5 Keys to Redefining Originations in a Digital-First World

How leading financial institutions are transforming originations to win customers, grow portfolios, and stay ahead of risk and fraud

For credit and lending leaders, the originations process has never carried more strategic weight. Today's applicants arrive shaped not by their last branch visit, but by every seamless digital experience they have ever had, from a one-click purchase to an instant streaming subscription. They expect speed, personalization, and a process that simply works. Research shows that nearly a quarter of consumers will abandon opening an account entirely if it feels too slow or cumbersome and, in a market where digital-native challengers are raising the bar on experience, that abandonment is rarely temporary. How well will your credit and loan origination software perform in this environment?

Key Takeways

- Real-time, connected data is the new decisioning baseline.

Fragmented, batch-driven data environments are no longer just a technical limitation, they're a competitive disadvantage. Leading institutions are moving to open ecosystem architectures that simultaneously ingest signals from multiple sources at the moment of decision, producing a more complete picture of the applicant without adding latency to the application journey. - Offer precision matters as much as approval speed.

In a market where applicants have abundant choices, the wrong offer is nearly as damaging as a rejection. Machine learning and mathematical optimization working together allow institutions to evaluate the full range of offer combinations in real time, balancing customer value, risk appetite, and portfolio constraints rather than defaulting to static policy tiers. - Fraud and credit risk need to be addressed in unison.

With synthetic identity fraud going undetected in 95% of onboarding cases and deepfake attempts up over 2,100% in three years, institutions that treat fraud and credit risk as separate workstreams are paying a compounding price. A unified decisioning layer where fraud signals, identity verification and credit assessment inform each other in real time improves accuracy across both dimensions without degrading the experience for legitimate applicants. - Agility and speed are key differentiators.

Fast decisions are table stakes for the borrower experience. What separates leading institutions is the ability to change credit policy in days rather than months, launch new product variants rapidly, and respond to regulatory shifts without rebuilding decisioning infrastructure. As Nationwide Building Society demonstrated, cloud-native platforms can cut strategy deployment time by 50% while preserving the governance and auditability that regulated lenders require.

The technology to get this right consistently, and at scale, exists today. The challenge, for many institutions, is knowing where to focus. What follows are five insights, built on decades of deep expertise in originations and a clear view of where the industry is heading. They define how leading financial institutions are reimagining originations for the digital-first era.

1. Leaders Are Moving from Data Silos to Decision Ecosystems

The conversation around originations data has fundamentally shifted. Leading institutions are not just collecting more data sources; they are connecting all available data in real time, at the exact moment of decisioning, to inform and enhance originations. They are moving away from fragmented, siloed solutions toward an open decision ecosystem powered by integrations. This provides the ability to ingest signals simultaneously from credit bureaus, open banking data, alternative data sources, fraud decisions and outcomes, and internal data about individual behavior.

The result is a complete and holistic view of the applicant that enables better decisions without adding time to the process. Institutions still relying on sequential, waterfall data checks are not just slower, they are making decisions on an incomplete picture of risk. For new-to institution customers, where historical profiles are absent, real-time data acquisition and alternative data signals bridge the gap, enabling equally informed, context-aware origination decisions. Institutions that have made this shift report a materially richer decisioning signal from day one of a customer relationship, without adding latency to the application journey.

2. The Right Offer at the Wrong Moment Costs You More Than a Declined Application

When a customer applies for a product, they expect a clear outcome: approved or declined, with limits and terms assigned. But modern originations don't stop at that decision — when an applicant doesn't qualify for what they requested, the ability to propose a credible alternative product, adjusted limit, or different terms can be the difference between losing a customer and gaining one.

Modern originations platforms apply machine learning and prescriptive analytics to evaluate the full spectrum of offer combinations in real time pricing, credit limits, product features, and terms surfacing the option that best balances customer value, portfolio profitability, and risk appetite.

FICO® Platform's AI & Analytics and Optimization capabilities work in tandem, with the former deploying fully interpretable, real-time models to assess risk and value simultaneously, and the latter applying mathematical optimization to ensure every offer is calibrated against the institution's actual portfolio constraints, not just a static policy rule. Prequalification strengthens this further, allowing institutions to extend confident, pre-assessed offers before a full application even begins, replacing guesswork with certainty from the very first touchpoint.

