How Dynamic Profiles Turn Transaction Signals Into Real-Time Customer Intent

Dynamic profiles change how organizations model customers and their operating environment, without rewiring data flows

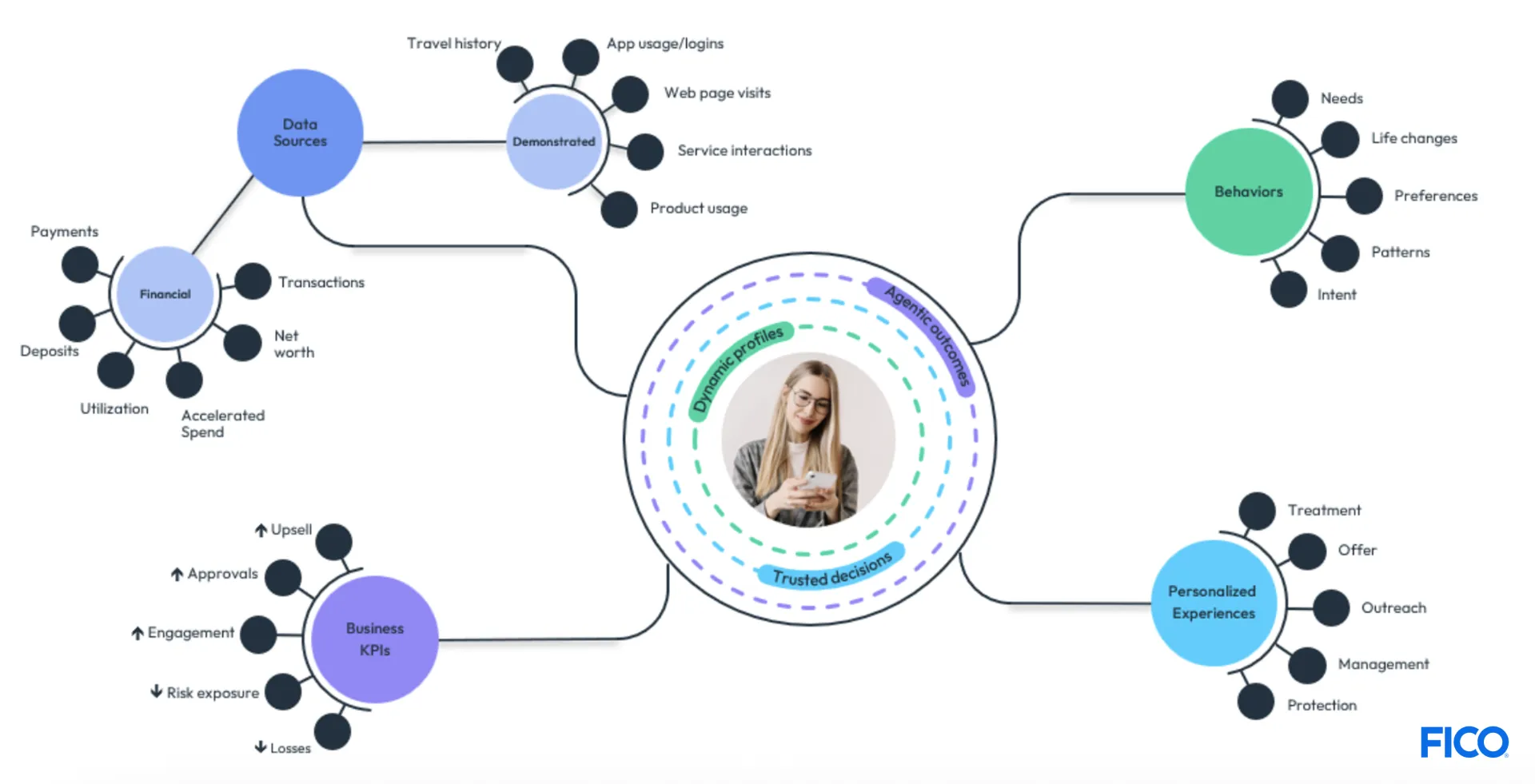

Financial institutions operate in environments where customer behavior, market conditions, and risk exposure shift with a single transaction. Yet many still rely on static customer models. They explain the past, but they miss what’s changing now. That gap makes timely, individualized experiences harder to deliver.

