How Octane Achieved a 99% Digital Auto-Resolution Rate in Early-Stage Collections with FICO

Learn how Octane used FICO's collections solution to achieve a 99% digital auto-resolution rate and automate 2.4M+ interactions without adding headcount

Octane partnered with FICO to transform its early-stage collections strategy from a manual, agent-led model to an intelligent, digital-first approach. The new intelligent and scalable collections strategy led to a 99% resolution rate, automated 2.4+ million interactions per month, and scaled effortlessly without adding headcount.

Key Takeaways

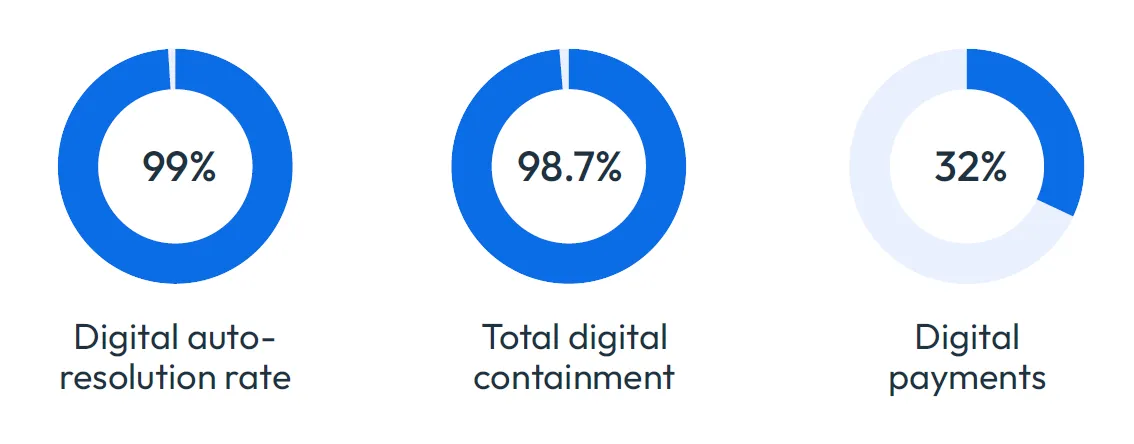

- Digital-first collections dramatically outperforms manual, agent-led approaches. Octane's shift from a dialer-based model to FICO's intelligent omni-channel communications resulted in a 99% digital auto-resolution rate and 98.7% total digital containment, proving that meeting customers on their preferred channels drives faster, higher-quality resolutions with less friction.

- Intelligent automation enables scale without adding headcount. By automating 2.4+ million interactions per month, Octane was able to absorb significant portfolio growth and manage increased delinquent volume while maintaining a stable collections team. Agents were freed up to focus exclusively on the highest-risk cases where human intervention matters most.

- A no-code, test-and-learn environment keeps strategy sharp and responsive. Using FICO® Platform, Octane can implement major strategy adjustments every 4–6 weeks without developer support, running champion/challenger tests to continuously refine messaging, timing, and channel mix in response to shifting customer behavior and market conditions.

- 4. Better collections and better customer experience are not mutually exclusive.

By delivering timely, risk-aligned communications through preferred channels with embedded payment links, Octane achieved 32% of digital payments submitted within 24 hours of communication, all while giving customers a smoother, lower-friction experience that reflects the same digital-first ethos they expect from the rest of the Octane journey.

Who Is Octane?

Octane is a leading U.S. point-of-sale lender specializing in powersports, outdoor power equipment, RV, auto, and other vehicle purchases. Through its in-house lender, Octane provides a seamless, end-to-end technology and financing experience for consumers across the credit spectrum, serving credit-worthy customers from super-prime buyers to first-time credit applicants who may be underserved by traditional lenders.

With more than 4,000 dealership partners and over $8 billion in originations, Octane has rapidly become one of the most influential players in the recreation finance industry and is expanding into new industries. Customers and dealerships choose Octane for its fast, transparent, digital-first financing experience that empowers borrowers and removes friction during the buying process.

