Debt Collection and Debt Resolution in 2022

As we enter the third year of the global pandemic, what are the challenges facing debt collection and debt resolution professionals?

Now that we’ve turned the page on the calendar, and entered the third year of the global pandemic, what are the challenges facing debt collection and debt resolution professionals? I’ve been in the business for more than 30 years now, and while some of what I see is new, much of it is awfully familiar.

Stress on Household Wallets

Regardless of the billions in cash reserves governments have invested in furlough schemes, business loans, deferred repayments and debt relief schemes, the cost of living continues to rapidly increase. Energy and fuel price rises are now critical catalysts weighing on the level of disposable income within many financially stretched households.

At the same time, there’s a perfect storm approaching combining insolvencies, job losses, interest rate rises and fuzzy but significant consumer over-commitments, driven in part by the rise in prevalence of BNPL (buy now, pay later) schemes.

There’s also likely to be a longer-term impact on the housing market, as loan-to-value is squeezed and property affordability puts home ownership out of range for even more first-time buyers. At the same time, rising interest rates and continued uncertainty are likely to also push up private sector rents as buy-to-let mortgages become costlier.

Stress on Creditors — Situational and Regulatory

Lenders face several thorny challenges of sifting through the pandemic’s inevitable financial fall-out.

The ability to cost-effectively deal with persistent indebtedness while offering customers breathing space is vital, particularly as income support schemes are wound down. There is also unease around BNPL as a competitive offering to traditional credit markets, its impact on consumers and the ability to successfully spot over-indebtedness.

A mass of digital solutions and fintech innovations offering real-time Open Banking data alongside transactional insight into customer affordability and vulnerability are being touted to Tier-1 lenders. The headache is knowing where to make the big bets for the best return.

Regulation also continues to pose demands on already stretched back-offices juggling limited budgets, manpower and bandwidth challenges.

