Your Customer’s AI Agents Are Coming – Are You Ready?

Agentic AI opens up a new world for customer interactions, and banks need the right capabilities to respond

Key Takeaways

- Your customers' AI agents are already knocking on your door.

Agentic AI isn't a future concept — it's arriving now. Customers' AI agents will autonomously shop for loans, negotiate terms, move funds, and switch providers in seconds. The real competitive question for banks is no longer whether they have AI, but whether their systems are equipped to meet and respond to a customer's agent intelligently and in real time. - Traditional customer loyalty is eroding fast — and AI accelerates that.

With switching at a ten-year high, $11 trillion in US household wealth at risk, and 62% of Gen Z and Millennials willing to trust non-bank AI platforms for financial services, loyalty can no longer be assumed. When AI agents strip away the friction that once kept customers in place, banks compete purely on the quality and speed of their offers. - Agentic AI transforms how banks run their businesses internally, not just how they serve customers.

Agentic AI compresses the cycle time between knowing and acting — from weeks to minutes. Anomalies are detected as they happen, experiments are designed automatically, and deployment happens in seconds. This is a fundamental shift in how institutions operate, not simply a faster version of the status quo. - Governance and traceability aren't optional extras — they're the foundation.

With banking penalties up 522% in 24 months and 42% of organizations saying AI is outpacing their governance, speed without accountability is a liability. Every automated decision needs to be auditable, attributable, and built on encoded policy rules. Banks that build agentic capabilities on a governed, traceable platform from the start will be far better positioned — both competitively and with regulators — than those trying to retrofit compliance later.

We are living through a period of technological acceleration unlike anything in human history. At FICO World 26 in May, FICO President of Software Nikhil Behl opened his keynote address with a striking sequence of numbers that framed the scale of the shift underway. It took 50 years for the telephone to reach 100 million users, 20 years for the television, and 5 years for the mobile phone. ChatGPT did it in just two months . Today, AI systems are processing 2.5 billion prompts every single day — and Google's AI alone processes 1.3 quadrillion tokens per month.

"We are in a period of acceleration that has no precedent in human history," Behl told the audience. "The question for every person in this room is simple: Are you moving fast enough to lead it — or will it lead you?"

For banks, that question is no longer hypothetical. It is here — and it looks like an AI agent.

Meet the Customer’s AI Agent

To illustrate the point, Behl introduced his own AI agent on stage — a version of himself that, while he was preparing his keynote, had reviewed his financial accounts across three institutions, identified a higher yield on his savings, negotiated terms with two banks' AI agents, and moved $25,000 to a new account earning an additional 1.2% APY. It had also flagged an insurance renewal priced 15% below market and queued alternatives for review. The entire interaction with his bank — involving a risk agent, a fraud agent, a retention agent, and a customer growth agent — took just four seconds.

This is not a distant scenario. It is already the direction of travel. As Behl put it, "The question isn't whether your customers will have an agent. It's whether that agent prefers your bank."

The scale of what's coming is significant. By the time of the next FICO World, Behl projected that 40% of attendees will be using AI agents — and from there, the numbers grow rapidly: thousands, then millions, potentially billions, with agents creating agents and supervisory agents managing entire networks. Yet today, only 14% of organizations have a system or governance in place to manage this.

Younger People Are Ready Now to Use AI Agents

The customer dimension makes this still more urgent. 86% of consumers say they would trust their main bank to deliver an AI assistant — but 62% of Gen Z and Millennials would also trust other generative AI platforms to deliver banking services. Loyalty, already under pressure, is being fundamentally reshaped. Nearly three-quarters of your customers already bank with your competitors, switching is at a ten-year high, and $11 trillion in household wealth is at risk in the US alone. When AI agents remove friction from financial decisions, brand loyalty disappears with it.

And then there is the generation coming up behind all of this. "This is a generation that won't open your app," Behl observed. "They'll ask their agent." A third of young adults are already turning to AI for advice on life decisions — these are tomorrow's banking customers, and they will interact with financial services entirely on their own terms, through their agents.

Three forces are converging simultaneously: the rapid scaling of agentic AI, intensifying regulatory complexity, and the erosion of traditional customer loyalty. Banking penalties surged 522% in 2024, and 42% of organizations say AI is advancing faster than their governance can keep pace. As Behl made clear, solving any one of these pressures in isolation is no longer enough.

This is the environment in which banks must now operate — and build.

