UK Credit Card Trends for September: Calm Before the Storm?

Monthly report on UK credit card trends shows financial prudence with spending down and percentage of payments to balance up – but will lockdown stashes save the day or fade away?

Our monthly UK Credit Market Report analyzing UK credit card trends for September 2021 shows the contrasting conditions that have been seen throughout 2021 continue. The month saw average spend fall, growth in payment levels and falling missed payment rates, all suggesting a current state of strong financial prudence. For lenders, however, focus needs to remain on reacting quickly to consumer changes in spend and payment behaviour which might indicate whether they can service their debt.

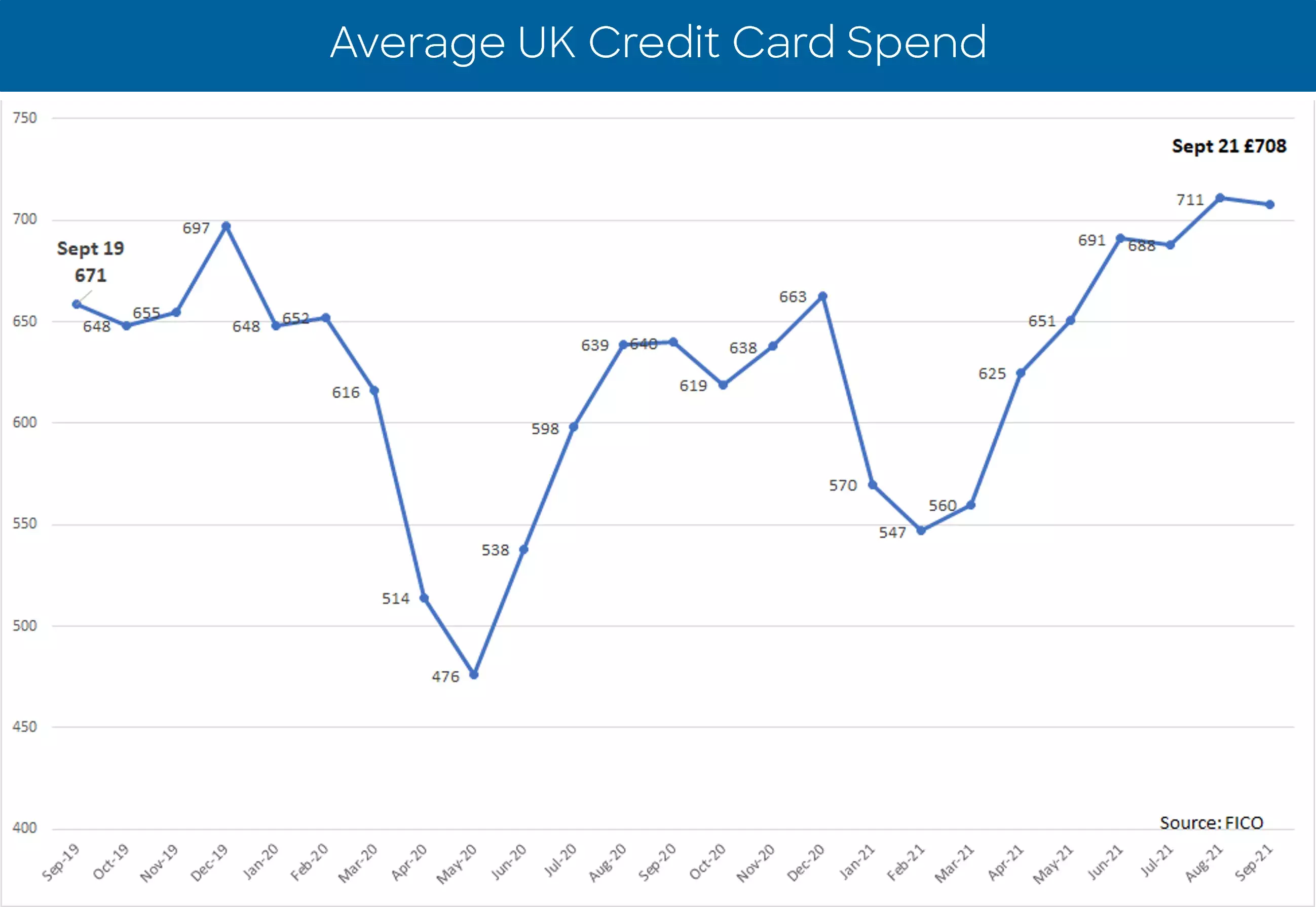

UK Card average spend falls for third time in 2021

The average spend on UK credit cards in September 2021 decreased £3 to £708. However, it was still £49 on September 2019, suggesting that consumers are still relying on lockdown savings.