Octane’s Challenge: Rapid Portfolio Growth and Rising Delinquencies Exposed the Limits of Manual Collections Outreach

Octane's rise coincided with one of the most difficult environments U.S. vehicle lenders had faced in decades. Delinquencies climbed across the industry, with subprime 60+ days past-due rates reaching their highest levels since the mid-1990s. Sports and performance vehicles, a core segment for Octane, carried elevated risk due to high payments, costly insurance, and greater sensitivity to economic shifts. Repossessions increased significantly, lenders tightened credit standards, and used-vehicle interest rates rose into double digits, particularly for subprime borrowers.

At the same time, Octane was entering a period of significant expansion. Beginning in 2019, the company broadened its focus beyond subprime lending, expanding into prime segments and new markets such as auto, recreational vehicles, tractors, and outdoor power equipment. Leadership anticipated rapid growth and the portfolio nearly doubled annually.

As volume increased, so did the number of accounts requiring payment reminders or early-stage collections outreach. The company's servicing team relied primarily on an agent-led, dialer-based strategy, partially through third-party service providers. As account volumes accelerated, it became clear that this approach could not scale and limited Octane's ability to directly control how and when customers were engaged.

The onset of COVID and broader market volatility introduced additional delinquency risk, making it even more important to manage early-stage performance carefully while continuing to grow. Together, these forces created a clear need to rethink collections by shifting toward a more scalable, efficient, and risk-aligned approach to customer engagement.

The Solution: How FICO Evolved Agent-Led Dialing with Intelligent Digital Engagement

As the business expanded, Octane set a strategic goal to improve early-stage collections with an intelligent digital-first approach. Customers were already interacting with Octane digitally during the prequalification and buying process, and the company saw an opportunity to extend that experience into collections. The team wanted a solution that would reach customers at the right time and on their preferred channel, personalize communication to risk and behavior, and reduce dependence on manual, agent-led workflows.

To bring this strategy to life, Octane turned to a partner they already trusted. The lender has partnered with FICO for originations and credit strategy, including using FICO® Auto Score 10. Extending the collaboration into intelligent digital engagement in collections was a natural next step. The team selected the FICO® Platform – Omni-Channel Engagement Capability for Collections (Customer Communication Services) to build, automate, and optimize their new collections strategy.

FICO's Customer Communications Capability enabled intelligent, automated, risk-aligned outreach across text, email, and voice, ensuring customers received timely reminders through the channels they prefer. Messages included embedded payment links and simple response options, making it easy for customers to act quickly without waiting for a phone call. The capability also reserved agent time for the highest-risk cases, improving focus where human engagement matters most.

Implementation moved quickly. Using FICO's no-code environment for designing and updating digital engagement strategies, Octane's servicing team configured the new approach in-house without relying on developers. The team built flexible workflows tied to risk tiers, payment behavior, and timing, then launched champion/challenger tests to begin optimizing immediately. The intelligent digital communications capability integrated smoothly with Octane's servicing systems, enabling automated case creation and real-time response handling across the entire portfolio.

The Results: 99% Digital Resolution, 2.4+ Million Monthly Automated Interactions, and a Scalable Collections Engine

FICO's intelligent digital communication capabilities have enabled Octane to shift from manual, agent-heavy outreach to a modern, data-driven collections capability that meets customers where they are, adapts quickly, and scales effortlessly as the business continues to grow. The result is a collections operation that performs more effectively, scales efficiently, evolves through rapid strategy refinement, and delivers a smoother, more supportive customer experience.

Improved Digital Resolution Performance

Using intelligent digital communications for early-stage collections, Octane’s in-house lender reaches customers quickly through their customers’ preferred communication channels, which has led to faster engagement, higher response rates, and more self-service resolutions. Automated reminders, embedded payment links, and simple response options enable customers to resolve their accounts with minimal friction.