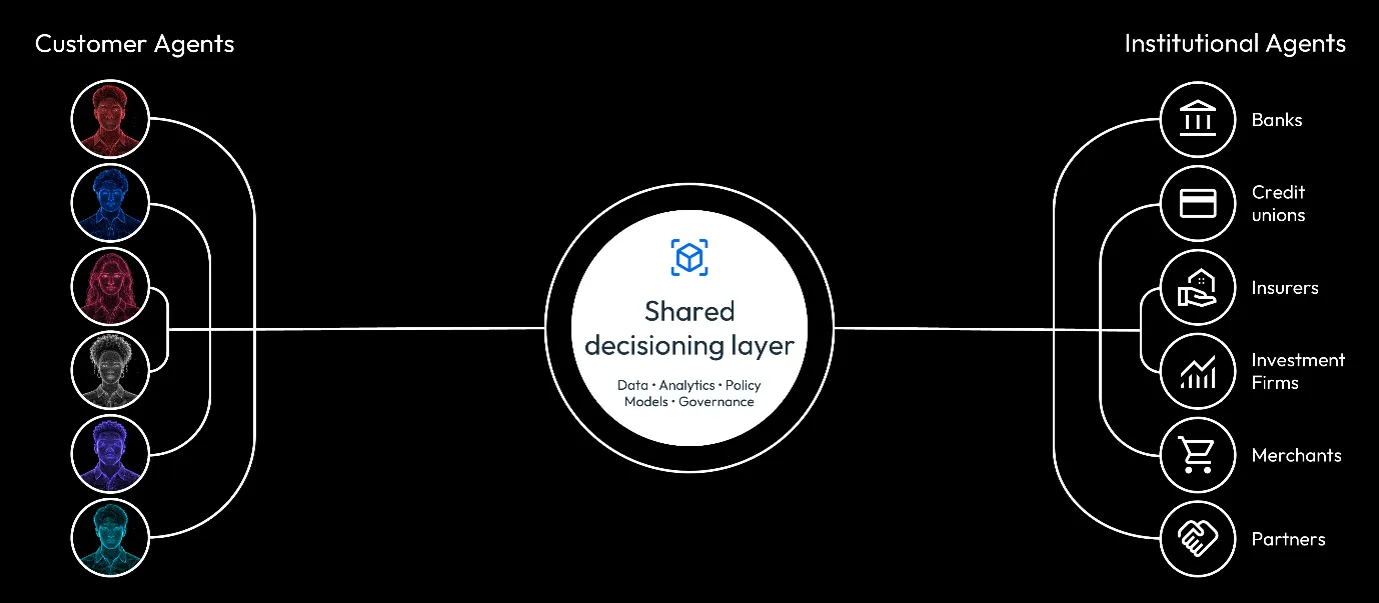

From Concept to Reality: FICO Platform and AI Agents

So what does this actually look like in practice? At FICO World 26, my colleague Nacho Gonzalez and I demonstrated exactly how an agentic financial future plays out — from both sides of the relationship.

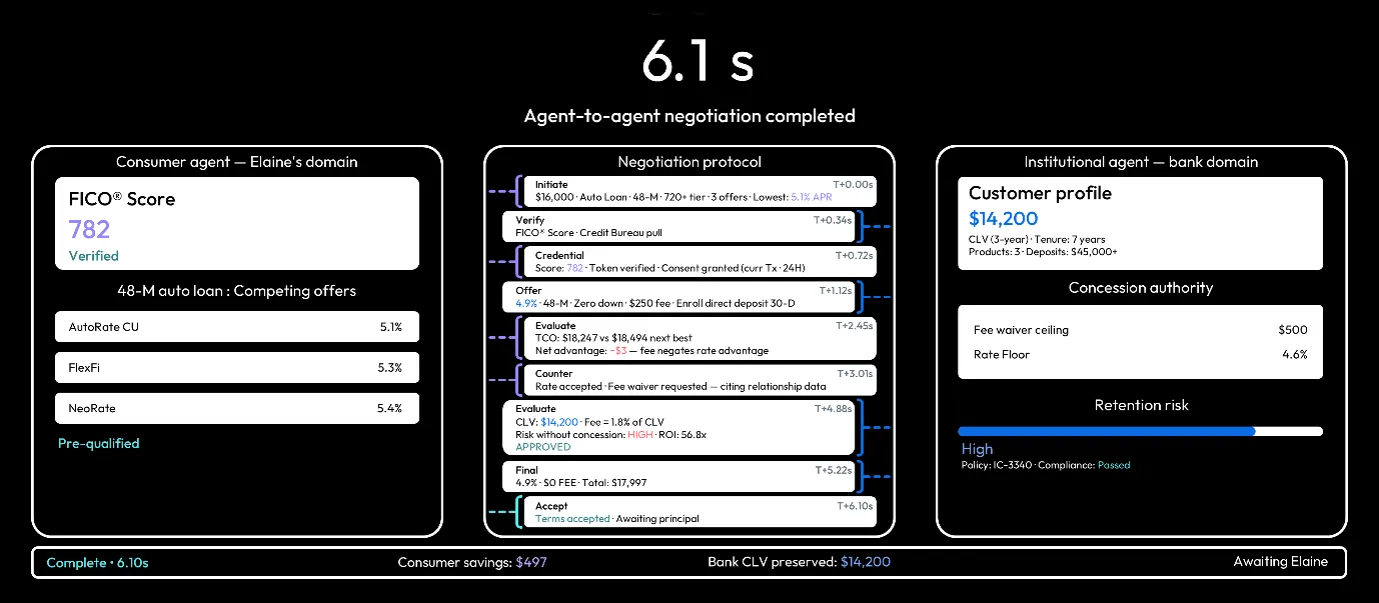

In our first demo, we followed a customer named Elaine, whose AI agent had flagged an urgent problem: her car was aging to the point of becoming a safety risk. Rather than spending hours calling dealerships and banks to find the best financing, Elaine's agent took over. It submitted a structured request for a 48-month auto loan — principal in the 720-plus credit tier, three competing offers already in hand, with the lowest at 5.1% APR. After a verification process, the bank's agents and Elaine's agent negotiated terms directly, with the bank ultimately waiving a $250 origination fee it had initially requested. The entire process took 6.1 seconds.