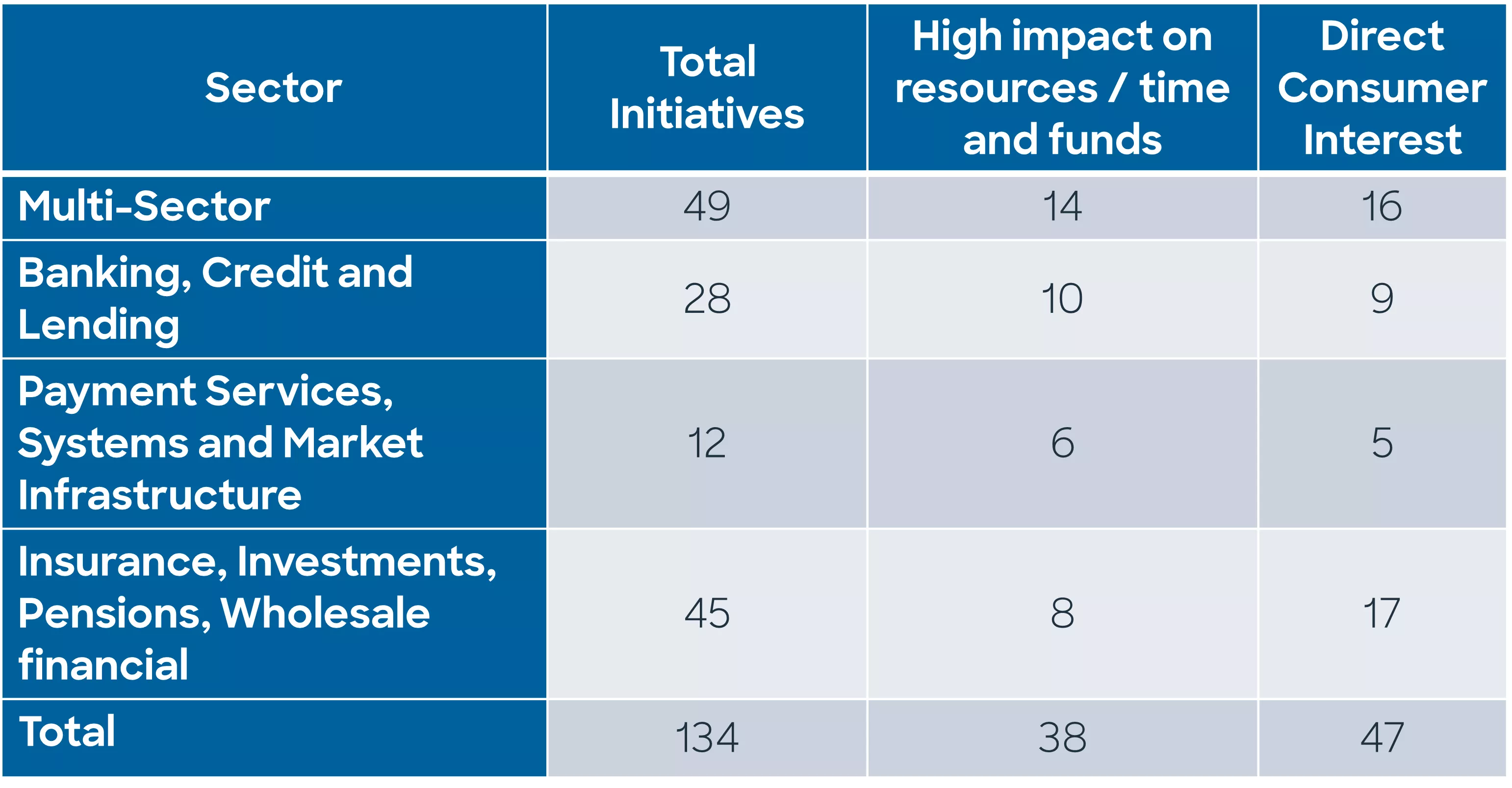

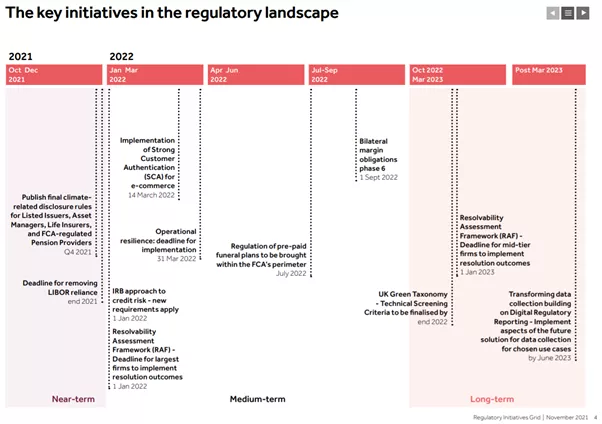

In the UK, for example, the FCA’s Regulatory Initiatives Grid details the in-flight and pending regulatory and industry-driven changes. In September 2020 there were 111 initiatives listed. In November 2021 there were 134 active initiatives listed.

The table below gives a summary of total initiatives by sector. The indicative impact is gained through institutional feedback to the FCA:

Other regions may not have the Initiatives Grid but they will have industry-level initiatives being originated and demanded by both local and “pan” organisations and authoritative bodies. For a periodical refresh on the number of initiatives the differing industries are grappling with, the Initiatives Grid is a decent reference.

https://www.fca.org.uk/publication/corporate/regulatory-intitiatives-grid-november-2021.pdf

Positive Signs for Debt Resolution

But beyond the challenges of regulatory change, it’s not all doom and gloom for lenders. Many consumers have been paying down debts; outstanding credit card debt decreased 3.7% in the year to Oct 2021 (The Money Charity, Dec 2021). there’s plenty of capital available and relatively modest collections portfolios, with most creditors reporting lower collections volumes than expected. Despite the challenges posed by the past three years, the broader economic outlook is positive. Lenders can take advantage by making a timely shift from a collections and recovery mindset to the delivery of more holistic customer support and debt resolution schemes. It’s a win-win for all parties, as I discussed in a recent webinar with McKinsey on digital-first collections.

Changing the Operating Model in Debt Collection

The expected debt tidal wave has so far been flattened, thanks to a combination of moratoria schemes and careful management – but are we at risk of complacency? How are lending appetites shaping among competitive Tier-1 banks and can they continue to be well-prepared for further surprises without ensuring the very best customer insights?

Will 2022 be the year when long-expected changes to collections industry operating models enjoy widespread adoption? It’s likely to pave the way for far shorter retention of in-arrears customers, a quicker hand-off to third-party debt resolution for delinquent accounts, and a more proactive approach to helping so-called ‘resolved customers’ being returned to the status of good customers. Lenders also look set to offer more frequent fire sales of non-performing loans (NPL) and non-performing exposures (NPE), to help keep portfolios healthy.

Technology and data sources are rapidly driving an ever-evolving back office for collections. Real-time access to ‘traditional’, new and emerging datasets continues at pace. Explainable AI, digital platforms and automation are all helping reduce overheads. But they are all critical investments that can be complex and time-consuming to set up. They also require talent and manpower to effectively deliver. Success hinges on the ability to parachute in expertise as needed when it comes to seamless installation and optimising operations.

Digital transformations for many have also progressed at pace during past 24 months – and are set to continue. As a result, the value of enhanced analytics is proven right across the enterprise Agility is now a mindset applied to all aspects of the business - not just IT implementation process – while everyone understands the benefits of improving customer journeys regardless of where they are on the lifecycle.

Right now, top performers are focussed on building agile, flexible and scalable capabilities. They’re less concerned about the accuracy of economic and behavioural forecasts than they are about ensuring they have the ability to handle whatever may come in a smart, expedient and appropriate manner.

How FICO Platform Can Help with Your Debt Resolution Results

- Discover how FICO’s debt resolution solutions can help you

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.