The Hidden Costs of Friction: What 18,000 Consumers Revealed About Identity Verification and Account Origination

Our comprehensive survey uncovered striking regional differences in consumer priorities and behaviors, challenging conventional wisdom about what drives account selection

In today's digital-first financial landscape, the balance between security and customer experience has never been more critical—or more delicate. A new FICO global consumer survey reveals surprising insights about how identity verification processes can create expensive customer churn, costing financial institutions both revenue and relationships in ways many organizations may not fully recognize.

The Global Consumer Perspective: Security vs. Simplicity

Our comprehensive study surveyed approximately 18,000 consumers across 18 countries spanning APAC, EMEA, Latin America, and North America, uncovering striking regional differences in consumer priorities and behaviors. The findings challenge conventional wisdom about what drives account selection and reveal concerning trends about customer abandonment.

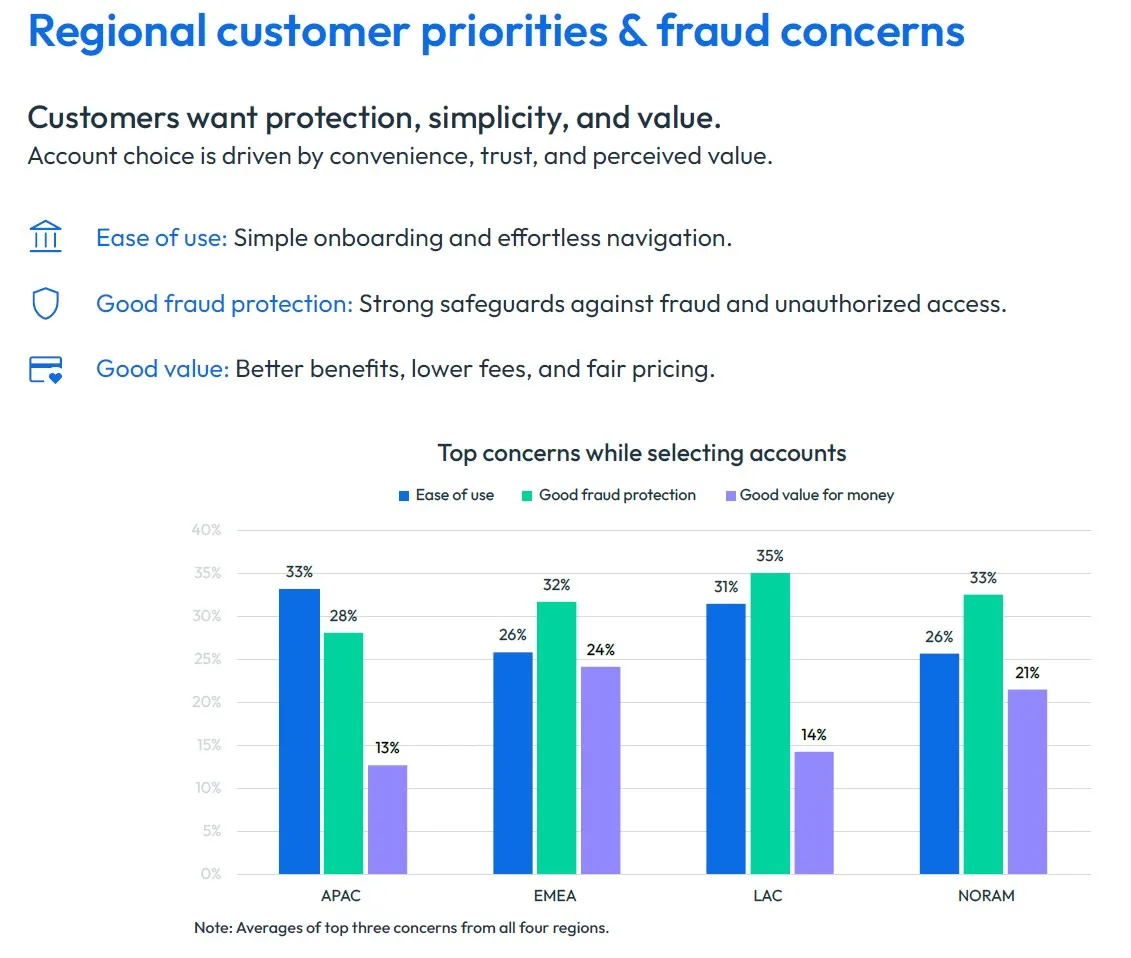

When choosing financial accounts, consumers consistently prioritize three key factors: convenience, protection, and perceived value. However, the weight given to each varies dramatically by region. While customers in APAC prioritize ease of use above all else, consumers in other regions place stronger emphasis on fraud protection as their primary deciding factor. This regional disparity has profound implications for how financial institutions should tailor their onboarding strategies.

Customers want protection, simplicity, and value led by:

- Ease of use: simple onboarding and effortless navigation

- Good fraud protection: strong safeguards against fraud and unauthorized access

Good value: better benefits, lower fees, and fair pricing

The Account Opening Opportunity Hiding in Plain Sight

Perhaps most intriguing is what our research reveals about customer abandonment during the account opening process. The data shows that complex identity verification procedures are creating significant friction at the worst possible moment—when potential customers are deciding whether to trust an institution with their financial relationship.