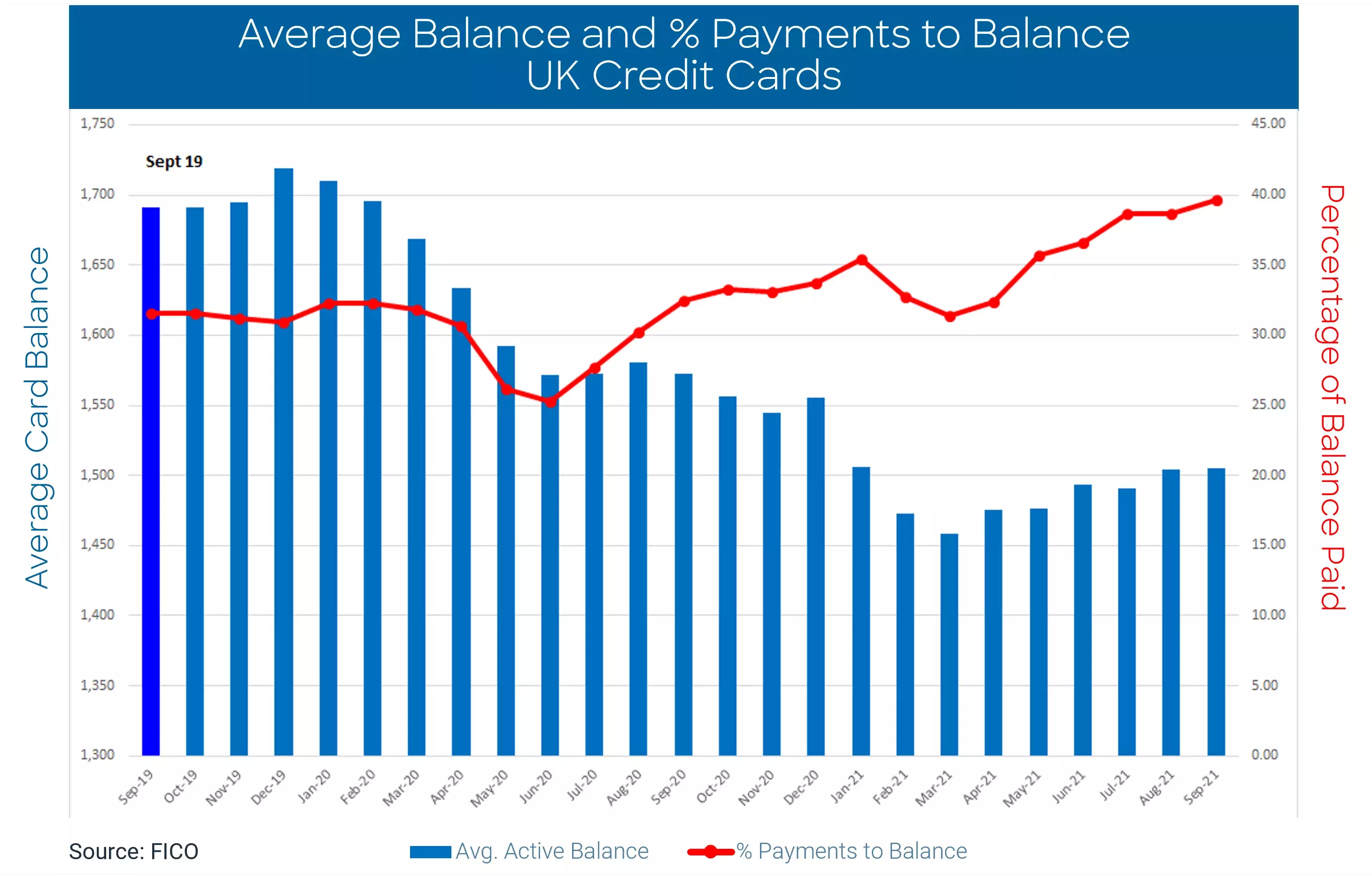

An eight-year high in percentage of payments to balance

Another indicator of the continuing role of pandemic savings is the eight-year high in the percentage of payments to balance. Year on year it is 22 percent higher and 26 percent above 2019 levels.

While average card balances grew £1 in September 2021, they remain 4 percent lower than a year ago and 11 percent below pre-pandemic levels (in September 2019).

This September, credit card holders moved from paying less than the amount due or the amount due to paying more than the amount due or the full balance (over a two-year high). This created the highest ratio of percentage of payments to balance in eight years.

Missed payment rates fall to new over two-year lows

The percentage of accounts missing payments fell 2.2 percent in September 2021. Their associated balance as a percentage of total balance decreased 2 percent, indicating the power of the savings and perhaps consumer restraint with an uncertain few months ahead.

The percentage of accounts missing payments is 30 percent lower than two years ago, and the percent of total balance is 17 percent below.

Only average balances on accounts missing one payment increased during the month, although these were 3.1 percent below September 2019. However, average balances on card users missing two or more payments are above pre-pandemic levels.

Compared to September 2019:

- Average balances for cardholders with two missed payments are 7 percent or £150 higher.

- Average balances for cardholders with three missed payments are 16 percent or £404 higher

- Average balances for cardholders with four or more missed payments are 15 percent or £406 higher.

This indicates that although a lower proportion of consumers are missing payments, those that do have higher average balances.

Spend over card limit stabilises

Compared to two years ago, far fewer cardholders are spending over their card limit, but those who do are spending even more over their limit than cardholders in September 2019. The percentage of accounts going over their limit stabilised, perhaps due to the drop in average spend, and remains 54 percent below September 2019 levels. The average amount being spent above limit remained the same month on month, however this is 12 percent higher than two years ago.

Cash usage long way from reaching pre-pandemic levels

The percentage of consumers using cash on their credit cards increased a further 7 percent in September 2021. However, cash usage is still 56 percent lower than pre-pandemic levels.

Looking ahead

October could be a pivotal month in consumer spending and payment behaviours. It was the first month with no furlough support and also marked the end of extra benefit payments, plus the increase in the energy cap level and continuing rises in fuel and food prices are all likely to have an impact. The contactless limit increase that was implemented mid-month, from £45 to £100, may also influence consumer use of credit.

Although lenders will be working on their 2022 strategic approach and perhaps getting back to business as usual in customer management, collections will remain at the forefront, along with ensuring any available or new credit is affordable for their customers.

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80 percent of UK card issuers. Issuers wishing to subscribe to this service can contact staceywest@fico.com.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.