This intelligent digital first approach delivers measurable improvements, including:

- 99% digital auto resolution rate

- 98.7% total digital containment across all cases, including:

- 32% digital payments submitted within 24 hours of communication

Clear Scalable Capacity

As Octane’s portfolio expanded, delinquent account volume increased. Digital communications allowed the team to absorb this growth seamlessly by automating outreach, streamlining workflows, and ensuring customers received reminders at the right time and on the right channel, without adding complexity or strain to the call center.

This intelligent, digital-first operating approach delivers clear scalability benefits, including:

- 2.4+ million automated interactions per month, supporting large-scale customer outreach

- Managed increased delinquent volume, while maintaining a stable collections team

- Majority of early-stage cases handled by automated digital outreach

- Agents are reserved for higher risk customers requiring human intervention

Ongoing Strategic Agility

Octane continually refines its digital engagement strategies to stay aligned with customer behavior and portfolio needs. Using FICO® Platform, the team can adjust messaging, timing, and channel mix quickly while running champion/challenger tests to identify the most effective approaches. This rapid, iterative approach ensures communication strategies remain current and continue improving over time.

This continuous test-and-learn approach delivers ongoing performance improvement, including:

- Major adjustments implemented every 4–6 weeks

- Ability to deploy new or revised engagement flows without developer support

- Improved effectiveness across scripts, channels, and timing sequences

- Faster adaptation to shifting customer behavior or market conditions

Improved Customer Experience

Octane’s borrowers, many of whom are financing a meaningful lifestyle purchase, benefit firsthand from the simple, digital-first communications experience. Customers receive timely reminders through their preferred channels and can resolve their accounts quickly through embedded links and intuitive self-service flows.

This experience-focused design delivers a great customer experience, including:

- Higher digital self-service across email, SMS, and voice

- Faster, lower-friction resolutions via embedded payment links

- Consistent, risk-aligned communication across all customer segments

What’s Next for Octane: Expanding Digital Engagement and Intelligence

Octane continues to build on its digital-first collections foundation, with a focus on expanding both the reach and sophistication of its engagement strategies. The team is actively exploring new ways to enhance communication channels, strengthen response rates, and further reduce reliance on manual processes.

Octane plans to incorporate more advanced, AI-driven capabilities into its digital communications strategy. These enhancements are expected to enable more dynamic, personalized interactions and help the team respond more intelligently to customer behavior in real time. In parallel, Octane is exploring ways to extend digital engagement into later stages of delinquency for select segments, as well as integrating collections strategies with broader customer assistance programs. This includes evaluating options such as payment flexibility and loan assistance offerings to better support customers who may be experiencing ongoing financial challenges.

Learn More About FICO's Collections Solutions

- Download the full Octane and FICO case study

- Read the case study to see how one company is saving $5 million annually in write-offs thanks to FICO’s collections analytics

- Learn more about the empathy paradox in collections and how it leads to increased revenue

- Learn more about FICO’s Collections solutions

Frequently Asked Questions

Reaching customers through a single channel is often not enough. By coordinating timing and sequencing across SMS, email, voice, and digital touchpoints, omni-channel communications solutions increase the likelihood that messages are seen, understood, and acted on. This helps drive engagement, improve resolution rates, and reduce the need for agent intervention.

The most effective approach is to reserve agent time for the highest-risk cases where human intervention matters most, while automating outreach for the majority of early-stage cases. This ensures that agent capacity is focused where it has the greatest impact, while customers who are likely to self-serve receive timely, frictionless reminders through their preferred channels.

Effective personalization doesn't require manual effort. By building flexible workflows tied to risk tiers, payment behavior, and timing, lenders can ensure that each customer receives the right message, on the right channel, at the right moment, all through automated, intelligent outreach. Embedded payment links and simple response options further reduce friction and make it easy for customers to act quickly.

The key is building a continuous test-and-learn capability into the collections strategy. Using a no-code environment, teams can adjust messaging, timing, and channel mix quickly without relying on developers, while running champion/challenger tests to identify the most effective approaches. This allows major strategy adjustments to be implemented every 4–6 weeks, ensuring communication strategies remain current and continue improving over time.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.