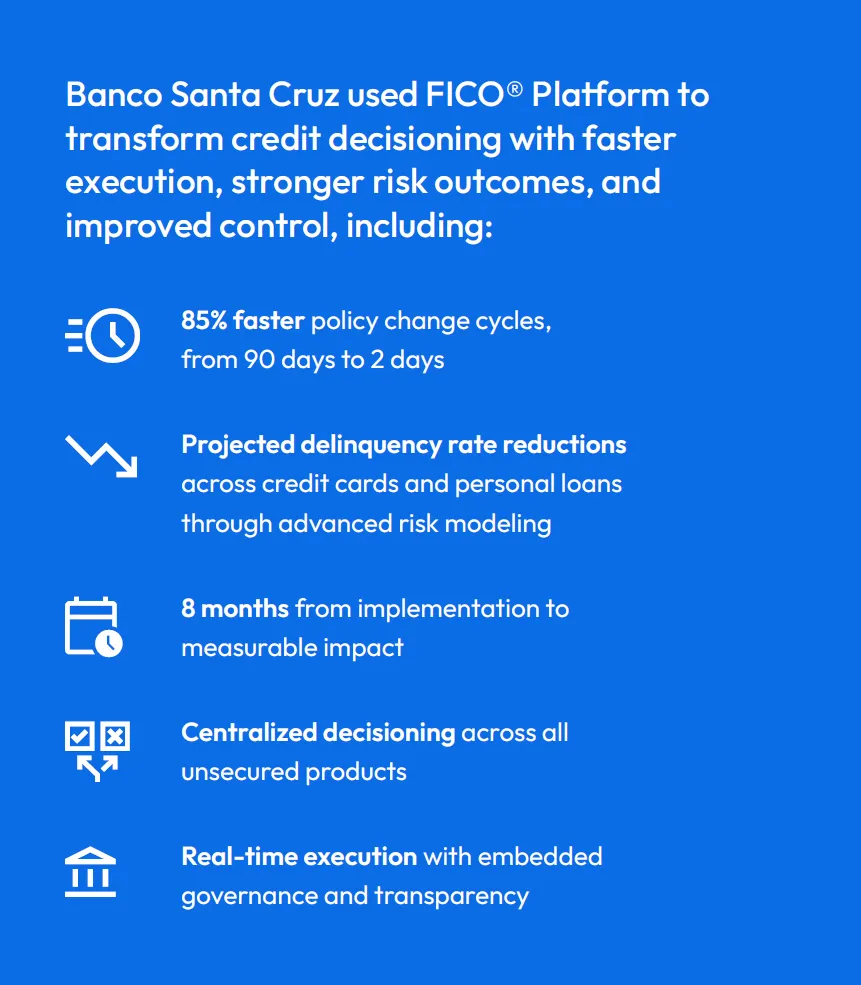

That was the case for Banco Santa Cruz, one of the Dominican Republic's largest private banks. Banco Santa Cruz partnered with FICO to modernize credit decisioning across its insecure portfolio. As a result, they achieved an 85% faster policy change cycle and reduced projected delinquency across unsecured portfolios in just 8 months.

3. The Fraud-Credit Risk Divide Is Costing You More Than You Think.

Decision outcomes in originations used to be primarily focused on credit risk conversations. That facet remains relevant, but it is now inseparable from an equally urgent one about fraud.

Application fraud has undergone a step change in sophistication. Synthetic identity abuse is estimated to go undetected at onboarding in approximately 95% of cases. Deepfake fraud attempts in financial services have risen by more than 2,100% over the past three years. And the overlap between fraud and credit risk is greater than many institutions recognize, as a fraudulent account is, by definition, a credit loss.

The institutions pulling ahead are those treating fraud detection and credit risk not as separate workstreams, but as a unified decisioning problem. FICO enables exactly this, bringing fraud signals, identity verification and credit risk assessment into a shared decisioning layer, so that each signal informs the other in real time. Coordinated decision logic improves accuracy across all dimensions simultaneously, without slowing the experience for most genuine applicants.