The abandonment rates vary considerably across different types of accounts and regions, with some account types experiencing particularly high drop-off rates. Personal bank accounts, representing the foundation of most customer relationships, show concerning abandonment patterns that should give every financial services executive pause.

But the problem doesn't end at account opening. Our research uncovered an equally troubling trend: customers who successfully navigate initial identity checks may later reduce or completely stop using their accounts if they perceive ongoing verification processes as too burdensome. There is tremendous opportunity for forward-thinking banks to win, retain, and protect customers with streamlined, safe, and intuitive account opening.

Financial Crime Fears Drive Contradictory Behaviors

Consumer attitudes toward financial crime reveal a complex psychology that institutions must navigate carefully. Customers fear financial crimes that can strike suddenly and cause direct financial loss that's difficult to reverse. Yet their concerns vary significantly by region.

Scams top the worry list in APAC at 33%, while identity fraud dominates concerns in LAC at 37%. Meanwhile, card misuse ranks highest among North American consumers at 23%. These regional differences suggest that one-size-fits-all approaches to security messaging and verification processes may be missing the mark.

Adding another layer of complexity, our research reveals that 7% of all global respondents believe their identity has definitely been used to open a financial account fraudulently, with the highest percentage occurring in North America at 9%. This statistic underscores why consumers demand robust protection—even as they simultaneously abandon accounts due to verification friction.

Application Fraud: Where Friction and Risk Collide

The consumer behaviors uncovered in our research play out against a backdrop of increasingly sophisticated application fraud. When individuals misrepresent their identity, inflate their income, or use stolen credentials to open accounts, they exploit the very same onboarding processes that frustrate legitimate customers. The irony is sharp: the friction that drives good customers away often fails to stop determined fraudsters.

Application fraud is multifaceted. Third-party fraud uses stolen or synthetic identities and is the variety most consumers picture when they think about identity theft. But our survey findings on income exaggeration hint at a murkier reality — first-party fraud, where applicants deliberately falsify their own information, is deeply intertwined with the "situational flexibility" attitudes our respondents revealed. And mule accounts, opened to move illicit funds, can slip through onboarding checks that prioritize speed over scrutiny.

Layering on more verification may catch more fraud, but our data shows it also pushes legitimate customers toward abandonment. Streamlining without intelligent risk assessment simply opens the door wider for bad actors. The institutions getting this right are moving toward orchestrated and adaptive approaches that calibrate friction to risk in real time — lighter-touch verification for low-risk applicants, escalated scrutiny where signals warrant it. Done well, this strengthens fraud prevention and customer experience simultaneously.

The Biometric Authentication Puzzle

Consumer attitudes toward biometric authentication present another fascinating paradox. While these technologies promise to reduce friction while maintaining security, our research reveals significant gaps between user preference and perceived protection across different biometric methods.

The data shows that consumer acceptance varies not just by technology type, but also by region, suggesting that deployment strategies for biometric authentication need to consider local preferences and cultural attitudes toward privacy and technology adoption.

The Trust vs. Convenience Dilemma

Perhaps most intriguingly, our survey uncovered attitudes toward income exaggeration that reveal the complex relationship between consumer behavior and institutional risk management. The findings show that consumer tolerance for "situational flexibility" varies dramatically across different types of applications and regional contexts.

These insights have profound implications for first-party fraud prevention, regulatory compliance, and the design of application processes that accurately assess consumer ability to repay while maintaining reasonable friction levels.

What This Means for Financial Institutions

The research reveals a fundamental challenge: consumers want both bulletproof security and frictionless experiences, but current approaches often force an either-or choice. The institutions that will thrive are those that can thread this needle—delivering robust fraud protection through intelligent, adaptive processes that feel seamless to legitimate customers.

The regional variations in consumer behavior and preferences also suggest that global financial institutions need more nuanced, localized approaches to identity verification and fraud prevention. What works in North America may drive abandonment in APAC, and vice versa.

The Path Forward

The full implications of these findings extend far beyond simple customer satisfaction metrics. They touch on fundamental questions of revenue optimization, risk management, regulatory compliance, and competitive positioning in an increasingly digital marketplace.

The complete research reveals specific strategies and technologies that can help institutions navigate these challenges while providing detailed benchmarks for understanding how your organization's performance compares to regional and global standards.

The future of financial services belongs to institutions that can master the art of invisible security—protection so intelligent and seamless that customers feel both safe and unencumbered. The question is: will your organization be among them?

Dive Deeper Into the Data

Download the full consumer insights infographic to explore detailed findings across APAC, EMEA, LAC, and NORAM, including specific metrics, regional comparisons, and strategic recommendations for balancing security with customer experience.

How FICO Can Help You Stop Fraud

- Understand more about modern approaches to enterprise fraud with the six E’s of enterprise fraud

- Explore our fraud solutions

- Explore our origination solutions

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.