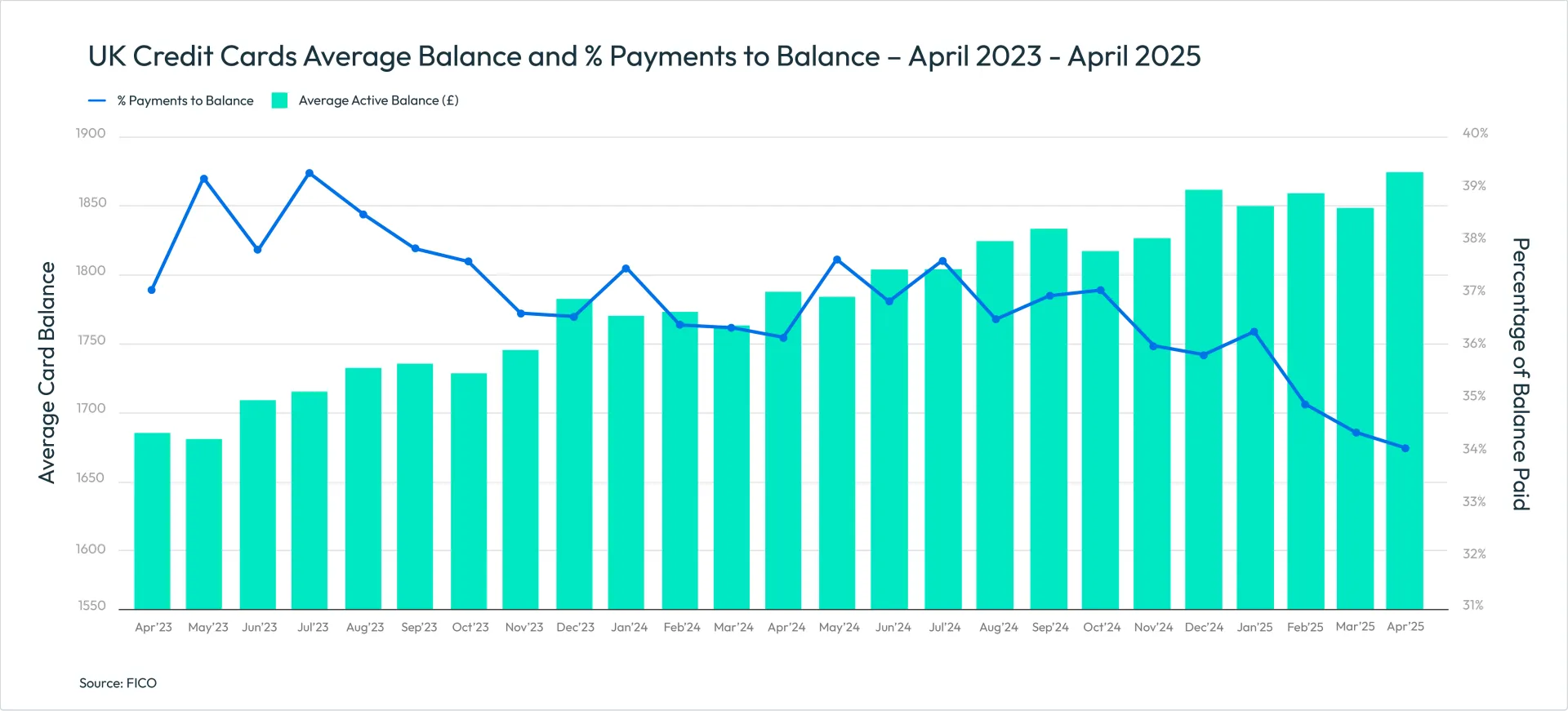

We saw the usual seasonal spending increase in April in the latest UK credit card data from the FICO Benchmarking Service, following a post-Christmas dip. However, spend was slightly lower year-on-year, reflecting continued financial pressures. The proportion of balance paid has also been trending downwards so far in 2025, and in April was 6.2% lower year-on-year. Combined with the impact of inflation, this meant balances were 4.9% higher than April 2024.

Here are some highlights of the report:

- Spending rose in April by 11.8% month-on-month, to £825 but was 0.5% down year-on-year

- Average balances rose by 1.5% on the previous month and 4.9% on the previous year, to £1,875

- Customers missing one credit card payment fell 22.1% month-on-month

- The average balance of accounts missing one payment is £2,325, 4.9% higher than April 2024

- The average balance for accounts with two and three missed payments was also significantly higher year-on-year, at 6% and 6.3% respectively

- The percentage of customers using credit cards to take out cash increased by 2.8% month-on-month after seven consecutive decreases, standing at 2.9% in April

Key Trend Indicators UK Cards – April 2025

| Metric | Amount | Month-Month Change | Year-Year Change |

| Average UK Credit Card Spend | £825 | +11.8% | -0.5% |

| Average Card Balance | £1,875 | +1.5% | +4.9% |

| Percentage of Payments to Balance | 33.98% | -0.9% | -6.2% |

| Accounts with One Missed Payment | 1.29% | -22.1% | -14.0% |

| Accounts with Two Missed Payments | 0.33% | +0.2% | -6.6% |

| Accounts with Three Missed Payments | 0.21% | -3.3% | -5.8% |

| Average Credit Limit | £5,845 | +0.2% | +3.1% |

| Average Overlimit Spend | £90 | -6.2% | +5.8% |

| Cash Sales as a % of Total Sales | 0.83% | -0.4% | -3.8% |

Source: FICO

Higher Balances, Lower Percentage of Balance Paid

What we saw in April reflects the continued pressure on household finances as overall credit card balances track higher year-on-year and average delinquent balances do the same.

Despite the seasonal drop in spending, balances increased by 1.5% month-on-month to an average of £1,875 – a 4.9% increase on the previous year. This measure continues to trend upwards.

Another signal of financial pressure is the percentage of balance paid, which has been decreasing since January 2025. Now standing at 33.98% it is 6.2% lower than April 2024 and 0.9% lower than March 2025. If this continues, it may reach pre-pandemic levels of around 30%.

Mixed Picture on Delinquencies

After the 23.1% month-on-month increase in March, the percentage of customers missing one payment has dropped by 22.1% in April, to 1.29%. This is also 14% lower year-on-year. Encouragingly, the large increase in the number of customers missing one payment in March has not carried through to customers missing two payments in April. At 0.3%, this is only a 0.2% increase month-on-month and is 6.6% lower year-on-year, indicating good collections practices. Just 0.2% of customers missed three payments, which is 3.3% lower month-on-month and 5.8% lower year-on-year.

However, the average balance for accounts with one missed payment increased slightly by 0.2% to an average of £2,325 in April, which is 4.9% higher year-on-year. Balances for accounts with two and three missed payments dropped month-on-month but remain higher than the previous year. The average two-cycle balance dropped 1.3% month-on-month and rose 6% year-on-year to £2,840. The average three-cycle balance dropped slightly by 0.2% to an average of £3,215, which is a 6.3% increase year-on-year.

Guidance for Card Issuers

In light of the latest FICO data, lenders will want to continue to review collections strategies, ensuring customers with higher balances at risk are prioritised and receive flexible and tailored treatment. They may also want to focus on those customers using their cards for cash withdrawals, as this can often be an early sign of financial stress.

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80% of UK card issuers.

How FICO Can Help You Manage Credit Card Risk and Performance

- Explore our solutions for customer management

- See my post on UK Credit Card Trends 2023-2024: More Spend and Delinquencies

- Read more posts on UK cards

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.