4. Speed Got You Here — Agility Is What Keeps You Ahead

Speed is a baseline expectation in originations. What separates leaders today is the agility of the system that produces the decision, the ability to adjust credit policies without a six-month IT project, launch a new product variant within days, and respond to regulatory change without rebuilding decisioning architecture from the ground up. Legacy infrastructure adds 20 to 30% to operational costs while simultaneously constraining the organization’s ability to adapt, which is a compounding disadvantage that grows more acute with every market cycle.

Cloud-native, composable platforms are closing that gap, and the evidence is increasingly concrete. Nationwide Building Society replaced its legacy mortgage decisioning infrastructure with FICO® Platform precisely to solve this problem, gaining the ability to adjust and deploy new decisioning strategies 50% faster than its prior architecture allowed, while maintaining the governance and auditability that a major mortgage lender demands.

Decisioning with FICO Platform puts strategy control directly in the hands of business users, reducing policy change cycles from months to days. Simulation allows teams to stress-test new credit strategies against real portfolio data before any live application is affected, so every policy change is validated.

5. The Application Is Over in Minutes — The Borrower Relationship Lasts Years

The question that defines competitive advantage in originations today is not whether the process is digital; it is whether it is designed to begin a relationship, not just complete a transaction. This means recognizing that friction is not always the enemy. The right level of identity verification, communicated clearly, builds trust rather than eroding it. It means every touchpoint during the application, from status updates and information requests to decision notifications, actively shapes the borrower's perception of the institution.

FICO® Platform's Omni-Channel Engagement capabilities ensure these interactions are consistent, personalized, and delivered on the channels customers use, not the channels most convenient for the lender. It also means that intelligence gathered at origination flows seamlessly into customer management and servicing through FICO® Platform's connected lifecycle architecture, so the institution's understanding of the customer deepens from day one rather than resetting at every subsequent interaction. The estimated 67% of banks that have lost clients due to slow and inefficient onboarding are a reminder of what is at stake when that foundation is poorly laid.

FICO Platform Addresses These Five Insights

Each of the five keys above addresses a distinct dimension of the originations challenge, but their true value is realized only when they work in concert.

FICO offers a modern approach to originations, built around an integrated decisioning view that delivers measurable results across the full originations chain. At its core is the ability to bring together data, intelligence and decisioning into a single, cohesive framework that operates in real time.

Rather than relying on fragmented or batch-driven processes, FICO enables institutions to seamlessly access and connect signals from across the ecosystem spanning credit bureaus, open banking, alternative data, fraud insights and internal behavioral data. This continuous flow of information ensures that every decision is informed by the most current and complete view of the customer, whether for an existing relationship or a new-to-institution applicant.

On top of this data foundation, advanced analytics and AI models translate raw signals into actionable intelligence, balancing predictive power with transparency and regulatory defensibility. Decisioning is no longer constrained by technology bottlenecks; instead, business users are empowered to adapt strategies quickly, test them against real-world scenarios, and deploy changes with confidence.

This integrated approach also enables institutions to orchestrate complex decision workflows at scale, while continuously optimizing outcomes across the portfolio. By validating strategies before deployment and solving trade-offs with precision, institutions can drive smarter, faster and more consistent origination decisions.

Learn More About How FICO Can Improve Your Originations

- Explore how Nationwide modernized mortgage decisioning with FICO® Platform

- See how Banco Atlantida achieved 100% digital onboarding automation through FICO® Platform

- Explore FICO solutions for originations

- Speak to a FICO expert about your originations challenges

Frequently Asked Questions

FICO® Platform's AI & Analytics and Optimization capabilities work in tandem to evaluate the full spectrum of offer combinations in real time (including pricing, credit limits, product features, and terms), surfacing the option that best balances customer value, portfolio profitability, and risk appetite, rather than defaulting to static policy tiers.

Yes. FICO® Platform brings fraud signals, identity verification, and credit risk assessment into a shared decisioning layer, so each signal informs the other in real time, improving accuracy across both dimensions simultaneously without slowing the experience for genuine applicants.

Nationwide Building Society achieved 50% faster strategy deployment after replacing its legacy mortgage decisioning infrastructure with FICO® Platform, while maintaining the governance and auditability requirements of a major regulated lender. More broadly, the platform reduces policy change cycles from months to days.

Intelligence gathered at originations flows seamlessly into customer management and servicing through FICO® Platform's connected lifecycle architecture, meaning the institution's understanding of the customer deepens from day one rather than resetting at every subsequent interaction.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.