That 6-second negotiation was not a simple transaction. It required orchestration, data, analytics, decisions, and governance, all operating in concert on FICO Platform. At its core was Dynamic Profiles — a real-time understanding of every customer: who they are, what they want, and what they'll need next. As Behl described it in his keynote, this is "a dynamic, real-time, always-on customer profile engine" that powers hyper-personalization "whether it's the human or their agent." When the agent arrived at the bank's door, the bank already knew Elaine — and was ready.

Managing Credit Portfolios Using AI Agents

The second demo looked at the same dynamic from the institutional side, and it is equally transformative. Sarah is a VP of consumer lending whose portfolio is losing ground to a competitor that has just launched a rewards campaign, capturing momentum across her top two prime segments. In the past, she might have discovered this in a monthly review meeting, weeks after the damage was done. Instead, three of her own agents went to work.

Her Performance Monitor Agent detected that accounts in the FICO 660–720 segment were showing a seasonally adjusted decline in average revolving balance of $187 against the adjusted baseline — and had identified this within the past 30 days. Her Change Proposal Agent picked up that signal, diagnosed the cause, and designed a controlled experiment to identify the optimal incentive level needed to reverse the trend. Once Sarah reviewed and approved it, her Lifecycle Agent confirmed the experiment had cleared all five policy gates and flagged it as ready for full portfolio deployment. Total human involvement: one review, one adjustment, one tap.

This is the shift that matters most for institutions thinking about agentic AI. It is not just about responding to customers faster — it is about running the business on a fundamentally different cycle time. The gap between knowing and acting compresses from weeks to minutes. Problems are not found in meetings; they are detected as they happen. Analysis does not take weeks; action is immediate. Deployment does not happen in cycles; it happens in seconds.

The Age of AI Agents Starts Now – Are You Ready?

Behl closed his keynote with a challenge that applies equally here: "The question isn't: Do you have AI? It's: Do you have the foundation to make it work?" FICO Platform was built to be that foundation — AI-first by design, with every decision composable, every outcome traceable, and every action governable. It was built, as Behl put it, "before most people even saw the need."

The institutions that move first with this agentic approach will win. Not because they adopted a new tool, but because they fundamentally changed how they operate. The race is already underway — measured not in quarters, but in seconds.

Learn More About FICO’s Use of AI

- Watch the FICO World 26 presentation on how FICO Platform Is Built for Agentic AI

- Download the 2026 Gartner report to see why FICO was named a leader in the decision intelligence category

- Learn more about FICO® Platform

- Download the Future of Agentic AI whitepaper to learn how to close the AI operationalization gap

Frequently Asked Questions

Agentic AI refers to AI systems that can autonomously plan, reason, and take sequences of actions to complete complex tasks. Agentic AI goes beyond single-prompt responses to operate more like a digital agent pursuing a goal. In financial services, the conversation around agentic AI in 2026 sits at the intersection of opportunity and caution: the technology is advancing rapidly, but questions around governance, auditability, and real-world performance in regulated environments remain open.

AI governance in banking refers to the frameworks, policies, oversight structures, and accountability mechanisms that organizations put in place to ensure their AI systems operate safely, fairly, and in compliance with regulatory requirements. In the US, this includes alignment with model risk management guidance such as SR 11-7, as well as emerging requirements around model explainability, bias testing, and audit trails.

The shift to agentic AI redefines where human expertise is applied rather than eliminating it. Relationship managers, analysts, and operations staff will move up the value chain — from executing decisions to shaping them — by focusing on the rules, thresholds, and goals that govern how agents behave. This requires investment in two areas in parallel: capability building, so teams understand how to work alongside AI agents and interpret the signals they surface, and workflow redesign, so banks have clarity on which decisions can be fully automated, which need human review, and which should always involve a person. The Sarah demo from FICO World 26 captures the model well — her agents handled detection, diagnosis, and experiment design, but she remained the decision-maker throughout.

Compliance in an agentic world has to be built into the foundation of how decisions are made, not reviewed after the fact. When agents are operating at the speed and scale described in this post, every negotiated offer, adjusted term, and account action carries regulatory weight — and traditional downstream compliance review simply cannot keep pace. FICO Platform addresses this through full decision traceability, meaning banks can audit exactly what data and logic drove any given outcome, and through a policy gate framework that encodes jurisdiction-specific rules directly into the decisioning workflow. This allows agents operating across different regulatory environments to automatically apply the right constraints, supporting fair lending obligations and consumer protection requirements without requiring manual intervention at every step.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.