Consider one customer over two weeks: fewer logins, more failed authentication attempts, and a shift toward higher-cash withdrawals. Each signal alone is ambiguous. Together, they may indicate stress or scam exposure, especially when corroborated by changes in spending or payment behavior.

Dynamic profiling maintains an adaptive view of each customer, including signals, behaviors, context, and risk markers. It keeps decisions anchored in what’s true now, not the last stored snapshot. Profiles update as events occur, which support faster, more relevant decisions across channels without rewriting existing data flows.

Over time, patterns in transaction and engagement signals may also indicate intent, for example an intent to reduce spending, seek assistance, avoid fees, or switch providers.

This is the first of a three-part series on three pillars of the FICO Platform: dynamic profiles, trusted decisioning, and agentic outcomes.

The Limits of Static Understanding

Traditional architectures leave teams with siloed, point-in-time fragments of customer information. Signals land in different systems and only converge later, after key decisions. Each function captures what it needs, but the broader view of how a customer changes across time and channels is missing. The result is personalization anchored in averages and segments, not emerging individual patterns.

The constraint is rarely data volume. It’s building and keeping current a decision-ready context for each customer, product, and device across channels.

What changes when customer context stays current

To keep pace with changing behavior, organizations need profiles that update as events occur. In FICO Platform, these profiles are maintained for entities such as customers, merchants, accounts, and products, so decisioning has current context. In many cases, direction matters as much as current position. Trend and trajectory can be more informative than periodic snapshots.

Dynamic profiles are built for enterprise scale and governed, auditable decisioning. They provide a decision-ready layer for front-office moments where batch persistence is too slow.

Maintain current context for each entity (not just a stored record).

Run low-latency analytics at high throughput.

Adopt incrementally by tapping existing pipelines and processing events in parallel.

The result is a decision-ready layer that connects real-time operations with analytical and back-office systems, without replacing existing infrastructure.

What this enables in practice

The value shows up in outcomes. When context updates continuously, decisioning identifies risks and opportunities earlier and acts sooner with better-timed next-best actions.

For example, a sustained drop in deposit inflows or a shift in payment patterns may signal affordability pressure or rising attrition risk before delinquency or churn. Teams typically validate those signals with additional context, such as changes in utilization, repayment behavior, or channel activity. Static back-end systems often detect the shift too late, which forces reactive interventions.

Personalized engagement depends on context. In a broader view of the customer, transaction data informs timely, tailored offers and interventions. Patterns in spend concentration, frequency, and average ticket size reveal needs and sensitivities and support higher lifetime value.

A FICO survey found that 91% of people believe customer experience is just as important, if not more important, than a bank’s products and services. Tracking intent as it changes aligns actions to observed behavior, not assumptions.

How teams adopt it without disruption

Organizations can adopt dynamic profiles incrementally. One approach is to tap existing pipelines and stream events through FICO Platform so profiles accumulate and refresh context over time.

In regulated industries, this modernizes decisioning while preserving governance, auditability, and stability.

Where this goes next

FICO is recognized as a Leader in the 2026 Gartner® Magic Quadrant™ for Decision Intelligence Platforms. In practice, decision intelligence depends on unifying fragmented signals and supporting decisions as behavior unfolds.

In the next posts in this series, trusted decisioning and agentic outcomes build on this foundation and move from reactive analysis to continuous action.

For technology leaders, the question isn’t whether customer understanding is dynamic. It’s whether your approach can model reality as it changes. Teams that modernize how they represent behavior are better positioned to adapt in complex environments.

Next: trusted decisioning.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.